A currency carry trade is an FX position that uses a lower-yielding currency as the funding side and a higher-yielding currency as the exposure side. The intended return comes from the interest-rate differential, but that spread is only one part of the outcome. Exchange-rate movement, funding costs, volatility, liquidity, leverage, and crowded positioning can offset or overwhelm the carry.

From a market-structure perspective, the important point is not only that a currency carry trade may seek a yield spread. It can also affect cross-border capital flows, currency positioning, funding pressure, and risk-on or risk-off behavior when conditions change.

What Is a Currency Carry Trade?

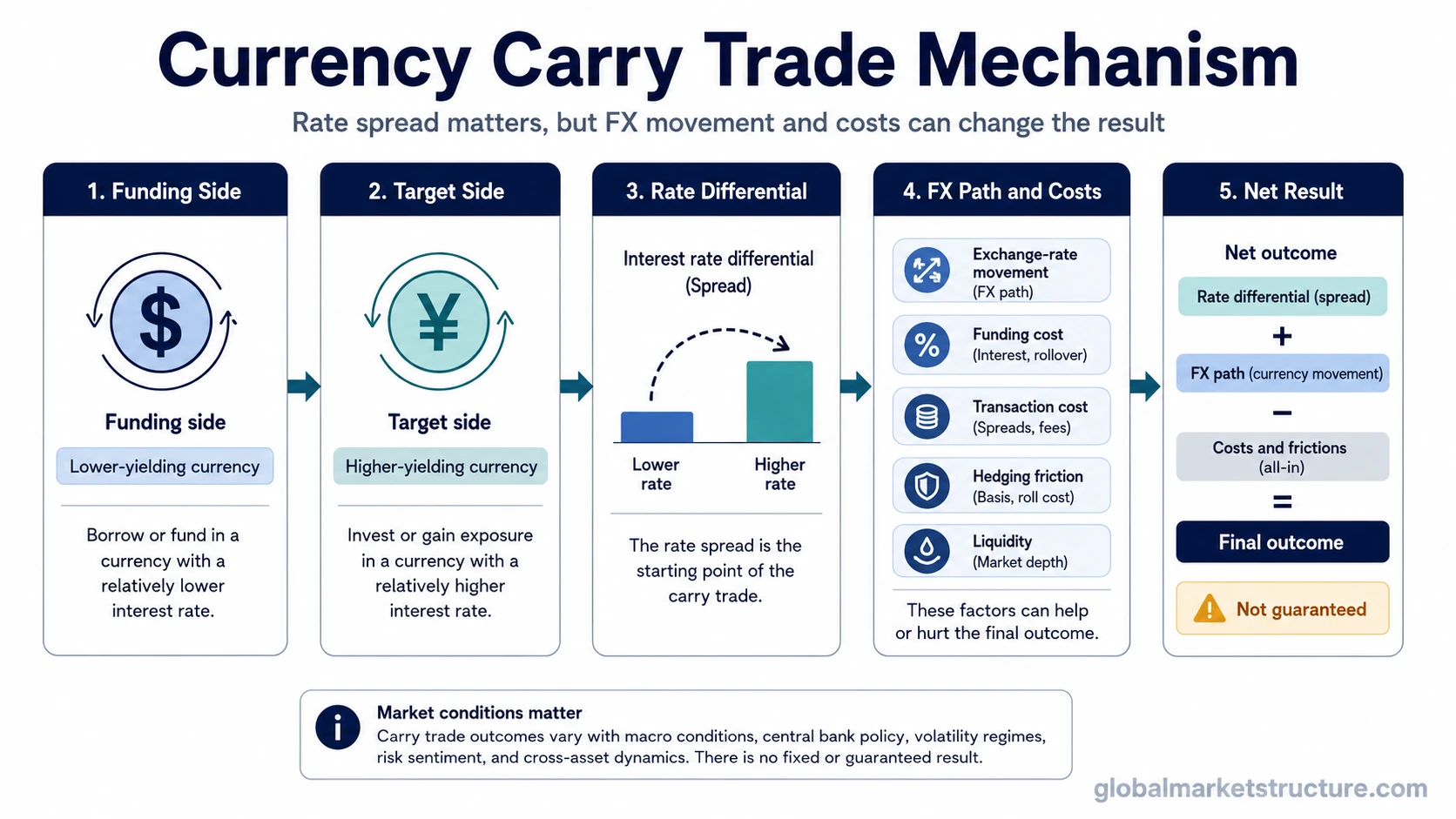

A currency carry trade is a foreign-exchange carry structure built around interest-rate differences between currencies. A participant uses a lower-yielding currency as the funding side and holds exposure to a higher-yielding currency as the target side. The higher-yielding side may provide carry, while the FX rate determines whether that carry is preserved, reduced, or reversed.

The lower-yielding currency is often called the funding currency. The higher-yielding currency is often called the target or investment currency. The trade works only if the interest-rate benefit is not erased by currency depreciation, rising funding costs, transaction costs, or a change in market conditions.

Key Points

- A currency carry trade seeks to benefit from the rate differential between two currencies.

- The FX move can offset or exceed the interest-rate benefit.

- Funding costs, volatility, liquidity, leverage, and crowded positioning can change the outcome.

- The concept matters for market structure because carry positioning can influence capital flows and unwind pressure.

How a Currency Carry Trade Works

The basic structure has two sides. On the funding side, the participant is exposed to a lower-yielding currency. On the target side, the participant holds exposure to a higher-yielding currency. If the target currency does not weaken enough to offset the interest-rate advantage, the position may collect positive carry.

The mechanism can be summarized as spread plus FX path minus costs. The spread is the rate differential. The FX path is the movement between the funding currency and the higher-yielding currency. Costs include funding, rollover, transaction, hedging, and financing frictions. Market stress can also change the ability to maintain the position.

This is why a currency carry trade is a specific FX expression of the broader carry trade concept. The general idea is to earn compensation from holding exposure with a positive carry profile, but the currency version adds direct exchange-rate risk.

Why the Rate Differential Is Not the Whole Outcome

The interest-rate differential is the visible attraction, but it is not a guarantee of return. A high-yielding currency can weaken enough to erase the income benefit. A funding currency can strengthen quickly when investors reduce risk. Funding costs can rise. Liquidity can deteriorate. Volatility can make the position harder to hold, especially if leverage or crowded positioning is involved.

The key limitation is that positive carry is earned over time, while FX losses can arrive quickly. A small rate advantage can be overwhelmed by a large exchange-rate move, a volatility shock, or a forced reduction in risk exposure.

Main Components of a Currency Carry Trade

A currency carry trade is easier to understand when its parts are separated. The rate spread is only one component. The full structure also depends on exchange rates, funding conditions, liquidity, volatility, and positioning.

| Component | Role in the structure | What can change the outcome |

|---|---|---|

| Funding currency | The lower-yielding currency used as the funding side of the structure. | A sharp rise in the funding currency can create losses on the FX side. |

| Higher-yielding currency | The target currency that provides the higher rate or yield exposure. | Depreciation of the higher-yielding currency can offset the carry benefit. |

| Interest-rate differential | The spread that creates the intended carry. | Policy changes, rate expectations, or funding costs can reduce the spread. |

| Exchange-rate movement | The FX path that determines whether carry is preserved or lost. | A currency reversal can dominate the interest-rate benefit. |

| Funding cost | The cost of maintaining the funding side and any financing attached to the position. | Higher financing costs can reduce or eliminate net carry. |

| Volatility | The movement environment that affects drawdowns, margin pressure, and holding risk. | Higher volatility can make the position less stable even if the rate spread remains positive. |

| Liquidity | The ability to enter, maintain, or reduce exposure without large price impact. | Weaker liquidity can amplify FX moves and make exits more costly. |

| Positioning and crowding | The degree to which many participants hold similar exposure. | Crowded positioning can increase unwind pressure when conditions reverse. |

Currency Carry Trade vs Carry Trade vs Yen Carry Trade

A currency carry trade should be separated from nearby carry concepts because each page has a different role.

Currency carry trade: the FX-specific version. It focuses on funding currency, higher-yielding currency, rate differential, exchange-rate movement, and currency-positioning risk.

Carry trade: the broader concept. It can include FX, fixed income, basis trades, volatility structures, and other exposures where positive carry is part of the thesis.

Yen carry trade: a yen-specific expression of FX carry. It belongs in a separate discussion because the yen can play a distinct funding-currency role in some market regimes.

The unwind stage is also separate. A carry trade unwind focuses on forced reduction, deleveraging, FX reversal, volatility, and liquidity pressure after the structure becomes vulnerable.

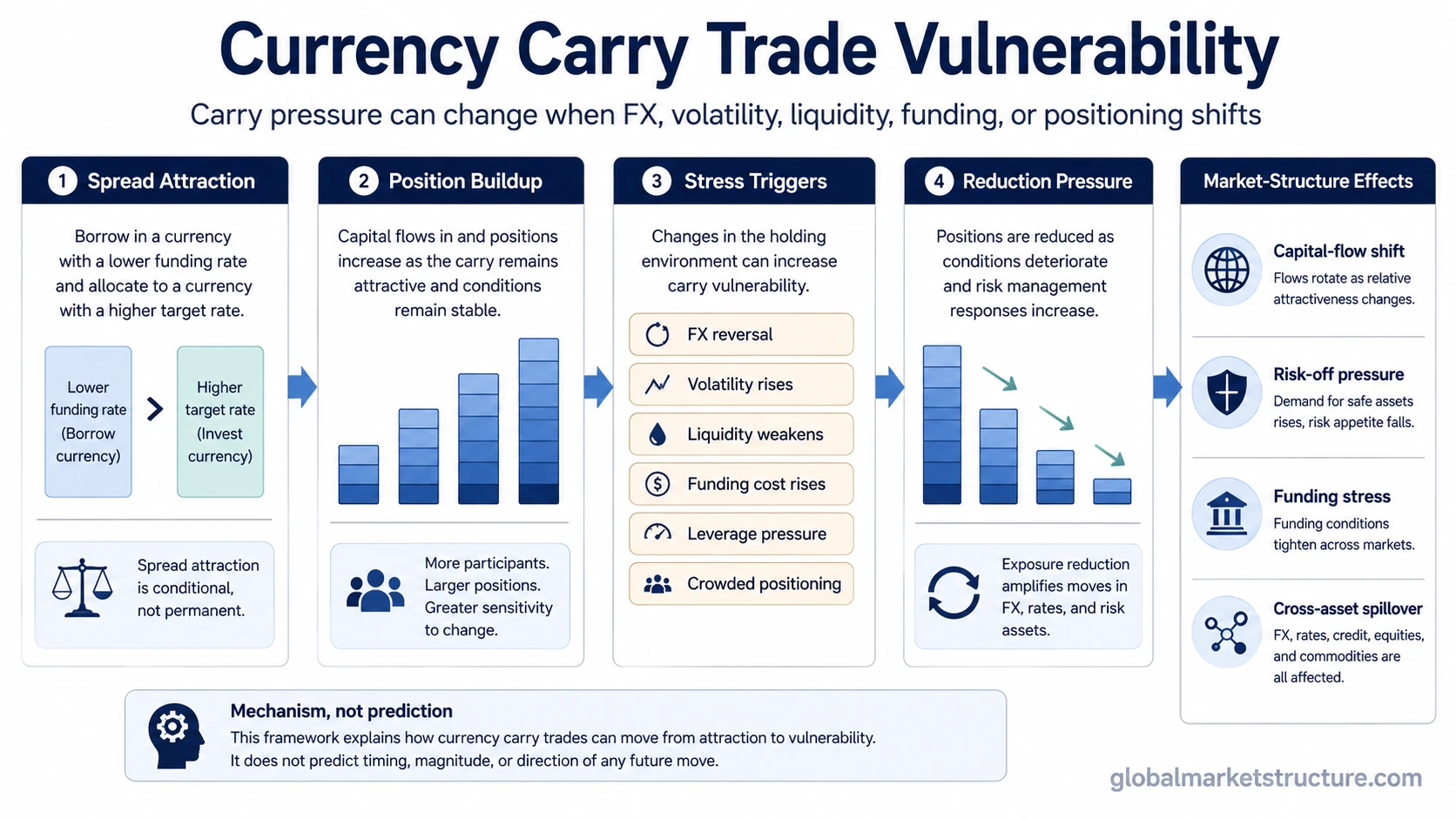

When Currency Carry Trades Become Vulnerable

Currency carry trades become more vulnerable when the conditions supporting the spread begin to weaken. A policy surprise can change rate expectations. A funding currency can strengthen during a risk-off move. A higher-yielding currency can fall when investors reassess growth, inflation, external balances, or political risk.

Volatility also matters. Carry trades often depend on the ability to hold exposure while the rate differential accumulates. If volatility rises, drawdowns can become harder to absorb. If liquidity deteriorates, reducing exposure can become more difficult. If positioning is crowded, many participants may try to reduce similar exposure at the same time.

Funding pressure is another vulnerability. When funding liquidity tightens, leveraged or balance-sheet-sensitive participants may have less room to maintain carry exposure. This can turn a slow income-oriented structure into a faster risk-reduction process.

Practical Scenario: When Positive Carry Can Still Lose

Consider a generic scenario where a lower-yielding currency funds exposure to a higher-yielding currency. The rate spread is positive, so the structure appears attractive from a carry perspective. For a while, the higher-yielding currency is stable, volatility is low, and funding costs are manageable.

The outcome changes if the higher-yielding currency starts to weaken. The interest-rate benefit may still exist, but the FX loss can become larger than the carry earned. If volatility rises at the same time, risk limits may tighten. If funding costs increase, the net spread may shrink. If many participants hold similar exposure, the same FX move can create broader unwind pressure.

This scenario is illustrative, not a current market call. It shows why the carry spread and the FX path must be evaluated together.

Why Currency Carry Matters for Global Market Structure

Currency carry matters because it can connect interest-rate differentials, FX markets, capital flows, and risk appetite. When carry conditions are attractive and volatility is low, capital may flow toward higher-yielding currencies. When volatility rises or funding conditions change, the same positioning can become a source of pressure.

The market-structure value comes from watching the transition. A currency carry trade is not only a spread calculation. It is also a positioning structure that may reveal how investors are using funding currencies, how they are expressing risk appetite, and where stress may appear if conditions reverse.

This is especially important when FX moves coincide with changes in liquidity, credit conditions, equity risk appetite, or cross-asset volatility. Currency carry can then become one part of a broader risk-on or risk-off environment rather than an isolated foreign-exchange trade.

Common Misunderstandings

Misunderstanding 1: Positive carry means the trade is profitable. Positive carry only describes the rate advantage before the full FX path, costs, and risk conditions are considered.

Misunderstanding 2: The higher-yielding currency is automatically better. A higher yield can reflect higher inflation, external risk, policy uncertainty, or other compensation for risk.

Misunderstanding 3: Currency carry is a trade signal. A rate differential is a structural input, not a standalone buy or sell instruction.

Misunderstanding 4: Currency carry risk is only about exchange rates. FX movement is central, but volatility, liquidity, leverage, funding cost, and crowding can also change the outcome.

Related Concepts

To place currency carry trade inside the broader carry family, start with the broader carry trade concept, then separate the FX-specific version from yen-specific carry and unwind pressure.

- Yen carry trade explains the yen-specific version of currency carry.

- Volatility carry trade explains carry built around volatility risk premium rather than currency-rate differentials.

- Funding liquidity helps explain why financing access and balance-sheet pressure can affect carry structures.

- Carry trade unwind explains what can happen when carry positioning is reduced under pressure.

FAQ

What is a currency carry trade in simple terms?

A currency carry trade is an FX structure that uses a lower-yielding currency as the funding side and a higher-yielding currency as the exposure side. The intended benefit comes from the rate difference, but the final outcome also depends on exchange-rate movement and costs.

How is a currency carry trade different from a broader carry trade?

A currency carry trade is the foreign-exchange version of carry. A broader carry trade can include other asset classes or structures where return depends partly on holding exposure with positive carry.

Why can a currency carry trade lose money even when the rate spread is positive?

It can lose money if the higher-yielding currency weakens, the funding currency strengthens, funding costs rise, volatility increases, liquidity deteriorates, or crowded positioning creates forced reduction pressure.

Is a yen carry trade the same as a currency carry trade?

No. A yen carry trade is a specific type of currency carry trade where the yen acts as the funding currency. Currency carry trade is the broader FX category.