A carry trade unwind happens when investors reduce or close positions funded through a lower-cost currency or financing source and held in higher-yielding exposure. It is a capital-flow, funding, and positioning mechanism. The unwind can be triggered by FX moves, narrower spreads, rising volatility, thinner liquidity, margin pressure, or crowded positioning, but it is not automatically a crash warning or market forecast.

Definition: A carry trade unwind is the reduction, closing, or forced exit of carry trade positions after the funding conditions, currency path, volatility environment, liquidity backdrop, or position crowding that supported the trade starts to move against it.

Key Points

- A carry trade unwind means positions are being reduced or closed, not merely that a carry trade exists.

- The pressure can come from FX moves, spread compression, volatility, weaker liquidity, margin calls, or crowded positioning.

- Leverage can turn a normal position reduction into a faster deleveraging sequence.

- Cross-asset spillover is possible, but the direction and severity depend on liquidity, leverage, positioning, and policy context.

- A carry trade unwind explains pressure transmission. It is not a standalone decision rule, guaranteed crash warning, or automatic recession indicator.

What Gets Unwound in a Carry Trade Unwind?

The starting point is a carry trade: investors fund exposure through a lower-cost currency or financing source and hold assets, currencies, bonds, equities, credit, or other positions that offer a higher expected return. The attraction is the spread, but the position is exposed to more than the spread alone.

What gets unwound is the combined package of funding, currency exposure, leverage, target exposure, and positioning. If the funding currency rises, the yield gap narrows, volatility increases, or liquidity becomes less forgiving, the trade can lose the conditions that made it attractive. Participants may then reduce exposure, buy back the funding currency, sell the target asset, cut leverage, or avoid adding to crowded positions.

Important distinction: The carry trade is the original structure. The carry trade unwind is the exit process. The unwind matters for market stress because many participants may try to reduce similar exposures while liquidity is becoming weaker.

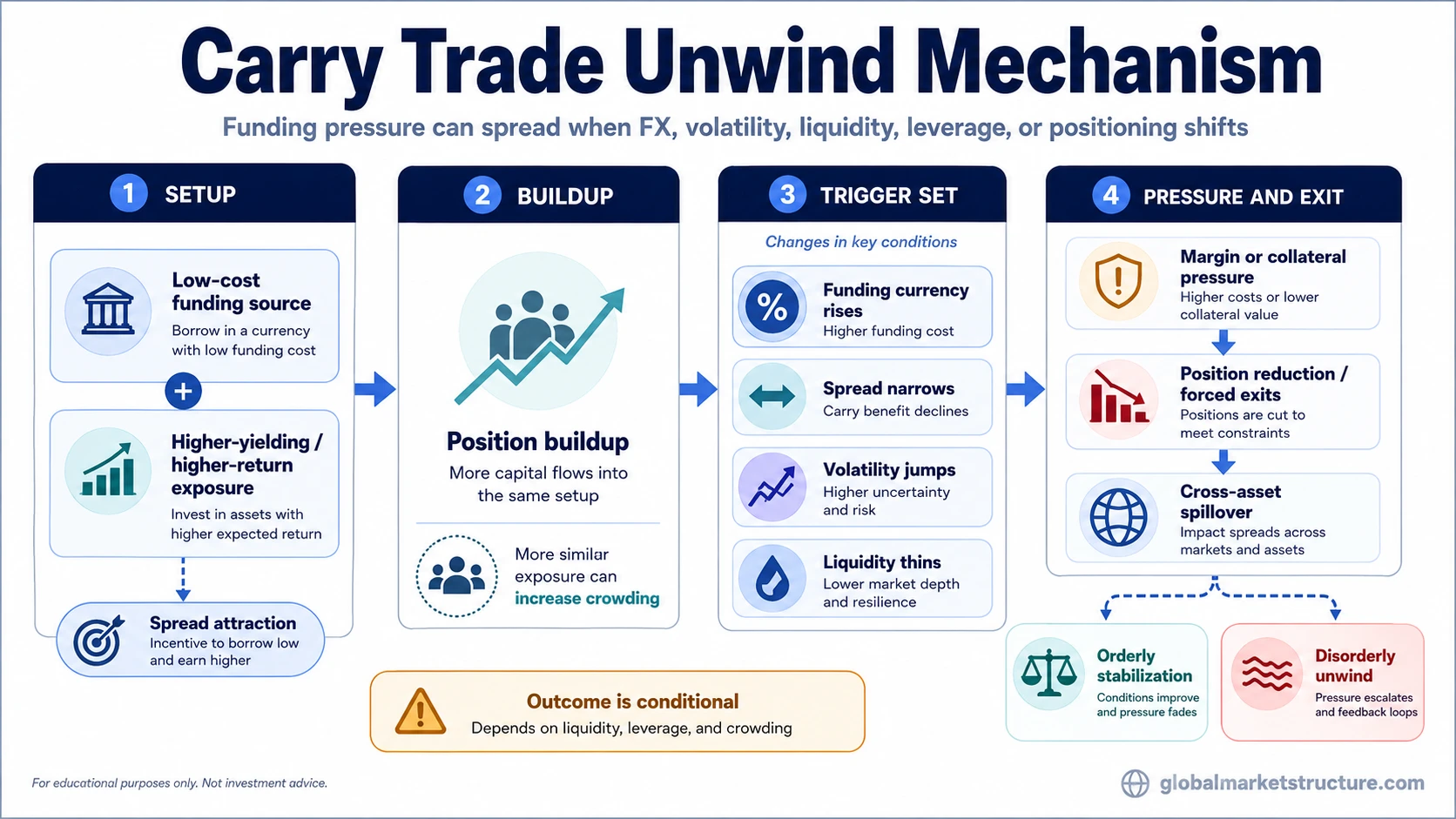

Carry Trade Unwind Mechanism

A carry trade unwind usually develops through a pressure chain rather than a single cause. The chain can begin with a small change in funding or FX conditions and become more serious if leverage, volatility, collateral pressure, or crowded positioning forces faster exits.

- Spread attraction: A lower-cost funding source makes higher-yielding or higher-returning exposure attractive.

- Position buildup: More investors enter similar trades because the spread, trend, or volatility backdrop appears favorable.

- Trigger shift: The funding currency strengthens, the spread narrows, volatility rises, policy expectations change, or liquidity weakens.

- Risk pressure: Losses, margin demands, collateral needs, or VaR constraints make the position harder to hold.

- Position reduction: Investors cut exposure, reduce leverage, buy back the funding currency, or sell target assets.

- Transmission: The unwind can spill into FX, equities, credit, volatility, bonds, and broader risk appetite if many participants are positioned similarly.

- Stabilization or disorder: The outcome depends on liquidity, leverage, policy response, balance-sheet strength, and how crowded the original trade was.

This sequence is conditional. A funding-currency move by itself does not prove that a large unwind is underway. The interpretation becomes more structural when currency moves, volatility, liquidity stress, position reduction, and cross-asset pressure appear together.

What Changes the Unwind Path?

The same carry trade unwind can remain orderly or become disorderly depending on which components shift at the same time. The table below separates the main drivers from their interpretation limits.

| Component | What Changes | Why It Matters | Interpretation Limit |

|---|---|---|---|

| Funding currency | The borrowed or funding currency strengthens. | Investors may need to buy back the funding currency or reduce exposure as funding becomes more expensive in effective terms. | A currency rally alone does not prove forced deleveraging. |

| Yield or rate spread | The return gap between funding and target exposure narrows. | The compensation for holding the trade becomes less attractive. | Spread compression can be gradual and does not always force exits. |

| Volatility | Price movement becomes larger or less predictable. | Risk models, margin requirements, and position limits can push investors to reduce exposure. | Volatility can rise for many reasons, so it must be read with liquidity and positioning. |

| Market liquidity | Depth weakens and trades move prices more easily. | Exit pressure can become more self-reinforcing when many participants reduce exposure at once. | Thin liquidity increases risk, but it does not define the trade by itself. |

| Leverage and collateral | Borrowed exposure becomes harder to maintain. | Margin calls, collateral needs, or internal risk limits can turn voluntary exits into forced selling. | The effect depends on balance-sheet strength and risk controls. |

| Crowded positioning | Many participants hold similar funding and target exposures. | Similar exits can amplify FX moves, asset selling, and volatility. | Crowding is difficult to observe directly and should be inferred cautiously. |

Why Carry Trade Unwinds Can Spread Across Markets

A carry trade unwind can become cross-asset because the trade is not only a currency position. It can connect funding markets, FX markets, equities, bonds, credit, volatility, and liquidity conditions. When investors reduce the target exposure and buy back the funding currency at the same time, pressure can appear in several places at once.

The spillover path is strongest when leverage is high, the funding currency move is sharp, liquidity is thin, and the target exposure is widely held. In that setting, losses in one part of the trade can force risk reduction elsewhere. A portfolio may sell equities, reduce credit exposure, cut emerging-market positions, or reduce volatility exposure even if the original stress began in FX funding.

Limitation: Spillover is possible, not guaranteed. A carry trade unwind can remain contained if positions are smaller, leverage is limited, liquidity remains functional, or policy conditions offset the pressure.

What a Carry Trade Unwind Does Not Prove

The phrase is often used during stressful market episodes, but it should not be read as a complete market signal. A carry trade unwind can help explain how pressure travels, but it does not automatically prove that every risk asset must fall or that a recession has started.

| Claim | Safer Interpretation |

|---|---|

| A carry trade unwind means a crash is certain. | No. It means funding and positioning pressure may be forcing exits. The outcome depends on liquidity, leverage, crowding, and policy response. |

| A stronger funding currency proves forced deleveraging. | No. It may be one input, but the stronger signal comes when FX, volatility, liquidity stress, and position reduction align. |

| All carry trades are the same. | No. FX-funded carry, volatility carry, credit carry, and basis or funding trades can share risk features but have different mechanics. |

| The unwind gives a direct trade instruction. | No. It is a market-structure explanation, not a buy, sell, short, or leverage instruction. |

How to Read a Carry Trade Unwind in Market Structure

A useful reading separates what is observed from what is inferred. Observed evidence can include a funding currency move, wider volatility, weaker liquidity, rising margin pressure, and risk-asset selling. Interpretation begins only after those signals are connected into a coherent pressure chain.

Observed: Funding currency strength, falling target exposure, wider volatility, thinner liquidity, or signs of deleveraging.

Interpreted: Participants may be reducing carry exposure because the original funding, spread, volatility, or positioning conditions have deteriorated.

Not proven: The unwind does not by itself prove a market crash, recession, policy mistake, or precise path for risk assets.

The practical reading is strongest when the evidence is multi-channel. Currency moves, volatility, liquidity, collateral pressure, and cross-asset risk reduction should be assessed together rather than treated as isolated signals.

Practical Scenario

A common scenario begins with investors borrowing in a low-yielding currency and holding higher-yielding assets while volatility is low. The spread appears attractive, and stable FX conditions make the trade easier to hold. Over time, similar positioning can build across funds, banks, and systematic strategies.

The unwind risk rises if the funding currency strengthens, the rate spread narrows, volatility rises, and liquidity becomes thinner. In that setting, some participants may cut exposure voluntarily, while others may reduce positions because margin, collateral, or risk-limit rules force them to do so.

Diagnostic sequence: First, identify the funding source and target exposure. Second, check whether the funding currency, spread, volatility, and liquidity conditions changed together. Third, look for evidence of position reduction or cross-asset stress. If only one input changed, the unwind interpretation remains weaker.

If many participants are positioned similarly, the exit process can amplify the original move. If liquidity remains strong and leverage is limited, the unwind may remain contained.

This scenario is illustrative, not a historical claim. It is designed to show the mechanism: carry trades can look stable while spread, FX, volatility, and liquidity conditions are aligned, then become fragile when those conditions shift together.

Carry Trade Unwind vs Nearby Concepts

Carry trade unwind sits near several related concepts, but it should not absorb all of them. The useful distinction is whether the page is explaining the original trade, the exit mechanism, a disorderly episode, a volatility-risk strategy, or a broader funding condition.

| Concept | Main Meaning | How It Differs From Carry Trade Unwind |

|---|---|---|

| Carry trade | The original structure of borrowing at lower cost to hold higher-yielding or higher-returning exposure. | The carry trade is the position structure. The unwind is the reduction or closing of that structure. |

| Carry trade unwind | The exit or deleveraging process when funding, FX, volatility, liquidity, or positioning conditions shift. | This is the core concept for understanding pressure transmission. |

| Carry trade crash | A sharper, more disorderly unwind with stronger feedback loops and broader stress. | A crash is a possible severe form of unwind, not the default outcome. |

| Volatility carry trade | A strategy or exposure that earns carry from selling or holding volatility risk under favorable conditions. | It can also unwind under stress, but it is not the same as FX-funded carry trade deleveraging. |

| Funding stress | Broader difficulty obtaining financing, rolling funding, or maintaining collateral. | Funding stress can contribute to an unwind, but it is wider than carry trade exits alone. |

Where the Yen Carry Trade Fits

Yen-funded structures are a common example in source-backed carry-unwind coverage because Japan has often been associated with low-rate funding conditions, but the yen example should not define the whole concept.

A yen-related unwind is one version of the broader mechanism: a funding currency changes direction, the economics of the trade deteriorate, volatility or margin pressure rises, and participants reduce exposure. Any named yen episode, policy catalyst, asset spillover, or estimate of positioning size should be treated as dated and source-backed rather than as an evergreen rule.

FAQ

What is a carry trade unwind?

A carry trade unwind is the reduction or closing of positions that were funded through a lower-cost currency or financing source and invested in higher-yielding or higher-returning exposure. The unwind can happen when FX, rates, volatility, liquidity, leverage, or positioning conditions move against the trade.

Why do carry trades unwind?

Carry trades can unwind when the funding currency strengthens, the yield spread narrows, volatility rises, liquidity weakens, margin pressure increases, or crowded positioning makes the trade harder to hold. The exact trigger can differ by market and regime.

Does a carry trade unwind always cause a market crash?

No. Some carry trade unwinds are orderly reductions in exposure. A crash-like outcome requires more severe conditions, such as heavy leverage, crowded positioning, thin liquidity, and forced exits occurring at the same time.

How is a carry trade unwind different from a carry trade crash?

A carry trade unwind is the general exit process. A carry trade crash is a more disorderly version where forced deleveraging and liquidity stress create sharper market moves. Not every unwind becomes a crash.

Why can yen strength affect carry trades?

Yen strength can affect yen-funded carry trades because investors who borrowed yen may face higher effective funding pressure or need to buy back yen while reducing target exposure. The effect depends on positioning, leverage, volatility, and liquidity.

How do volatility and margin pressure affect carry trade exits?

Higher volatility can raise the risk of holding leveraged positions and can trigger internal risk-limit reductions. Margin or collateral pressure can force investors to reduce exposure faster than they would under calmer liquidity conditions.

Final Interpretation

A carry trade unwind is most useful as a framework for understanding funding pressure, positioning exits, and cross-asset transmission. It should be interpreted with liquidity, leverage, volatility, policy expectations, and evidence of crowding. The concept explains how pressure can travel through markets, but it does not by itself prove a crash, a recession, a currency path, or a trade signal.