Funding stress is a market funding condition in which participants face greater difficulty obtaining, rolling, or maintaining financing at predictable cost. It can appear through higher funding costs, weaker collateral capacity, margin and haircut pressure, counterparty caution, or reduced balance-sheet availability. It is a pressure condition, not a guaranteed market-crash signal or automatic policy forecast.

Funding stress means financing pressure. The focus is not whether prices are moving up or down by themselves. The focus is whether market participants can keep financing positions, roll borrowing, post collateral, and access balance-sheet capacity without sudden cost or availability pressure.

Funding Stress Is / Is Not

The clearest way to define funding stress is to separate it from nearby terms that often appear in the same market environment. Funding stress can overlap with broader financial stress, but it has a narrower financing-access meaning.

| Funding stress is | Funding stress is not |

|---|---|

| Pressure in obtaining, rolling, or maintaining financing. | A personal-finance term about household budgeting or consumer anxiety. |

| A condition linked to collateral, margins, haircuts, repo costs, and counterparty caution. | The same thing as broad financial stress, which can include many market, credit, and volatility indicators. |

| A funding-market condition that can make financing-dependent positions harder to hold. | A direct prediction that markets must crash or that forced selling must happen. |

| A pressure channel that can interact with liquidity, leverage, and balance-sheet capacity. | The same thing as market liquidity, which focuses on trading without large price impact. |

| A condition that may affect carry, basis, and leveraged relative-value exposures. | A buy, sell, short, hedge, or leverage instruction. |

Where Funding Stress Fits in Market Structure

Funding stress sits inside the financing side of market structure. It is closely connected to funding liquidity, because both deal with the ability to access financing. The difference is that funding liquidity describes the financing capacity itself, while funding stress describes pressure on that capacity.

It also differs from market liquidity. Market liquidity asks whether an asset can be bought or sold without large price impact. Funding stress asks whether the holder of a position can finance that position under changing cost, collateral, and counterparty conditions.

This distinction matters because a market can appear liquid at the trading level while funding conditions are becoming less stable underneath. A participant may still be able to sell an asset, but the reason for selling may come from financing pressure rather than a changed view of the asset itself.

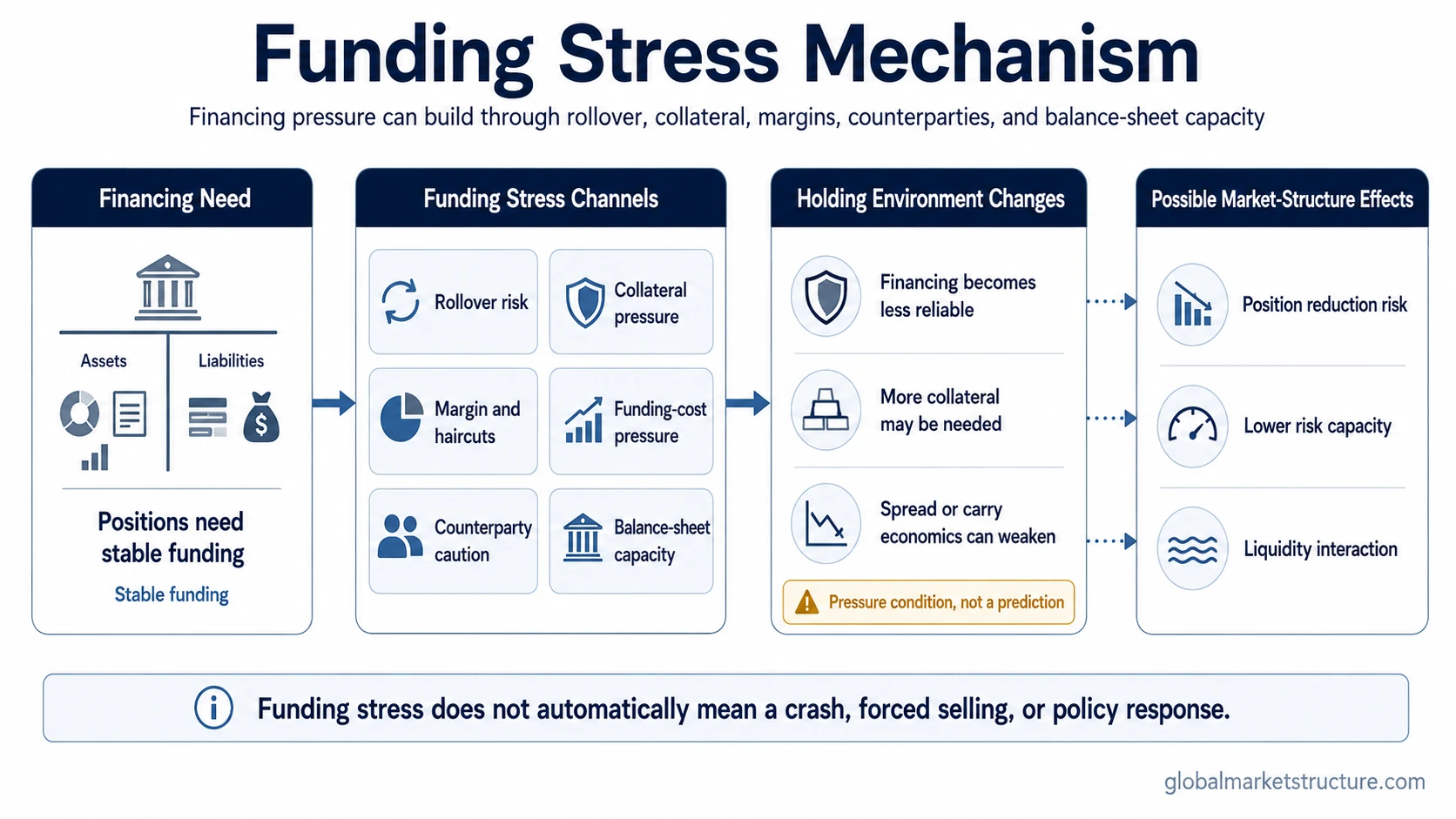

How Funding Stress Works

Funding stress usually develops through several connected channels. The channels do not need to appear in a fixed order, and none of them proves a crisis by itself. The point is that financing-dependent positions become more sensitive when the cost, availability, or reliability of funding changes.

| Channel | How it creates pressure | Why it matters |

|---|---|---|

| Rollover risk | Borrowing that previously rolled smoothly becomes harder, shorter, or more expensive to renew. | Positions that depend on continuous financing may need to be reduced or restructured. |

| Collateral pressure | Collateral becomes less acceptable, less valuable, or subject to larger discounts. | The same position may require more collateral support than before. |

| Margin and haircut pressure | Lenders demand more protection against price or credit risk. | Leverage becomes less stable even if the original investment idea has not changed. |

| Funding-cost pressure | The cost of financing rises relative to the return or spread being earned. | Carry, basis, and spread positions can lose attractiveness or become harder to maintain. |

| Counterparty caution | Participants become less willing to lend, intermediate, or extend balance sheet. | Financing availability can tighten even before a visible market breakdown. |

| Balance-sheet capacity | Dealers or lenders have less room or willingness to absorb financing demand. | The system becomes less able to cushion demand for funding. |

How Funding Stress Can Show Up

Funding stress can show up in several market-facing ways. A single indicator is not enough to define the whole condition, but repeated pressure across funding channels can make the signal more meaningful.

- Rising secured or unsecured funding costs: Financing becomes more expensive relative to the expected return from the position.

- Shorter or less reliable rollover: Borrowers may still obtain funding, but with less certainty, shorter terms, or tighter conditions.

- Higher collateral demands: More collateral is needed to support the same exposure.

- Wider haircuts: The lender applies a larger discount to collateral value, reducing effective borrowing capacity.

- Reduced counterparty willingness: Lenders and intermediaries become more selective, even before markets show broad visible stress.

- Greater pressure on leveraged exposure: Positions that depend on cheap and stable funding become more sensitive to small changes in cost or availability.

What Funding Stress Does Not Prove

Funding stress is often discussed during unstable market periods, but it should not be treated as a deterministic signal. It does not automatically prove that a crash is coming, that a central bank will respond, or that a specific asset must move in one direction.

The limitation is important: funding stress describes pressure in the financing environment. The market effect depends on size, duration, concentration, leverage, liquidity, policy backdrop, and whether the pressure remains isolated or spreads across participants and markets.

This is why funding stress should be read as a mechanism, not as a standalone forecast. It becomes more relevant when it interacts with weaker market liquidity, crowded positioning, falling collateral values, widening credit spreads, or reduced balance-sheet capacity.

Practical Scenario

A financing-dependent position may look stable when funding is cheap, collateral is accepted easily, and lenders are willing to roll exposure. If funding costs rise, haircuts increase, and counterparties become more cautious, the same position can become harder to maintain even if the original market view has not changed.

The important point is not that liquidation must happen. The important point is that the position becomes more sensitive to financing conditions. If many similar positions depend on the same funding channels, pressure can become more visible across related markets.

Funding Stress vs Financial Stress

Funding stress and financial stress are related, but they are not identical. Financial stress is the broader term. It can include volatility, credit spreads, equity-market weakness, banking pressure, risk aversion, and other system-wide indicators. Funding stress is narrower. It focuses on whether participants can obtain, roll, and maintain financing.

The distinction helps avoid over-reading the term. A market can show some funding pressure without a full financial-stress episode. A broad financial-stress episode, however, often includes funding stress because financing access is one of the channels through which pressure spreads.

Related Concepts

Funding stress is easier to understand when it is placed next to nearby market-structure concepts. Funding liquidity explains the financing capacity behind the system, while market liquidity explains the ability to transact in assets without large price impact.

It also connects to financing-dependent strategies such as carry trade and carry and roll-down, where the stability of funding costs and financing access can affect whether a spread, yield, or basis exposure remains attractive.

Core distinction: funding stress is not just a price move. It is the financing pressure that can change whether positions remain affordable, collateralized, and rollable under changing market conditions.

FAQ

Is funding stress the same as financial stress?

No. Funding stress is narrower. It focuses on pressure in financing access, rollover, collateral, margins, funding costs, and balance-sheet capacity. Financial stress is broader and can include credit, volatility, equity-market, banking, and other system-wide indicators.

Does funding stress always mean markets will crash?

No. Funding stress is a pressure condition, not a market forecast. It may matter more when it spreads across financing channels, affects leveraged participants, or interacts with weaker market liquidity, but it does not guarantee a crash or forced liquidation.

How is funding stress different from market liquidity?

Funding stress is about financing a position. Market liquidity is about trading an asset without large price impact. The two can interact, but they describe different parts of market structure.