Fund flows are the net movement of money into or out of mutual funds, ETFs, asset classes, sectors, issuers, or fund categories over a defined period. In market-structure analysis, fund flows help show where allocation pressure is building or leaving, but they do not prove future market direction by themselves.

A fund can receive inflows when investors add money and experience outflows when investors redeem money. The useful question is not only whether money moved in or out. The stronger question is whether the movement is persistent, concentrated, broad, passive, active, risk-seeking, defensive, or simply short-term churn.

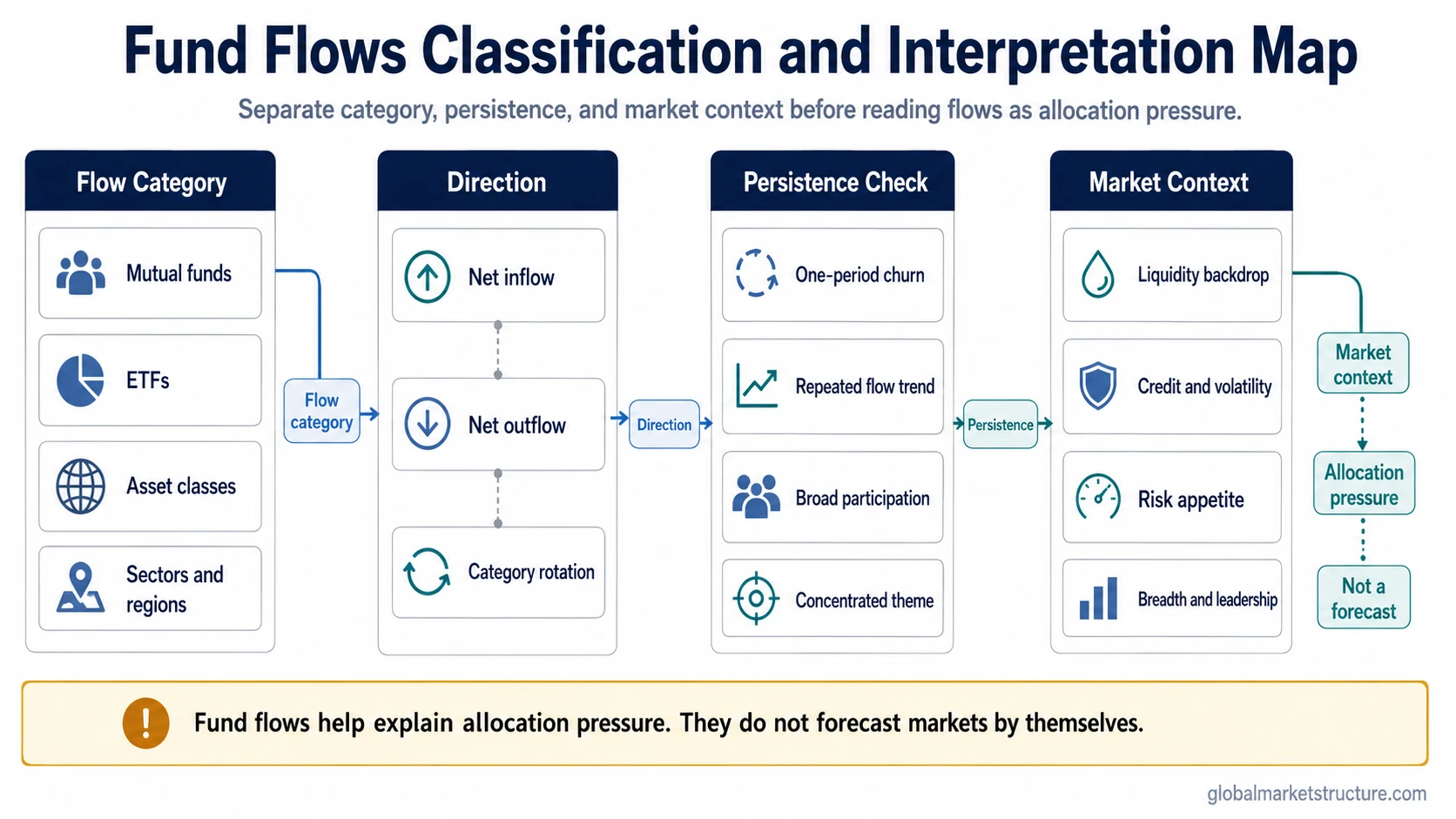

Fund Flows Definition

Fund flows measure money moving into or out of investment funds over a specific period. The fund may be a mutual fund, ETF, sector fund, bond fund, money market fund, commodity fund, active strategy, passive index product, or another pooled investment vehicle.

- Net inflow: more money enters the fund or category than leaves during the measurement period.

- Net outflow: more money leaves the fund or category than enters during the measurement period.

- Flow period: the time window being measured, such as daily, weekly, monthly, quarterly, or longer.

- Flow category: the grouping used to interpret the movement, such as equities, bonds, sectors, regions, themes, active funds, passive funds, or ETFs.

Fund flows are most useful as evidence of allocation behavior and positioning pressure. They are weakest when treated as a direct forecast, a performance signal, or proof of why every investor acted.

Key Points About Fund Flows

- Fund flows show where money is entering or leaving funds, ETFs, asset classes, sectors, or categories.

- Inflows can reflect demand, rebalancing, passive allocation, or delayed response to prior performance.

- Outflows can reflect risk reduction, reallocation, liquidity needs, or rotation into another category.

- One-period flow data can be noisy. Persistent flows often matter more than isolated weekly or monthly changes.

- Fund flows do not automatically predict returns, confirm investor intent, or define a market regime.

How Fund Flows Are Measured

Fund flows are usually measured over a defined reporting window. Depending on the fund type and data source, the measurement may reflect subscriptions, redemptions, ETF creations and redemptions, or other reported asset movements used to estimate how much net money entered or left a fund or category.

The exact method can differ by data source, fund type, timing, category definition, and reporting convention. For that reason, fund-flow analysis should separate the direction of the flow from the confidence of the measurement. A broad category flow, an ETF-specific flow, and a mutual-fund report may describe related behavior, but they are not always measuring the same thing in the same way.

For evergreen market interpretation, the most important inputs are usually the flow direction, size, timeframe, category, persistence, and surrounding market context. Current figures, provider-specific methodology, and official reporting caveats should be checked against the relevant data source when exact numbers are used.

Main Fund-Flow Categories

Fund-flow data becomes more useful when the category is clear. A headline flow number without category context can blur very different behaviors into one figure.

| Flow type | What it measures | Useful context | Main limitation |

|---|---|---|---|

| Mutual fund flows | Money entering or leaving mutual funds | Longer-horizon allocation behavior and category demand | Can be slower, delayed, or affected by reporting timing |

| ETF flows | Money entering or leaving exchange-traded funds | Theme demand, sector rotation, asset-class exposure, and passive channels | Can reflect trading, hedging, arbitrage, or short-term positioning |

| Asset-class flows | Money moving into or out of broad groups such as equities, bonds, commodities, or money markets | Risk appetite, liquidity preference, defensive allocation, and broad portfolio shifts | Too broad to explain investor intent on its own |

| Sector or theme flows | Money moving into sectors, regions, industries, or themes | Leadership, crowding, rotation, and narrative concentration | Can lag price performance or reflect passive index demand |

| Active and passive flows | Money moving through discretionary active products or index-linked passive products | Channel-specific demand and rebalancing behavior | Does not always reveal conviction, because passive flows can be mechanical |

Why Fund Flows Matter for Positioning and Market Pressure

Fund flows can show where exposure is being added or reduced across the market. Sustained inflows into equity funds may suggest that investors are increasing risk exposure. Sustained inflows into money market funds or defensive bond categories may suggest a stronger preference for liquidity, income, or capital preservation.

The market-pressure value comes from the combination of flow direction, category, persistence, and price behavior. If money keeps entering one theme while price momentum is already strong, the flow can support demand but may also point to crowded enthusiasm. If money leaves a category while prices stop falling, the flow may show capitulation risk, lagged redemption pressure, or a rotation already reflected in price.

Fund flows are therefore better read as positioning evidence than as a stand-alone signal. They help frame questions such as:

- Where is exposure being added?

- Where is exposure being reduced?

- Is the movement broad or concentrated?

- Is the flow persistent or temporary?

- Does the flow confirm or conflict with price, credit, liquidity, and risk-appetite signals?

Persistence Matters More Than One-Period Churn

A single flow reading can be misleading. Weekly or monthly movements can reflect rebalancing, tax timing, model allocation, ETF creation and redemption activity, or a reaction to prior market moves. A short burst of inflows does not automatically show durable conviction.

Persistent flows can be more informative because they suggest that allocation behavior is continuing across multiple reporting windows. Multi-week or multi-month inflows into a category may show a stronger shift in demand than one isolated print. Persistent outflows can show sustained pressure, but they still need context because money may be rotating into another category rather than leaving risk assets entirely.

The stronger interpretation comes from sequence. A flow pattern becomes more meaningful when it persists, aligns with broader market behavior, and appears in a category where the flow channel can plausibly affect liquidity, positioning, or market pressure.

Common False Reading: Flows Are Not Forecasts

Inflows are not automatically bullish, and outflows are not automatically bearish. A fund can receive inflows after a strong rally because investors are chasing performance. Another fund can see outflows near a low because investors are redeeming after losses. The flow direction alone does not reveal whether the next market move will continue or reverse.

Fund flows also do not directly measure asset performance. A fund can gain assets because of price appreciation, receive new investor money, lose assets through redemptions, or change through a mix of these forces. Market interpretation should avoid treating asset growth, flow direction, and price return as interchangeable.

The safest reading is conditional. Fund flows can strengthen an interpretation when they align with price, liquidity, breadth, credit conditions, volatility, sector leadership, and broader risk environment. They become weaker when the reading depends on one flow number alone.

Fund Flows Versus Related Flow Concepts

Fund flows sit inside the broader capital-flow and positioning universe, but they are not identical to every type of money movement.

| Concept | How it differs from fund flows | Why the distinction matters |

|---|---|---|

| Capital flows | Broader movement of capital across borders, accounts, asset classes, institutions, and economies | Fund flows can be one channel of allocation behavior, but not all capital movement is fund flow |

| Safe-haven flows | Defensive movement toward assets perceived as safer during stress or risk-off conditions | Some fund flows may reflect defensive demand, but safe-haven behavior depends on the risk environment and asset destination |

| Active vs passive fund flows | Separates discretionary manager allocation from index-linked or rules-based passive channels | Passive flows can be mechanical, while active flows may reflect manager preference, but neither should be treated as pure intent without context |

This distinction prevents a common category error. Fund flows can help interpret allocation pressure, but they do not replace broader capital-flow analysis, risk-off flow analysis, or channel-specific active and passive flow interpretation.

Illustrative Scenario: Risk-On Rotation Versus Defensive Flow Shift

A market may show strong inflows into equity ETFs while money leaves defensive bond funds. The tempting interpretation is that investors are turning risk-on and that equities should keep rising. That reading is incomplete if the flows are only one-week movements after a large equity rally.

The interpretation becomes stronger when inflows persist across several equity categories, breadth improves, credit spreads remain stable, and the liquidity backdrop supports risk appetite. The weaker case would be concentrated inflows into one crowded theme while credit weakens, volatility rises, or broader participation deteriorates.

A defensive shift can work the same way. Money moving into money market funds or high-quality bond categories may suggest caution, but the interpretation becomes stronger only when it aligns with risk-off behavior across credit, yields, volatility, currency pressure, or market breadth.

How to Read Fund Flows in Market-Structure Context

A clean fund-flow read separates measurement from interpretation. The measurement says money moved into or out of a defined fund, category, or asset class. The interpretation asks what that movement may reveal about positioning, liquidity preference, risk appetite, or crowding.

Useful fund-flow analysis usually checks five layers:

- Category: Which fund, sector, region, asset class, or theme received or lost money?

- Timeframe: Is the flow daily noise, weekly movement, or a multi-month pattern?

- Channel: Is the movement active, passive, ETF-driven, mutual-fund-driven, or rebalancing-related?

- Market backdrop: Are liquidity, credit, volatility, yields, and breadth confirming the flow interpretation?

- Positioning risk: Does the flow show early accumulation, broad confirmation, late crowding, or forced exit pressure?

The best use is not to ask whether fund flows are bullish or bearish in isolation. The better question is what they reveal about allocation pressure inside the broader market environment.

Frequently Asked Questions

Are fund inflows always bullish?

No. Inflows can support demand, but they can also reflect performance chasing, passive rebalancing, or crowded enthusiasm after a move has already happened.

Are fund outflows always bearish?

No. Outflows can show redemption pressure or risk reduction, but they can also reflect rotation, tax timing, rebalancing, or late-stage selling after prices have already adjusted.

What is the difference between fund flows and asset performance?

Fund flows measure money entering or leaving a fund or category. Asset performance measures price return. A fund can rise in value because holdings appreciate even if investor flows are weak, and it can receive inflows even if recent returns are already stretched.

Why does flow persistence matter?

Persistent flows across several periods can reveal a more durable allocation shift. One-period flow data can be noisy and may reflect rebalancing, reporting timing, or short-term reaction rather than a lasting change in positioning.