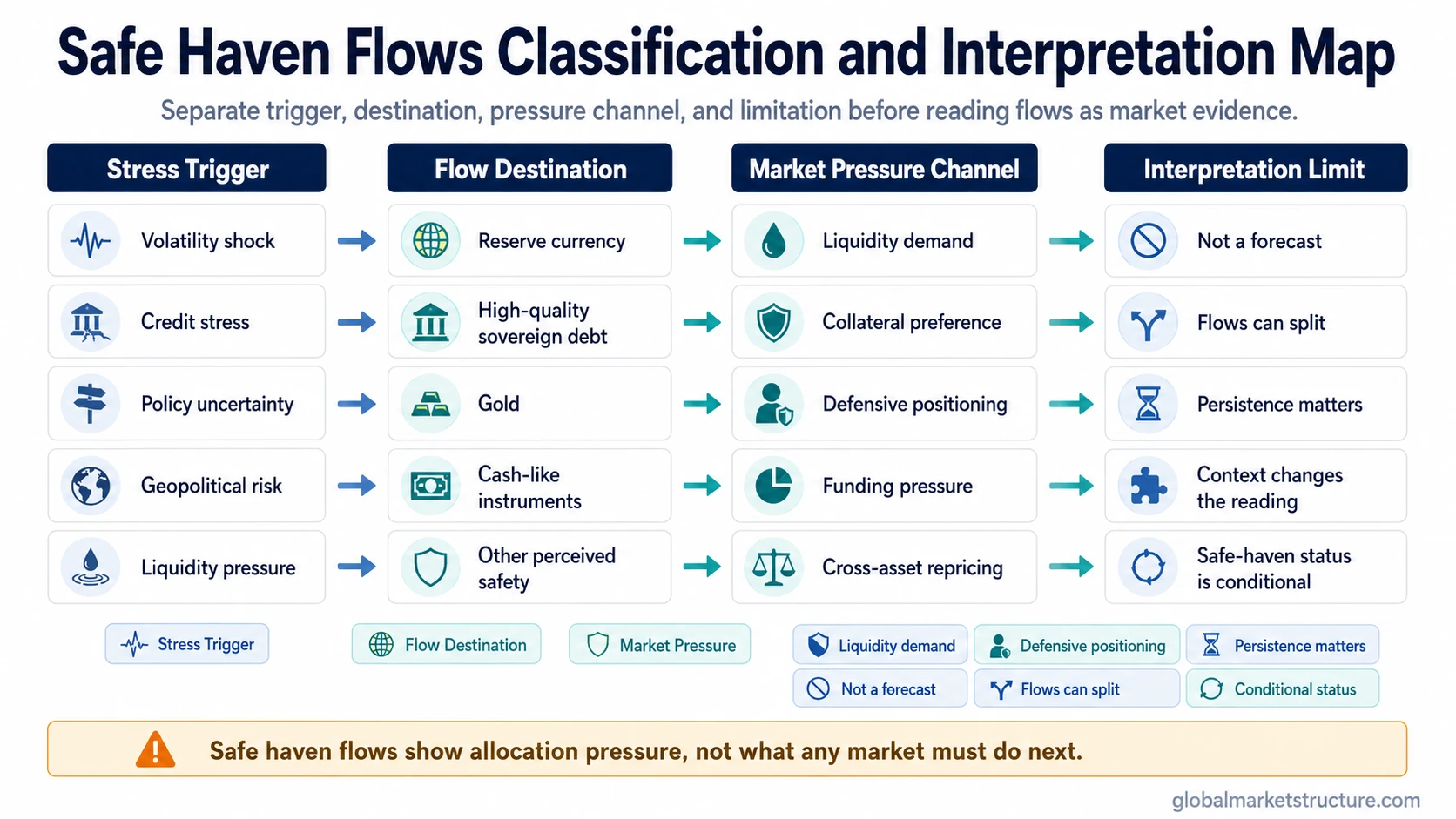

Safe haven flows are capital movements toward assets, currencies, or instruments that investors perceive as safer or more liquid during periods of stress. They show allocation pressure and positioning behavior, not a forecast of what any specific market must do next.

The useful distinction is between the destination and the movement. A safe-haven asset is a possible destination. A safe-haven flow is the movement of capital toward that destination when investors reduce risk, seek liquidity, or try to preserve optionality.

Simple definition: safe haven flows occur when capital shifts away from riskier exposures and toward perceived safety during uncertainty, volatility, policy stress, geopolitical risk, liquidity pressure, or broader risk-off conditions.

Safe-Haven Assets vs Safe-Haven Flows

Safe-haven assets and safe-haven flows are related, but they are not the same concept. The asset is the place capital may move toward. The flow is the movement itself, including its size, persistence, timing, and effect on market pressure.

| Concept | What it describes | Why the distinction matters |

|---|---|---|

| Safe-haven asset | An asset, currency, or instrument perceived as relatively defensive or liquid in stress. | The label describes a possible destination, not whether capital is actively moving there now. |

| Safe haven flow | The movement of capital toward perceived safety during stress. | The flow shows allocation pressure, positioning adjustment, and liquidity preference. |

| Risk-off behavior | A broader market regime in which investors reduce risk exposure. | Risk-off can include safe haven flows, but it can also include deleveraging, cash raising, and forced selling. |

| Capital flight | A more severe movement away from a country, currency, or financial system because confidence is weakening. | Capital flight can overlap with safe haven flows, but it usually implies stronger loss-of-confidence pressure. |

How Safe Haven Flows Create Market Pressure

Safe haven flows usually begin with a stress trigger. Investors may reduce exposure to risk assets, raise liquidity, hedge uncertainty, or shift toward markets that appear deeper, more liquid, or institutionally safer.

The pressure channel can appear across currencies, sovereign bonds, gold, cash-like instruments, and other perceived defensive destinations. The same stress episode can produce different flow patterns because liquidity, policy expectations, reserve behavior, funding pressure, and investor positioning may pull capital in different directions.

Mechanism: stress trigger → risk reduction → demand for perceived safety or liquidity → cross-asset pressure → interpretation depends on persistence, crowding, and regime context.

Common Destinations for Safe Haven Flows

Commonly discussed safe-haven destinations can include the U.S. dollar, high-quality sovereign debt, gold, the Swiss franc, the Japanese yen, and cash-like instruments, but the label is conditional rather than permanent. Safe-haven behavior can weaken, split, or reverse when policy expectations, real yields, liquidity needs, or institutional confidence change.

A safe-haven destination can also receive flows for different reasons. Currency demand may reflect liquidity preference. Sovereign-bond demand may reflect duration demand or collateral preference. Gold demand may reflect distrust of financial assets or currency debasement concerns. Cash demand may reflect a desire for optionality rather than confidence in any single asset.

| Flow destination | Possible pressure channel | Interpretation limit |

|---|---|---|

| Reserve currency | Liquidity demand, funding pressure, or global settlement preference. | Currency strength can reflect stress demand, not necessarily economic strength. |

| High-quality sovereign debt | Demand for liquid duration, collateral, or institutional safety. | Bond behavior can change when inflation, fiscal risk, or policy uncertainty dominates. |

| Gold | Demand for a non-credit, real-asset-style store of value. | Gold can be affected by real yields, dollar strength, liquidity needs, and positioning. |

| Cash-like instruments | Preference for optionality and reduced exposure. | Cash raising can signal caution, forced deleveraging, or temporary liquidity management. |

Why Persistence Matters

A short burst of safe haven flows can reflect a temporary shock response. Persistent flows can suggest a deeper allocation shift, stronger risk aversion, or a broader reassessment of liquidity and safety. The difference matters because one-day stress behavior can fade quickly, while sustained flow pressure can reshape currency, bond, credit, and equity conditions for longer.

Persistence should be read with surrounding evidence. If safe-haven demand appears alongside wider credit spreads, weaker market breadth, tighter liquidity, and defensive leadership, the signal is more structural. If the move fades while risk appetite returns, it may have been a short-lived positioning adjustment.

False Readings and Limitations

Safe haven flows are not a standalone market forecast. They can show where capital is moving under stress, but they do not prove that a crash, recession, currency rally, bond rally, or risk-asset decline must follow.

The most common mistake is treating one destination as if it represents the whole stress environment. Flows can split. Investors may seek dollars for liquidity while avoiding long-duration bonds because inflation or fiscal risk is also rising. Gold may rise in one stress regime and lag in another. A currency can strengthen because of funding pressure, even when the underlying economy is not stronger.

Safe-haven interpretation also depends on positioning. If a destination is already crowded, new stress may produce a weaker response than expected. If investors need cash quickly, they may sell assets that are usually considered defensive. For market-structure analysis, the stronger reading comes from the interaction between flows, liquidity, credit, rates, the dollar, and breadth.

Short Illustrative Scenario

A common scenario is that volatility rises while investors reduce equity exposure and increase demand for liquid currency or short-term government instruments. That does not automatically mean every safe-haven asset will rise. The cleaner interpretation is that capital is prioritizing liquidity and perceived safety until the stress either fades or becomes persistent enough to affect broader market structure.

Related Concepts

Fund flows are more specific vehicle or category-level measurements, such as money moving into or out of funds, ETFs, sectors, or asset classes. Safe haven flows are broader stress-driven allocation movements and may or may not be visible through fund-flow data alone.

Capital flight is a stronger and more specific confidence problem. It usually describes capital leaving a country, currency, or financial system because investors are trying to escape perceived political, currency, banking, or sovereign risk.

FAQ

What are safe haven flows?

Safe haven flows are capital movements toward assets, currencies, or instruments perceived as safer or more liquid during stress. They show allocation pressure, not a forecast.

Are safe haven flows the same as safe-haven assets?

No. A safe-haven asset is a possible destination. A safe haven flow is the movement of capital toward that destination during stress.

Do safe haven flows predict what markets will do next?

No. They can reveal risk aversion, liquidity preference, or positioning pressure, but they do not prove that a specific market move must happen next.

Why do safe havens sometimes move in different directions?

Safe havens can respond to different pressures. Liquidity demand, real yields, policy expectations, reserve behavior, inflation risk, and crowded positioning can make one destination strengthen while another weakens.