Capital flows are cross-border movements of money used for investment, financing, asset allocation, lending, or balance-of-payments activity. In market-structure analysis, they matter because they can pressure currencies, yields, liquidity conditions, risk appetite, and positioning without becoming direct forecasts.

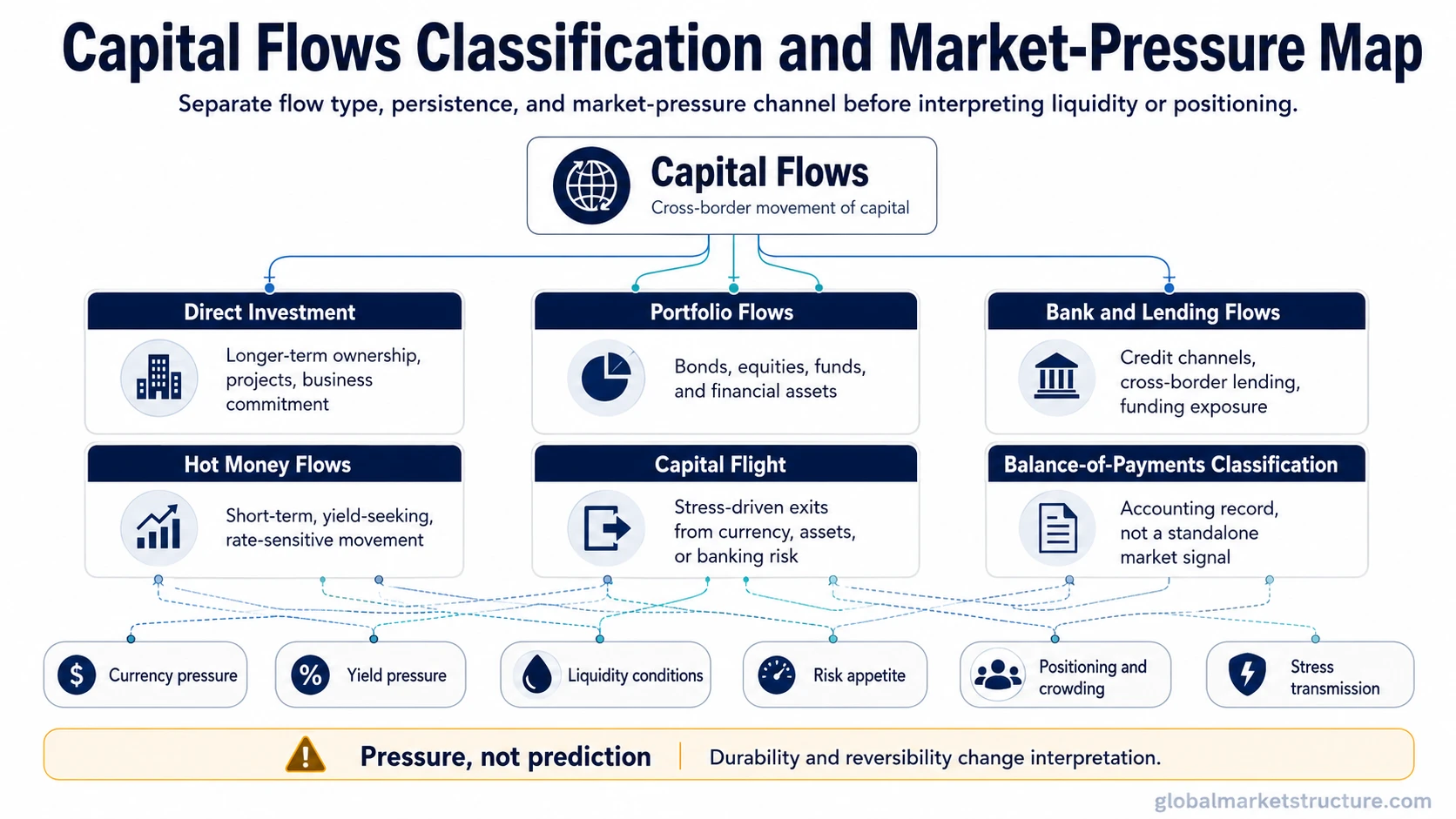

Capital flows describe the movement of capital between countries, markets, sectors, or asset classes. The term can include foreign direct investment, portfolio investment, bank lending, credit flows, short-term speculative movement, and stress-driven outflows.

The market impact depends on where the capital comes from, where it goes, how stable it is, and whether the flow is supported by long-term allocation or short-term positioning.

What Capital Flows Mean

Capital flows are not one single signal. A long-term investment into productive assets, a bond-fund allocation, a bank-lending channel, and a fast reversal of speculative capital can all involve cross-border money movement, but they do not carry the same market meaning.

The broad concept is useful because it connects macro conditions with observable market pressure. When capital moves into a country or asset class, it may support demand for that currency, compress yields, ease liquidity conditions, or strengthen risk appetite. When capital moves out, the opposite pressure can appear, especially if the outflow is fast, concentrated, or driven by funding stress.

The important distinction is that capital movement creates pressure, not certainty. A flow can support an existing trend, reinforce a macro regime, or expose crowding, but price direction still depends on valuation, policy, liquidity, positioning, and the response of other market participants.

Main Types of Capital Flows

Capital-flow interpretation starts with classification. The same headline phrase can refer to durable investment, portfolio allocation, short-term speculation, lending channels, or stress exits. Each type affects markets through a different mechanism.

| Flow type | What it describes | Market-structure interpretation | Main limitation |

|---|---|---|---|

| Foreign direct investment | Capital committed to businesses, production, ownership stakes, or long-term projects. | Usually more stable and tied to longer-term confidence, growth expectations, or strategic allocation. | It may not explain short-term asset-price pressure. |

| Portfolio flows | Capital moving into or out of equities, bonds, funds, or other financial assets. | Can affect yields, equity demand, currency pressure, and risk appetite more quickly than direct investment. | It can reverse when rates, policy expectations, or risk conditions change. |

| Banking and lending flows | Cross-border credit, loans, funding channels, and balance-sheet exposure. | Can transmit liquidity conditions and stress across regions. | The risk may be hidden until funding conditions tighten. |

| Short-term or hot money flows | Fast-moving capital seeking yield, carry, safety, or momentum. | Can intensify currency moves and positioning pressure. | High reversibility can make the signal fragile. |

| Capital flight or stress flows | Capital leaving because of perceived economic, political, currency, or financial-system risk. | Can reveal rising stress and falling confidence. | It should not be treated as a complete forecast without broader evidence. |

| Balance-of-payments classification | Accounting categories used to record cross-border transactions. | Useful for separating economic classification from market interpretation. | Accounting classification alone does not explain positioning or market timing. |

How Capital Flows Affect Currencies, Yields, and Liquidity

Capital flows move through demand, funding, and risk-allocation channels. When investors move capital into a market, they often need local currency, local securities, or local credit exposure. That can create demand for the destination currency, increase demand for bonds or equities, and change the liquidity available to local markets.

Currency pressure is often the easiest channel to observe. Cross-border inflows can support a currency when foreign investors need to buy it to gain exposure. Outflows can pressure a currency when investors sell local assets or move capital back into another currency. The dedicated currency channel belongs on capital flows and exchange rates, but the broad entity concept starts with this simple pressure mechanism.

Bond yields can also respond to capital movement. Strong foreign demand for local bonds can help compress yields, while reduced demand or forced selling can add upward pressure. The interpretation depends on whether the flow reflects confidence, yield-seeking behavior, defensive demand, or stress-driven repositioning.

Liquidity conditions are affected because flows change who is supplying capital and how easily risk can be financed. A market supported by steady inflows may look stable while incremental demand remains strong. It can become more fragile if the main sources of new buying are already crowded, rate-sensitive, or highly reversible.

Capital Flows vs Fund Flows, Hot Money, and Balance-of-Payments Categories

Capital flows are the broad concept. Fund flows are narrower because they usually describe money moving into or out of funds, products, or investment vehicles. Fund-flow data can be useful, but it is only one visible slice of the broader capital-flow picture.

Hot money flows are a specific subset of capital flows. They are usually shorter-term, more rate-sensitive, and more reversible than long-term capital allocation. This matters because a market supported by hot money can behave differently from one supported by durable direct investment or long-horizon portfolio allocation.

Balance-of-payments categories record capital movement through formal economic accounts. The financial account balance of payments is useful for understanding how cross-border financial assets and liabilities are recorded. That accounting structure is related to capital-flow analysis, but it is not the same as interpreting market pressure, crowding, or reversibility.

How to Interpret Capital Flows in Market Structure

Useful capital-flow analysis asks what kind of capital is moving, how persistent the movement is, and whether the flow is creating durable sponsorship or crowded exposure. A large inflow can support a market, but the quality of that support depends on who is buying, why they are buying, and how quickly they could leave.

Horizon: Long-term direct investment usually carries different information than short-term speculative allocation.

Source: Domestic savings, foreign portfolio investors, banks, reserve managers, and leveraged investors can create different pressure.

Destination: Flows into bonds, equities, credit, currency, or real assets can transmit through different market channels.

Stability: Stable flows can reinforce a regime, while reversible flows can increase fragility.

Concentration: A flow concentrated in one crowded market or theme can create reversal risk if incremental demand weakens.

Positioning is the bridge between flow data and market behavior. If capital has already moved heavily into one side of a market, the next phase depends less on the historical flow and more on whether new sponsorship remains. Crowding can raise reversal risk, but crowding alone is not a reversal signal.

A capital-flow scenario is also not the same as confirmed market direction. Flow pressure should be read with policy conditions, currency behavior, yield moves, credit stress, liquidity depth, and cross-asset confirmation.

Common Capital-Flow Misreads

Misread 1: Flow direction equals future price direction. Inflows can support demand, but markets can still fall if valuations, policy, earnings expectations, liquidity, or positioning overwhelm the flow.

Misread 2: Fund-flow headlines explain the whole capital-flow picture. Fund flows may show one visible channel, but they do not capture all direct investment, bank lending, balance-sheet activity, or private cross-border movement.

Misread 3: Crowding means immediate reversal. Crowding can make a move fragile, but reversal usually requires a catalyst, loss of incremental demand, funding pressure, or confirming market behavior.

Misread 4: Capital flows are a policy conclusion. Capital-flow analysis can show pressure and transmission, but it does not automatically prescribe policy, allocation, or market action.

A Simple Capital-Flow Scenario

Imagine a market receiving steady foreign inflows into local bonds and equities. The inflows can support the currency, help compress yields, and improve risk appetite while investors continue adding exposure.

The interpretation changes if the same inflow becomes crowded, rate-sensitive, or dependent on a narrow group of buyers. If the yield advantage fades or liquidity conditions tighten, the earlier flow support may become less reliable. The issue is not that inflows were bullish or bearish by themselves. The issue is whether the sponsorship remains durable or becomes reversible.

Related Capital-Flow Concepts

Capital flows provide the broad entity layer for understanding cross-border movement of money. Fund flows narrow the focus to investment vehicles and product-level allocation. Hot money flows isolate the short-term, reversible part of the capital-flow spectrum. Financial-account classification explains how cross-border financial transactions are recorded.

For product-level allocation: use fund flows when the question is about money moving into or out of investment funds.

For fast-moving reversible capital: use hot money flows when the question is about short-term, rate-sensitive, or speculative movement.

For currency pressure: use capital flows and exchange rates when the question is how cross-border movement affects FX demand.

For accounting classification: use the financial account balance of payments when the question is how financial assets and liabilities are recorded.

FAQ

Are capital flows the same as fund flows?

No. Capital flows are broader cross-border movements of money. Fund flows are narrower and usually describe money moving into or out of investment funds, products, or vehicles.

Do capital inflows always strengthen a market?

No. Inflows can support demand, liquidity, or currency pressure, but the final market effect depends on valuation, policy, positioning, liquidity, and whether the flows are durable or reversible.

Why do short-term capital flows matter?

Short-term flows can move quickly when rates, currency expectations, funding conditions, or risk appetite change. That reversibility can make markets more fragile when positioning becomes crowded.

Are capital flows a forecast?

No. Capital flows are evidence of pressure and allocation behavior. They can support an interpretation, but they should not be treated as a direct prediction of future price direction.