Capital flows describe how money moves across countries, funds, asset classes, and risk environments. The useful starting point is not one headline flow number, but the distinction between broad capital movement, investment-vehicle flows, defensive movement, short-term speculative movement, and stress-driven exits.

In market-structure analysis, capital-flow concepts help explain where pressure may be building across currencies, liquidity conditions, risk assets, and defensive assets. They are context inputs, not official flow data, policy conclusions, or automatic market signals. A flow reading becomes more useful when it is compared with time horizon, liquidity, policy context, positioning, credit conditions, and price behavior.

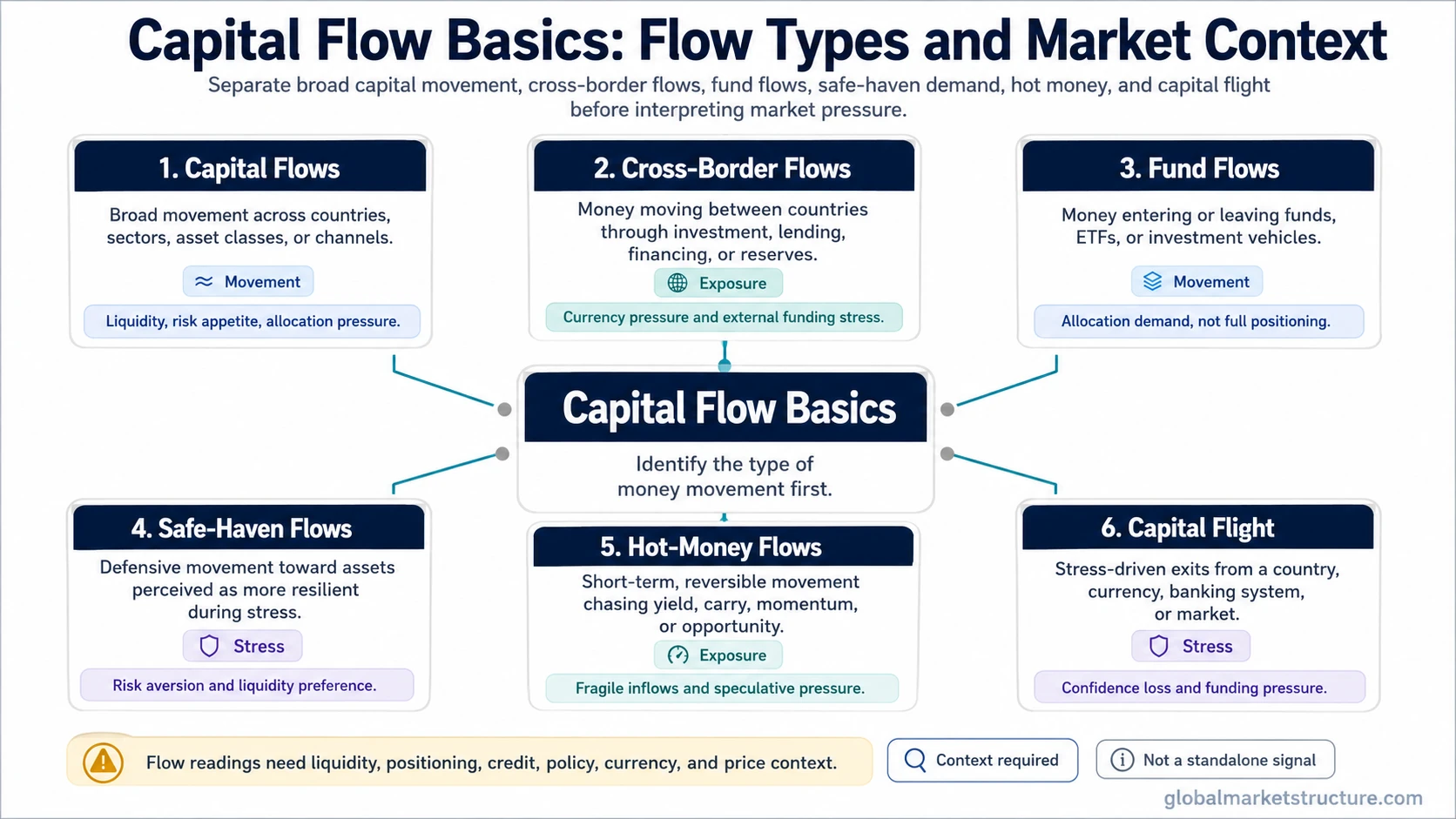

What Capital Flow Basics Covers

Capital-flow analysis starts with a simple question: what kind of money movement is being observed? A cross-border flow says something different from a fund-flow report. A safe-haven flow says something different from speculative hot money. Capital flight says something different from normal portfolio allocation.

The main distinction is between movement of capital across economic borders, movement into or out of investment vehicles, and movement caused by risk appetite or stress. Confusing those categories can make a flow signal look stronger, cleaner, or more directional than it really is.

Main Types of Capital Flows

Different capital-flow concepts answer different market questions. Separating the concept families first reduces the risk of treating one flow reading as a complete market signal.

| Flow concept | What it describes | What it helps interpret | What it does not prove | Deeper concept path |

|---|---|---|---|---|

| Capital flows | Broad movement of money between countries, sectors, asset classes, or financial channels. | Liquidity direction, risk appetite, currency pressure, and broad allocation changes. | It does not prove a precise market direction or timing outcome. | Start here when the question is broad movement of money. |

| Cross-border flows | Money moving between countries through investment, lending, trade-related financing, or reserve activity. | Currency pressure, external funding stress, balance-of-payments strain, and foreign capital dependence. | They do not automatically explain every move in a currency or equity market. | Use when the question involves country-level capital movement. |

| Fund flows | Money entering or leaving funds, ETFs, mutual funds, or other investment vehicles. | Investor allocation, demand for an asset class, and changes in fund-level exposure. | They do not necessarily show the full positioning of hedge funds, dealers, or leveraged participants. | Use when the source is fund or ETF inflow and outflow data. |

| Safe-haven flows | Defensive movement toward assets perceived as more resilient during stress. | Risk aversion, demand for liquidity, currency defense, and stress-sensitive allocation shifts. | They do not prove that all risk assets must keep falling. | Use when money appears to be moving defensively. |

| Hot money flows | Short-term capital movement that can shift quickly in search of yield, momentum, carry, or perceived opportunity. | Fragile inflows, speculative pressure, and sensitivity to rate or currency changes. | They do not show durable investment confidence by themselves. | Use when the flow looks fast, yield-sensitive, or reversible. |

| Capital flight | Stress-driven movement of money out of a country, currency, banking system, or market. | Loss of confidence, funding pressure, policy credibility risk, and defensive behavior under stress. | It does not always identify the exact trigger without supporting evidence. | Use when the question involves forced or fear-driven exits. |

Capital Flows vs Fund Flows and Positioning

Capital flows are the broadest category. They can describe movement across borders, asset classes, sectors, currencies, institutions, or funding channels.

Fund flows are narrower. They describe money entering or leaving investment vehicles, which can be useful for reading allocation demand but incomplete as a full picture of market exposure.

Positioning is different again. Positioning is about who is already exposed, how crowded that exposure may be, and how vulnerable it is to reversal. A market can receive inflows while positioning is already crowded, or show outflows while leveraged exposure remains high.

Useful distinction: flows describe movement; positioning describes exposure. A fresh inflow can add demand, but the market impact depends on who is buying, how crowded the trade already is, and whether liquidity can absorb the flow without large price movement.

When Capital Flows Matter for Market Structure

Capital flows matter most when they connect with a broader market condition. Cross-border outflows can become more important when a currency is already under pressure. Fund outflows can become more important when market liquidity is thin. Safe-haven flows can become more important when credit stress, volatility, and defensive leadership appear at the same time.

A common scenario is that money begins leaving riskier assets while defensive assets attract demand. The tempting reading is that risk appetite has fully broken. The stronger reading checks whether credit spreads are widening, liquidity is deteriorating, currency stress is rising, and market breadth is weakening. The weaker reading is a temporary allocation shift without wider confirmation.

What Capital Flows Cannot Show Alone

Capital-flow readings can show movement, pressure, or allocation change, but they cannot explain timing, causality, or market direction by themselves. The same inflow can mean fresh demand, crowded exposure, short-term yield chasing, or delayed reaction to an earlier price move.

The reading becomes stronger only when it is checked against liquidity, positioning, credit conditions, policy context, currency behavior, and price confirmation.