A basis trade is a relative-value or convergence position built around the price gap between a cash or spot asset and a related futures or derivative contract. In market-structure analysis, it can reveal positioning, leverage, funding dependence, and possible unwind pressure, but it does not forecast yields, equities, policy, or risk direction by itself.

Definition: A basis trade focuses on the difference between two linked prices, usually a cash price and a futures price, or a spot price and a related derivative price. The trader is not simply expressing a directional market view. The structure depends on whether the price relationship narrows, converges, or remains financeable.

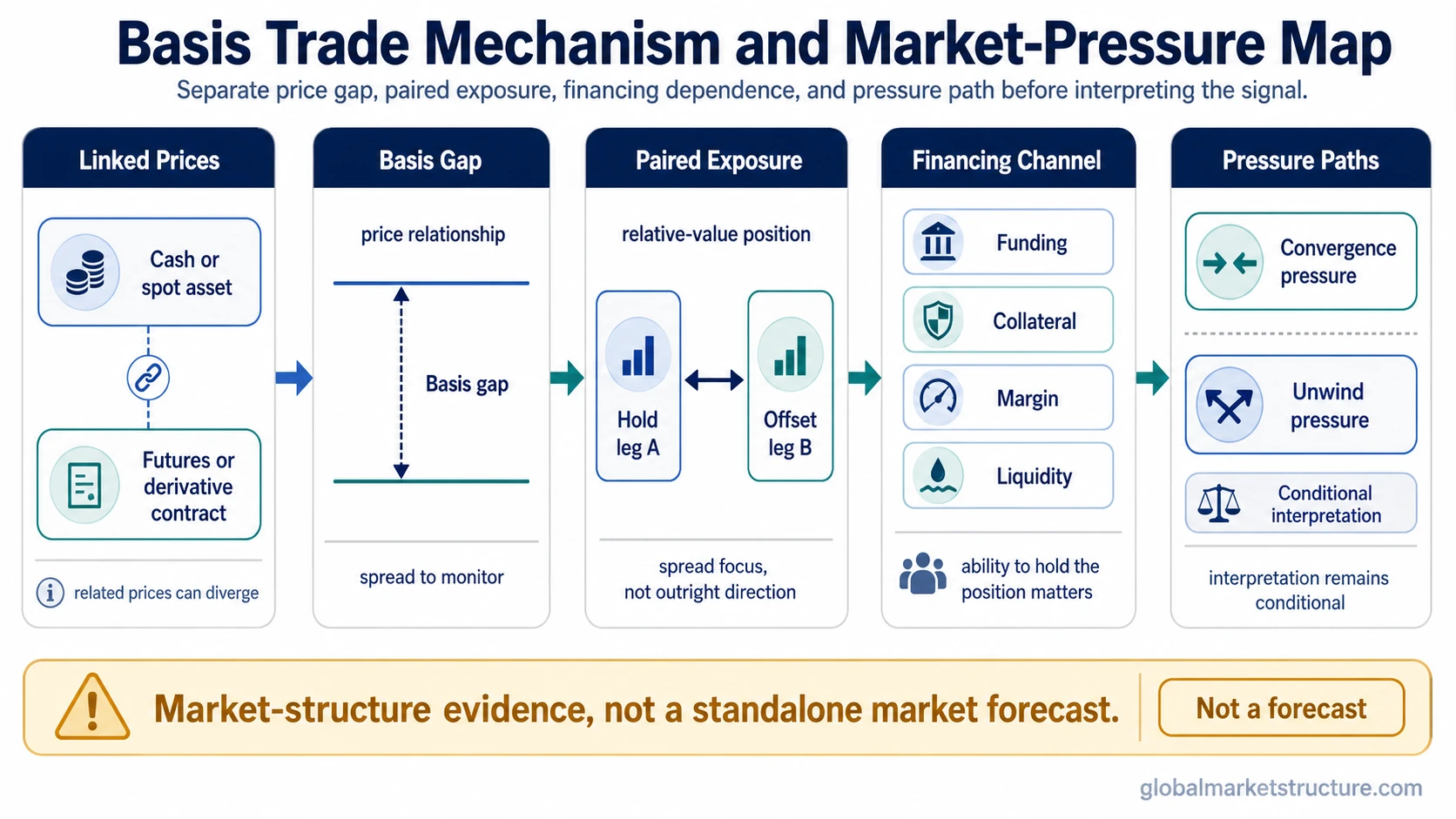

Basis Trade in One View

- A basis trade is built around a price gap between related instruments, not around a simple bullish or bearish forecast.

- The trade often depends on financing, margin, collateral, and the ability to hold both sides of the position.

- A small basis can matter when the position is large, leveraged, or sensitive to changes in funding conditions.

- Basis-trade activity can show positioning and market-pressure risk, but it is not a standalone signal for market direction.

What a Basis Trade Is and What It Is Not

A basis trade uses the relationship between two linked market prices. One side is usually a cash or spot instrument. The other side is usually a futures contract, forward contract, swap, or another derivative tied to the same underlying exposure.

The useful distinction is that the basis trade is about the spread between the instruments. A directional trade mainly depends on whether the underlying market rises or falls. A basis trade depends more on how the price gap behaves, whether the position can be financed, and whether stress forces one or both sides to unwind.

| Concept | What it means | How it differs from a basis trade |

|---|---|---|

| Basis trade | A relative-value position around the gap between linked cash, spot, futures, or derivative prices. | The core focus is the spread relationship and its financing conditions. |

| Treasury basis trade | A specific form involving cash Treasuries and Treasury futures. | It is an important example, not the full meaning of basis trade. |

| Basis trading | The broader activity of trading or managing basis relationships. | It can describe the process, while basis trade names the position structure. |

| Cash and carry trade | A structure that buys the cash asset and sells the related futures contract when the spread supports carry after costs. | It is one common basis-related structure, but not every basis trade is cash-and-carry. |

| Carry trade | A position built around earning a funding, yield, or rate differential. | It can overlap with financing logic, but it is not automatically a basis trade. |

How the Basis Trade Mechanism Works

The mechanism begins with a basis gap. If the cash or spot instrument and the related futures or derivative contract are priced differently, a relative-value participant may try to hold one side and offset it with the other side.

1. Basis gap appears: the cash or spot price and the related futures or derivative price do not line up after carry, financing, delivery, or market-friction costs.

2. Paired exposure is created: the position usually combines a long side and a short side so the main focus is the spread, not outright market direction.

3. Financing supports the position: leverage, margin, collateral, and borrowing costs determine whether the trade remains attractive and durable.

4. Convergence or stress changes the reading: the basis may narrow as expected, stay open because of structural frictions, or widen if funding and liquidity conditions deteriorate.

A basis trade can look calm when the spread is stable, but the underlying pressure can change quickly if financing becomes more expensive, margin requirements rise, or liquidity weakens in one leg of the position.

Basis Trade Classification

Basis trades differ by market, instrument pair, financing channel, and the reason the basis exists. A general classification helps prevent the common mistake of treating every basis trade as a Treasury trade or as a simple cash-and-carry structure.

| Basis-trade type | Typical linked prices | Main pressure channel | Interpretation limit |

|---|---|---|---|

| General cash or spot versus futures basis | Cash/spot instrument and related futures contract | Convergence, carry costs, funding cost, liquidity in each leg | Does not automatically show market direction. |

| Treasury cash-futures basis | Cash Treasury securities and Treasury futures | Repo financing, futures positioning, dealer intermediation, cash-market liquidity | Needs Treasury-specific evidence before making size, leverage, or stress claims. |

| Commodity basis | Physical or spot commodity and futures contract | Storage, delivery, inventory, financing, and contract maturity | May reflect logistics and storage constraints, not only speculative positioning. |

| Derivative or swap basis | Related derivative prices, swaps, forwards, or funding-linked instruments | Collateral, funding rates, balance-sheet capacity, counterparty terms | Requires careful definition of the exact instruments being compared. |

| Cash-and-carry structure | Cash asset and futures contract | Carry after financing, storage, collateral, and execution costs | Adjacent to basis trading, but not the whole category. |

Why Leverage and Funding Matter

Many basis trades involve small spread differences. That means the economic incentive can look modest unless the trade is large, financed, or repeated across many related instruments. Leverage can turn a small basis into a meaningful source of market exposure, but it also makes the position sensitive to financing conditions.

The repo market matters when cash securities are financed through short-term borrowing. If borrowing costs rise, collateral terms tighten, or balance-sheet capacity becomes scarce, a basis trade can become harder to hold even if the original spread logic still appears valid.

Key limitation: a basis trade can be mechanically hedged in price terms while still exposed to funding, margin, liquidity, and balance-sheet constraints. Spread logic does not remove financing risk.

How Basis-Trade Activity Can Affect Market Pressure

Basis-trade activity can matter for market structure because the position connects cash markets, futures markets, financing markets, and dealer balance-sheet capacity. The trade can be relative-value in design, but the unwind can still create directional-looking pressure if many participants need to reduce similar exposures at the same time.

That is why funding liquidity is central to interpretation. A basis trade may remain stable while financing is available, collateral is accepted, and market depth is sufficient. The same trade can become more fragile when funding costs rise, margin terms tighten, or liquidity in one leg becomes thin.

Unwind pressure does not mean the market must move in one predetermined direction. It means the position may transmit stress across linked markets because cash securities, futures contracts, financing, and dealer capacity are no longer independent pieces.

Illustrative scenario: a futures contract trades rich to the related cash instrument, and relative-value participants build paired positions to capture the spread. If financing costs later rise or margin becomes more restrictive, the position may become less attractive. The pressure comes not only from the original price gap, but from the need to keep both sides financed and liquid.

Measurement and Proxy Caution

Basis-trade activity is difficult to measure cleanly from a single public number. Futures positioning, cash-market holdings, repo borrowing, fund disclosures, or regulatory data can each show part of the picture, but none of them should automatically be treated as the exact size of a true basis trade.

For example, a futures short may be part of a basis trade, a hedge, a relative-value book, or another strategy. A repo position may support a basis trade, but it can also finance other balance-sheet activity. The interpretation becomes stronger only when multiple indicators line up with the same structure.

Measurement rule: treat proxies as evidence fragments, not as complete proof. Exact claims about basis-trade size, leverage, current hedge-fund exposure, or regulatory effects require dated source verification before publication.

Common False Readings

A basis trade is useful market-structure evidence, but it is easy to overread. The presence of basis-trade activity does not automatically predict Treasury yields, equity direction, central-bank policy, or a liquidity crisis.

False reading 1: “basis trade means yields must move.” The trade may affect market pressure, but the yield path depends on broader demand, policy expectations, liquidity, positioning, and macro conditions.

False reading 2: “basis trade equals carry trade.” A basis trade focuses on a linked-price spread. A carry trade focuses on earning a funding or yield differential. The two can overlap, but they are not identical.

False reading 3: “basis-trade stress proves a crisis.” Stress in a basis trade can be a warning about funding and positioning pressure, but crisis interpretation requires broader confirmation from liquidity, volatility, credit, dealer capacity, and cross-market behavior.

Related Concepts

Basis trade is the general concept. Treasury basis trade covers the Treasury-specific version. Basis trading covers process language and broader terminology.

Cash and carry trade and carry trade are adjacent structures, but neither one replaces the broader basis-trade category. For stress transmission, carry trade unwind is more relevant when financing pressure forces crowded positions to reduce exposure.

FAQ

Is a basis trade the same as a Treasury basis trade?

No. A Treasury basis trade is a specific type of basis trade involving cash Treasury securities and Treasury futures. Basis trade is the broader category, and it can appear in other markets where related cash, spot, futures, or derivative prices diverge.

Why can basis trades create market pressure?

Basis trades can create market pressure because they often depend on financing, leverage, margin, and liquidity across more than one instrument. If funding becomes harder or one leg becomes less liquid, participants may need to reduce positions even if the original spread logic still appears reasonable.

Does basis-trade activity predict market direction?

No. Basis-trade activity can reveal positioning, funding dependence, and possible unwind pressure, but it does not predict market direction by itself. The interpretation depends on liquidity, funding conditions, market depth, positioning, and broader cross-market context.