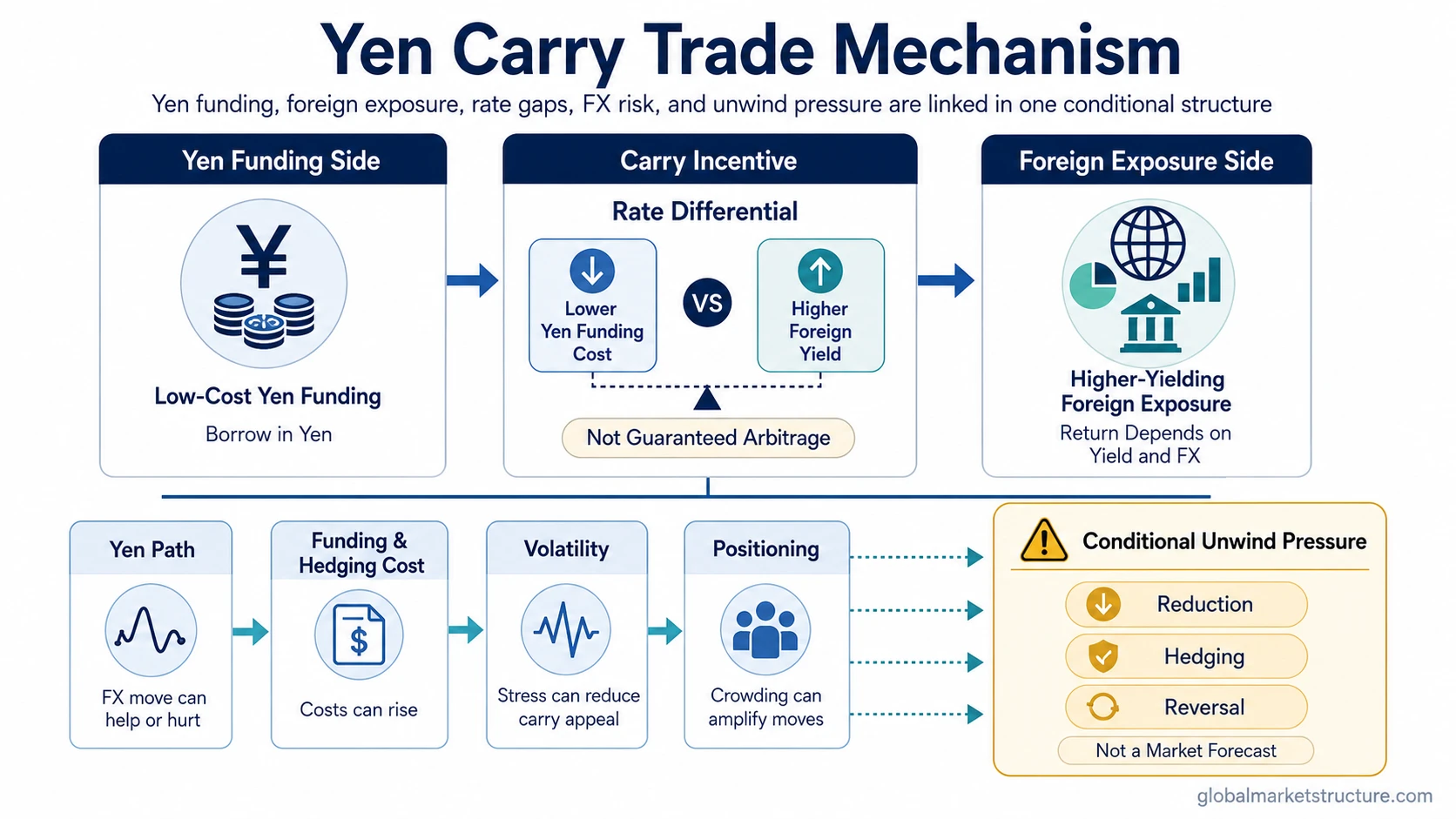

A yen carry trade is a yen-funded carry structure where low-cost yen funding is used to hold higher-yielding foreign-currency assets or exposures. The result depends on the rate gap, the yen’s exchange-rate path, funding costs, volatility, and positioning, so the structure is conditional rather than guaranteed arbitrage or a direct forecast for markets.

Definition: A yen carry trade uses the Japanese yen as the funding currency and places capital into higher-yielding foreign-currency assets or exposures. The expected carry comes from the yield difference, but the actual result can change when the yen strengthens, funding costs rise, volatility increases, or crowded positioning adjusts.

The yen carry trade belongs to the capital-flow and funding-currency side of market structure. It helps explain why rate differentials, currency stability, liquidity conditions, and risk appetite can interact across FX, bonds, equities, and broader risk assets without producing a mechanical one-way signal.

Key Points

- The yen is the funding side of the structure.

- Higher-yielding foreign-currency assets or exposures are the carry side.

- The rate gap matters only alongside FX movement, funding costs, volatility, and positioning.

- A yen carry trade unwind is a reduction or reversal process, not the same thing as the original carry structure.

What Is the Yen Carry Trade?

The yen carry trade is the yen-funded version of a broader currency carry trade. The basic idea is to borrow or fund in a lower-yielding currency and hold exposure linked to a higher-yielding currency, asset, or market.

The yen is commonly discussed as a funding currency when yen funding costs sit below available foreign yields. That does not make the trade risk-free. The carry advantage can be reduced or reversed if the yen appreciates, if funding becomes more expensive, if volatility rises, or if many participants reduce similar exposures at the same time.

The useful distinction is structural. The trade is not only about a rate gap. It also depends on whether the currency, financing, hedging, margin, and liquidity environment allows the exposure to remain attractive and maintainable.

How the Yen Carry Trade Works

The mechanism starts with yen funding. Capital is then placed into a higher-yielding foreign-currency exposure. The expected benefit comes from the difference between the low cost of yen funding and the higher return or yield on the foreign exposure.

The trade becomes more fragile when the yen rises against the target currency, when hedging costs increase, or when volatility makes leveraged or crowded exposure harder to maintain. A favorable yield spread can therefore coexist with rising risk if the FX or funding side moves against the trade.

Basic mechanism: yen funding creates the low-cost funding side, foreign exposure creates the yield side, the rate differential creates the carry incentive, and FX, funding, volatility, and positioning determine whether that incentive remains stable.

Yen Carry Trade Mechanism Table

The same yield gap can mean different things depending on surrounding conditions. A clean reading separates the channels instead of treating the yen carry trade as one single market signal.

| Channel | What Supports Carry | What Weakens Carry | Interpretation Boundary |

|---|---|---|---|

| Rate differential | Foreign yields remain meaningfully above yen funding costs. | The yield gap narrows or expected future rate paths change. | A rate gap is not enough without FX and funding stability. |

| Yen direction | The yen is stable or weak against the exposure currency. | The yen appreciates enough to offset the carry advantage. | A yen move alone does not prove a full market regime shift. |

| Funding and hedging cost | Borrowing, rollover, and hedging conditions stay manageable. | Funding costs rise or hedges become more expensive. | Funding pressure can change the trade even if yield spreads still look attractive. |

| Volatility | Low volatility supports confidence in maintaining carry exposure. | Higher volatility raises risk, margin pressure, and hedging demand. | Volatility is a condition, not a standalone forecast. |

| Positioning | Exposure remains balanced and adjustments are gradual. | Crowded positioning increases the risk of simultaneous reduction. | Exact positioning claims require data and dates before publication. |

| Liquidity and risk appetite | Markets remain willing to finance and hold risk exposure. | Risk appetite falls, liquidity thins, or balance-sheet capacity tightens. | Carry pressure can matter without proving a crisis. |

Why the Yen Carry Trade Matters for Market Structure

The yen carry trade can connect funding conditions, FX movement, capital flows, and broader risk appetite. When the structure is attractive, capital may favor higher-yielding markets. When the structure becomes less attractive, exposure may be reduced, hedged, or repriced.

That connection affects how market participants interpret changes in the yen, global yields, volatility, and cross-asset behavior. The concept is most useful as a funding and positioning mechanism, not as a prediction model for any single asset class.

A yen rally may pressure yen-funded exposure, but it may also reflect other drivers. A risk-asset selloff may coincide with carry adjustment, but it may also reflect growth, earnings, credit, policy, or liquidity concerns. The stronger reading comes from checking whether several conditions are moving together rather than assigning every market move to the carry trade alone.

What Can Weaken or Reverse the Trade

A yen carry trade weakens when the expected reward for holding the foreign exposure becomes smaller or harder to maintain. The most direct pressure comes from yen appreciation, because the funding currency rising against the exposure currency can offset the yield advantage.

The trade may also become less attractive when the rate differential narrows, funding costs rise, hedging becomes expensive, or volatility increases. These changes do not have to occur all at once. Even a shift in expected rate paths may reduce the perceived advantage before realized policy rates fully change.

Limitation: A weakening yen carry trade is not the same thing as an automatic market crash, a USD/JPY forecast, or a complete explanation for equities, bonds, or credit. It is one funding and positioning channel that becomes more informative when it lines up with volatility, liquidity, risk appetite, and cross-asset confirmation.

Yen Carry Trade vs Yen Carry Trade Unwind

The yen carry trade is the active funding structure. A yen carry trade unwind is the process of reducing, hedging, reversing, or forcibly adjusting that exposure. The unwind is therefore a later condition, not the definition of the trade itself.

An unwind can happen gradually if the carry advantage fades or more abruptly if currency movement, volatility, margin pressure, or liquidity stress forces participants to adjust at the same time. The key point is conditional pressure. The existence of carry exposure does not mean an unwind is inevitable, and an unwind does not automatically mean a systemic crisis.

The distinction helps prevent a common mistake: treating every yen move as proof that a large carry unwind is already underway. The interpretation becomes more defensible only when FX movement, volatility, funding pressure, and positioning behavior point in the same direction.

Common False Readings

One false reading is to treat the yen carry trade as guaranteed arbitrage. The rate differential can be attractive, but FX movement, funding costs, hedging costs, volatility, and position crowding can change the result.

Another false reading is to treat the yen as a complete risk-on or risk-off signal. Yen appreciation can pressure yen-funded exposure, but a currency move is not enough by itself to explain the whole market environment.

A third false reading is to treat carry pressure as a direct trading instruction. The structure can help classify funding sensitivity and cross-asset pressure, but it does not provide an entry, exit, target, or asset-level recommendation.

Simple Yen Carry Trade Scenario

A common scenario is that a wide rate gap makes yen funding look attractive while the yen is stable and volatility is low. Capital can remain comfortable in higher-yielding foreign exposure because the funding side is cheap and the FX side is not working against the structure.

The same exposure becomes harder to maintain if the yen strengthens, funding costs rise, or volatility jumps. The yield gap may still exist, but the total risk-reward of the structure changes because currency movement and financing conditions begin to offset the carry benefit.

The useful reading is conditional funding exposure, not yield spread alone. Yield matters, but the interpretation depends on the full mix of rates, FX, funding, volatility, positioning, and liquidity.

Related Carry Concepts

The broader currency carry trade concept explains the general funding-and-yield structure across currencies. The yen carry trade is the yen-funded version, so the funding currency is not interchangeable in the interpretation.

Volatility changes carry interpretation because stable funding and risk appetite often support carry exposure. A volatility carry trade is related through the broader carry family, but it is a different structure tied to volatility exposure rather than yen-funded foreign-currency exposure.

FAQ

What is the yen carry trade in simple terms?

A yen carry trade uses low-cost yen funding to hold higher-yielding foreign-currency assets or exposures. The expected benefit comes from the rate gap, but FX movement, funding costs, volatility, and positioning can change the result.

Is the yen carry trade guaranteed arbitrage?

No. The rate differential can be attractive, but yen appreciation, higher funding costs, hedging costs, volatility, and crowded positioning can reduce or reverse the expected carry benefit.

What is the difference between a yen carry trade and a yen carry trade unwind?

The yen carry trade is the active funding structure. A yen carry trade unwind is the reduction, hedging, reversal, or forced adjustment of that exposure.

Does a yen carry trade predict markets?

No. It can help interpret funding sensitivity and cross-asset pressure, but it is not a direct forecast for currencies, equities, bonds, credit, or risk assets by itself.