A Treasury basis trade is a Treasury cash-futures relative-value trade that commonly pairs a long cash Treasury position with a short related Treasury futures position, often with the cash leg financed through repo. The trade matters for market structure because it connects futures demand, repo funding, leverage, dealer balance-sheet capacity, and Treasury-market liquidity, but it is not by itself a market-direction forecast, a crisis signal, or a trade recommendation.

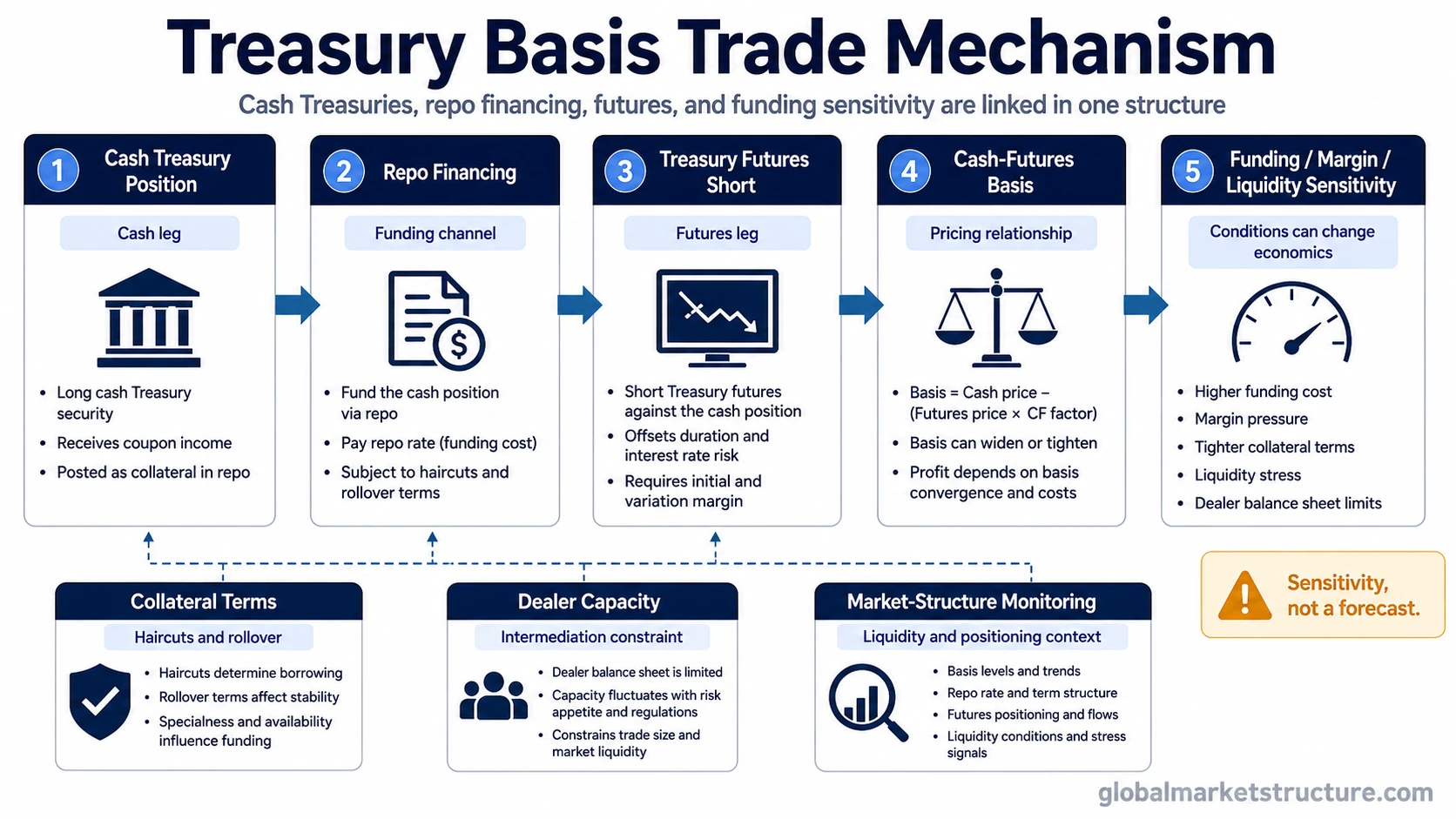

Definition: A Treasury basis trade seeks to capture the difference between a cash Treasury security and a related Treasury futures contract. The basic structure is cash Treasury exposure on one side, Treasury futures exposure on the other side, and financing conditions around the cash leg in the middle.

Price convergence is only one part of the trade; financing cost, margin, collateral, delivery terms, and liquidity can change the result.

Key Points

- A Treasury basis trade is built around the relationship between a cash Treasury security and a related Treasury futures contract.

- Repo financing often supports the cash Treasury leg, which makes funding conditions central to the structure.

- Leverage and margin can make small basis changes more important for participants using financed positions.

- The concept is relevant to Treasury-market liquidity monitoring because it links futures demand, repo funding, positioning, and dealer capacity.

- The existence of Treasury basis trading does not, by itself, establish an imminent unwind, crash, rate move, or trading opportunity.

What Is a Treasury Basis Trade?

A Treasury basis trade is the Treasury-market version of a cash-futures basis relationship. A participant may buy a cash Treasury security and sell a related Treasury futures contract, seeking to benefit from the difference between the cash security and the futures price after financing and other costs.

The “basis” is the relationship between the cash Treasury price and the futures price. In practice, the exact calculation can depend on delivery options, cheapest-to-deliver considerations, financing assumptions, and futures contract details, so the basis should not be treated as a single universal signal.

Core boundary: The Treasury basis trade is narrower than broad basis trading. It belongs specifically to the relationship between cash Treasuries, Treasury futures, and the funding conditions that support the position.

Treasury Basis Trade Classification

| Dimension | Treasury Basis Trade Reading |

|---|---|

| Category | Treasury cash-futures relative-value trade. |

| Cash leg | Long exposure to a cash Treasury security. |

| Futures leg | Short exposure to a related Treasury futures contract. |

| Funding channel | Repo financing is commonly used to finance the cash Treasury position. |

| Main participants | Often associated with leveraged relative-value participants, while demand for Treasury futures can influence the cash-futures relationship. |

| Market-structure relevance | Links Treasury futures demand, repo funding, leverage, dealer capacity, and Treasury-market liquidity. |

| Common misread | Treating the trade as a guaranteed arbitrage, a standalone crisis signal, or a direct market-timing tool. |

How the Treasury Basis Trade Works

The mechanism begins with a cash Treasury position. A participant buys or holds a Treasury security and finances that position, often through repo. Repo financing matters because the cash leg has to be funded, rolled, and collateralized.

The offsetting futures leg is usually a short Treasury futures position. The futures short helps isolate the cash-futures relationship rather than taking a simple directional Treasury exposure. The expected result depends on the basis, financing costs, delivery economics, margin requirements, and transaction frictions.

Mechanism sequence:

- Cash Treasury position is established.

- The cash position is commonly financed through repo.

- A related Treasury futures contract is sold short.

- The cash-futures basis becomes the main pricing relationship being monitored.

- Funding cost, margin, collateral, and liquidity conditions determine whether the trade remains economically attractive.

The structure can look mechanically simple, but the risk channel is not only price convergence. The trade depends on stable financing, manageable margin, and enough market liquidity to adjust or reduce exposure without excessive price impact.

Why Repo Funding Matters

Repo financing is a funding channel, not the whole trade. It allows the cash Treasury leg to be financed against collateral, but the terms of that financing can change. If repo rates rise, haircuts increase, rollover becomes less reliable, or collateral terms tighten, the same cash-futures basis can become less attractive.

Funding liquidity and repo financing are related, but they are not identical. Repo describes a specific secured financing channel, while funding liquidity describes the broader ability of participants to obtain and maintain financing on workable terms.

Margin also matters because the futures leg can require additional collateral when prices move. A position that appears small in basis terms can still become sensitive to funding and liquidity if leverage is high and financing conditions shift at the same time.

Funding limitation: Repo access does not remove risk. It changes the trade from a simple price relationship into a financing-dependent structure where rollover terms, margin calls, collateral requirements, and liquidity can affect stability.

Why Treasury Basis Trades Matter for Market Structure

Treasury basis trades sit at the intersection of cash Treasuries, Treasury futures, repo markets, and leveraged positioning. That intersection can affect how liquidity behaves when volatility rises or funding terms become less forgiving.

Demand for Treasury futures can affect the cash-futures relationship that relative-value participants monitor. When that positioning is financed, the trade also becomes connected to balance-sheet capacity, dealer intermediation, collateral conditions, and the ability of participants to maintain exposure through changing market conditions.

For market-structure interpretation, the Treasury basis trade is best read as a transmission mechanism. It helps explain how a pricing relationship can connect to funding liquidity and market liquidity, but it does not independently forecast interest rates, equity direction, or systemic stress.

When the Treasury Basis Trade Becomes Vulnerable

A Treasury basis trade becomes more fragile when several pressures appear together. Higher funding costs can reduce the economics of the cash leg. Wider repo haircuts can require more collateral. Higher futures margin can increase liquidity needs. Higher volatility can make both legs harder to manage. Lower market depth can raise the cost of reducing exposure.

| Pressure Point | Why It Matters | False Reading to Avoid |

|---|---|---|

| Repo rates rise | Financing the cash Treasury leg becomes more expensive. | Higher funding cost alone does not prove forced selling. |

| Haircuts increase | More collateral may be needed to support the same exposure. | A haircut change is not the same as a market crash signal. |

| Futures margin rises | Participants may need more liquid resources to maintain the futures leg. | Margin pressure does not prove that all participants are under stress. |

| Market liquidity weakens | Reducing or adjusting positions can become more costly. | Thin liquidity should not be read as a complete explanation by itself. |

| Dealer capacity tightens | Intermediation can become less elastic when balance-sheet constraints matter. | Dealer capacity is one channel, not a complete causal story. |

The strongest interpretation requires supporting evidence from funding, margin, liquidity, volatility, collateral, and positioning conditions. A single input can be informative, but it is rarely enough to support a strong market-structure conclusion.

Treasury Basis Trade vs Basis Trade and Cash-and-Carry Trade

A basis trade is the broader concept: it refers to trading the price difference between related instruments. The Treasury basis trade is the Treasury-specific version built around cash Treasury securities, Treasury futures, and the funding conditions that support the position.

A cash-and-carry trade is a broader arbitrage family where a cash asset and a related derivative are paired. Treasury basis trading overlaps with that logic, but the Treasury-market version has its own funding, delivery, margin, and liquidity characteristics.

Clean distinction: Basis trade is the broad category. Cash-and-carry is the broader arbitrage family. Treasury basis trade is the Treasury cash-futures expression where repo funding and Treasury-market liquidity become central to interpretation.

Practical Scenario: Funding Conditions Tighten

A participant holds cash Treasuries financed through repo and offsets that exposure with a short Treasury futures position. Futures demand remains firm, but repo financing becomes more expensive and collateral terms become less favorable. At the same time, futures margin requirements rise as volatility increases.

The basis relationship may still appear narrow in price terms, but the economics of the position have changed. The trade is now more sensitive to funding cost, liquidity needs, and the ability to maintain both legs. That scenario can matter for market-structure monitoring without establishing an imminent unwind or a broader market crisis.

Common Misreadings

| Misreading | Safer Interpretation |

|---|---|

| Treating Treasury basis trading as guaranteed arbitrage. | Convergence can be part of the logic, but financing costs, margin, delivery details, and liquidity frictions can change the result. |

| Treating basis-trade size as proof of an imminent forced unwind. | Positioning can raise monitoring importance, but stress depends on funding, margin, volatility, collateral, liquidity, and participant behavior. |

| Treating the Treasury basis trade as a rate forecast. | The structure is about a cash-futures relationship and financing conditions, not a standalone forecast for yields. |

| Treating repo financing as the entire concept. | Repo is the funding channel for the cash leg; the full trade also includes the futures leg, basis economics, margin, and liquidity conditions. |

FAQ

Is a Treasury basis trade the same as a basis trade?

No. A Treasury basis trade is a specific form of basis trading built around cash Treasuries and Treasury futures. Basis trading is the broader concept and can appear in other markets or instruments.

Why does repo financing matter in a Treasury basis trade?

Repo financing often funds the cash Treasury leg. Changes in repo rates, haircuts, rollover conditions, or collateral requirements can affect the economics and stability of the trade.

Does Treasury basis trading predict a market crisis?

No. Treasury basis trading can matter for liquidity and funding-risk monitoring, but the existence of the trade does not, by itself, predict a crisis, a forced unwind, or a specific market direction.

Why is leverage important in Treasury basis trades?

Leverage can make small changes in basis, funding cost, margin, or liquidity more important for participants that rely on financing. Leverage increases sensitivity, but it does not make one outcome certain.