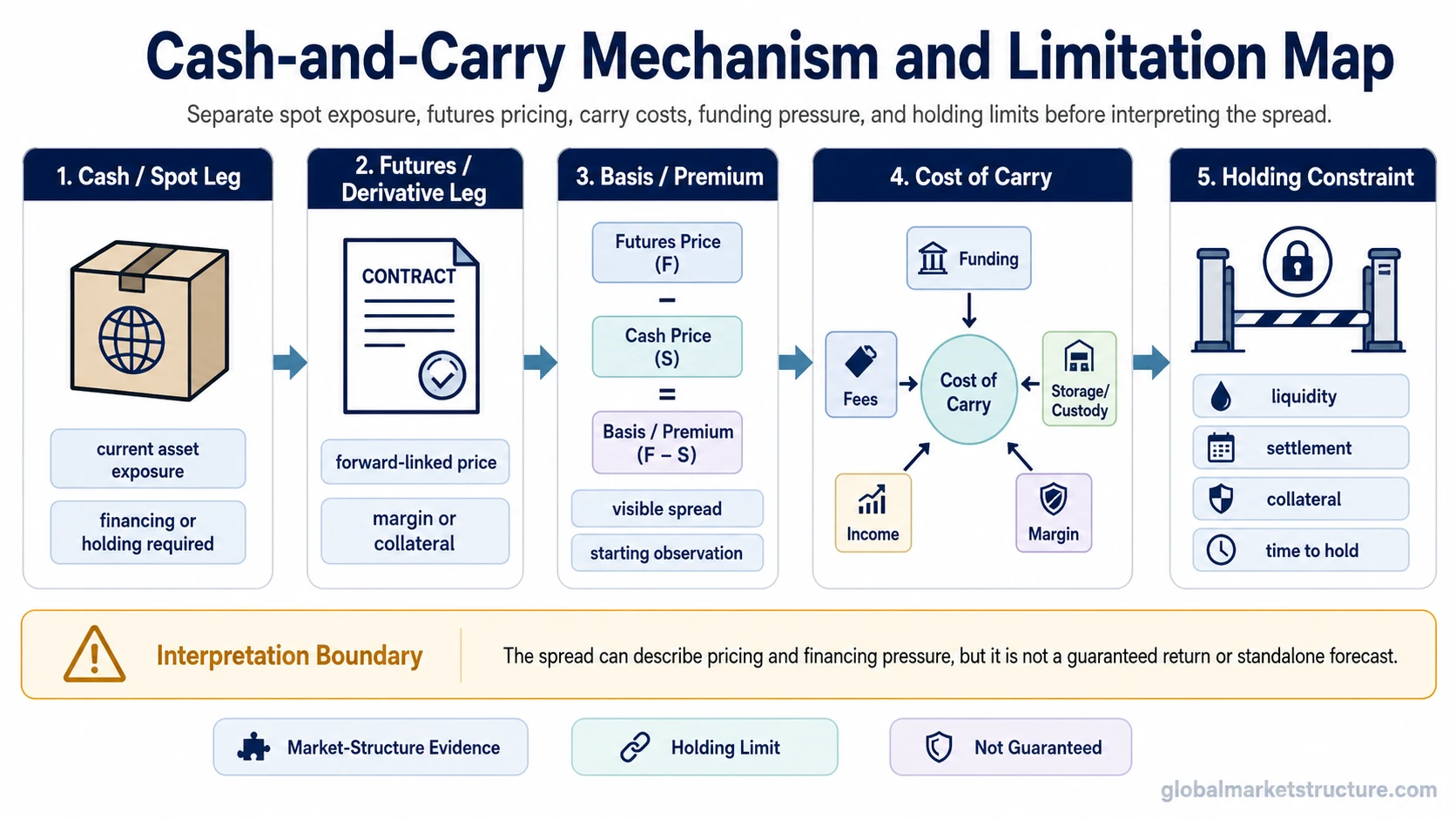

A cash and carry trade is a paired market structure in which a cash or spot asset is held while a related futures or derivative position offsets part of the price exposure. The interpretation depends on the gap between the current price, the future price, and the cost of carry, and it is not a guaranteed return because financing, liquidity, execution quality, margin, settlement, and holding conditions can change the result.

Definition: A cash and carry trade links a cash or spot position with a related futures or derivative position. The structure is built around basis or futures premium, carry costs, financing conditions, and the ability to hold both sides until the expected price relationship changes.

For market-structure interpretation, the important point is not that the trade promises a clean payoff. Cash-and-carry activity can reveal how spot pricing, futures pricing, financing costs, collateral pressure, liquidity, and holding capacity interact.

Key Points

- A cash and carry trade pairs a cash or spot position with a related futures or derivative position.

- The spread only matters after basis, carry costs, funding, margin, liquidity, fees, settlement, and holding ability are considered.

- The structure can look arbitrage-like, but market-neutral exposure does not remove financing, execution, or liquidity risk.

- Cash-and-carry evidence is better read as pricing and financing evidence, not as a standalone forecast or trade instruction.

What Is a Cash and Carry Trade?

A cash and carry trade starts with a price relationship between a cash or spot asset and a related future price. The cash side represents current ownership or exposure. The futures or derivative side represents a forward-linked price relationship that may trade above or below the cash price.

When the future price is above the current cash price by more than the estimated cost of carry, the structure may appear attractive on paper. That first reading is incomplete until financing, collateral, liquidity, execution, settlement, and the time needed to hold the position are included.

The phrase is often connected with arbitrage because the two legs can offset part of the directional price exposure. That does not make the result automatic. A change in funding cost, margin requirement, market depth, or settlement assumption can change the interpretation of the spread.

How the Cash-and-Carry Mechanism Works

The mechanism is easiest to understand as a relationship between two prices and the cost of maintaining the cash position. The cash asset has to be financed or held. The futures or derivative contract reflects a future-linked price. The basis or premium is meaningful only after carry costs and practical constraints are included.

| Component | What it means | What can change the interpretation |

|---|---|---|

| Cash or spot leg | The current asset exposure that is bought, held, borrowed, or otherwise maintained. | Financing cost, borrow availability, custody, storage, income, collateral treatment, or balance-sheet capacity. |

| Futures or derivative leg | The related forward-linked contract used to offset part of the cash asset’s price exposure. | Contract terms, margin, settlement assumptions, liquidity, roll cost, and execution quality. |

| Basis or premium | The price gap between the cash asset and the related future or derivative price. | The gap may narrow, widen, or become expensive to hold before any expected convergence occurs. |

| Cost of carry | The cost and income profile of holding the cash leg until the expected price relationship changes. | Funding rates, fees, storage, insurance, income, coupons, dividends, or margin requirements depending on the asset type. |

| Holding constraint | The ability to maintain both sides long enough for the price relationship to matter. | Liquidity shocks, margin calls, financing withdrawal, position limits, execution slippage, or changing collateral conditions. |

The same apparent spread can carry different meaning under different funding conditions. A wide premium with stable financing and deep liquidity is not the same as a wide premium during rising funding stress, thin order books, or changing collateral requirements.

Cash-and-Carry, Basis, and Cost of Carry

Basis is the price relationship between the cash asset and the related futures or derivative contract. In a cash-and-carry structure, the basis matters because it is the visible gap that the trade is built around. Cost of carry determines whether that gap is large enough to compensate for the real cost of holding the cash side.

Carry cost is not always a single financing number. Depending on the asset, it may include borrowing cost, funding spread, storage, insurance, custody, dividends, coupons, fees, margin, or income that offsets part of the holding cost. The more uncertain those inputs are, the less reliable a simple spread reading becomes.

A positive futures premium should therefore be treated as a starting observation, not a finished conclusion. The stronger interpretation asks whether the premium still exists after realistic funding, margin, liquidity, settlement, and holding assumptions are applied.

Why Cash and Carry Is Not a Guaranteed Return

Cash-and-carry language can sound cleaner than the structure really is because the two legs may reduce directional price exposure. The remaining risk is often concentrated in financing, liquidity, margin, execution, settlement, and the ability to hold the position under stress.

Limitation: A cash-and-carry spread can look attractive before the real constraints are included. Funding can become more expensive, margin requirements can change, liquidity can thin, execution can worsen, settlement assumptions can fail, and the position can become difficult to maintain.

| Risk or constraint | Why it matters | Market-structure reading |

|---|---|---|

| Funding cost | The cash leg often needs financing or balance-sheet capacity. | A spread that looked sufficient can shrink after financing costs rise. |

| Margin and collateral | The futures or derivative leg can require variation margin or collateral support. | Pressure can appear even when the long-term price relationship still appears logical. |

| Liquidity | Both legs must be entered, maintained, adjusted, or exited under real market depth. | Thin liquidity can turn a theoretical spread into an unstable holding problem. |

| Execution | The two legs may not be executed at the assumed prices. | Slippage, fees, and timing gaps can change the economics of the structure. |

| Settlement and delivery | The expected price relationship depends on contract terms and settlement behavior. | A simplified convergence assumption may not match the practical settlement path. |

| Ability to hold | The structure may need time for the price relationship to normalize. | Funding or margin pressure can force adjustment before the expected relationship plays out. |

A Practical Cash-and-Carry Scenario

A futures contract trades above the cash asset by more than the first estimate of carry costs. At first, the spread appears to compensate for holding the cash asset while offsetting part of the exposure through the futures contract.

The reading changes if the financing, fee, margin, or liquidity assumptions become harder to maintain before the expected price relationship changes. The spread still exists, but the market-structure message becomes less about a clean arbitrage and more about the conditions required to hold the basis exposure.

This scenario separates the visible price gap from the hidden constraints behind it. A spread can describe pricing pressure, financing conditions, and balance-sheet capacity without producing a reliable forecast by itself.

Cash and Carry Trade vs Related Concepts

Cash-and-carry overlaps with several nearby concepts, but the distinctions matter. The structure is specifically about a paired cash or spot exposure and a related futures or derivative exposure. Other carry and basis concepts may share some language while describing a different market relationship.

| Concept | Core distinction | Why the distinction matters |

|---|---|---|

| Cash and carry trade | Pairs a cash or spot position with a related futures or derivative position. | The focus is the relationship between spot price, future price, cost of carry, and holding constraints. |

| Carry trade | Broader funding and exposure logic where an investor or institution seeks to benefit from a carry differential. | It does not always require a paired cash and futures structure. |

| Basis trade | Uses the price relationship between related instruments as the central evidence. | Cash-and-carry is one way basis can matter, but the terms should not be treated as identical. |

| Treasury basis trade | Treasury basis trade focuses on the relationship between cash Treasuries and Treasury futures. | The Treasury-specific version brings its own financing, futures, collateral, and systemic-risk considerations. |

| Fixed income carry | fixed income carry describes income, financing, and rates exposure in bonds or rate-sensitive instruments. | It can involve coupon income and curve effects without being the same paired cash/futures arbitrage structure. |

| Reverse cash-and-carry | A related opposite-direction structure built around the reverse price relationship. | It belongs near the same concept family but should not replace the basic cash-and-carry definition. |

Common Mistakes When Interpreting Cash-and-Carry

Common mistake: Treating a positive futures premium as a free return. The premium is only one input. Financing, margin, liquidity, execution, settlement, and holding ability decide whether the apparent spread remains meaningful.

Another common mistake is treating market-neutral language as risk-free language. Offsetting price exposure does not remove funding pressure, margin calls, collateral strain, or liquidity risk. The structure may reduce one type of exposure while increasing sensitivity to another.

A third mistake is treating the spread as a forecast. Cash-and-carry activity can help describe pricing and financing conditions, but it does not forecast market direction by itself. The better interpretation asks what the spread reveals about basis, liquidity, funding availability, and the cost of holding exposure.

FAQ

Is a cash and carry trade risk-free?

No. A cash and carry trade can reduce part of the directional price exposure, but funding costs, margin, liquidity, execution, settlement, and holding constraints can still change the result.

Is cash and carry the same as a basis trade?

No. Cash and carry is a specific paired cash or spot and futures or derivative structure. A basis trade is broader and can describe different ways of using price relationships between related instruments.

What does cost of carry mean in a cash-and-carry trade?

Cost of carry is the cost and income profile of holding the cash asset until the expected price relationship changes. It can include financing, storage, insurance, income, fees, margin, borrow, or other frictions depending on the asset.

What is reverse cash-and-carry?

Reverse cash-and-carry is a related opposite-direction structure that starts from the reverse price relationship between the cash asset and the related futures or derivative contract.