Sudden stop economics refers to a sharp interruption or reversal of external capital inflows. Its market-structure importance comes from the chain that can form when the flow shock affects FX, reserves, current-account adjustment, credit conditions, liquidity, and risk appetite. Not every outflow, currency decline, or reserve movement qualifies as a sudden stop.

Definition: A sudden stop is a capital-flow shock in which external financing slows abruptly, stops, or reverses after a period of reliance on foreign inflows. The label becomes more useful when the disruption is large, persistent, and visible across several market channels rather than one isolated move.

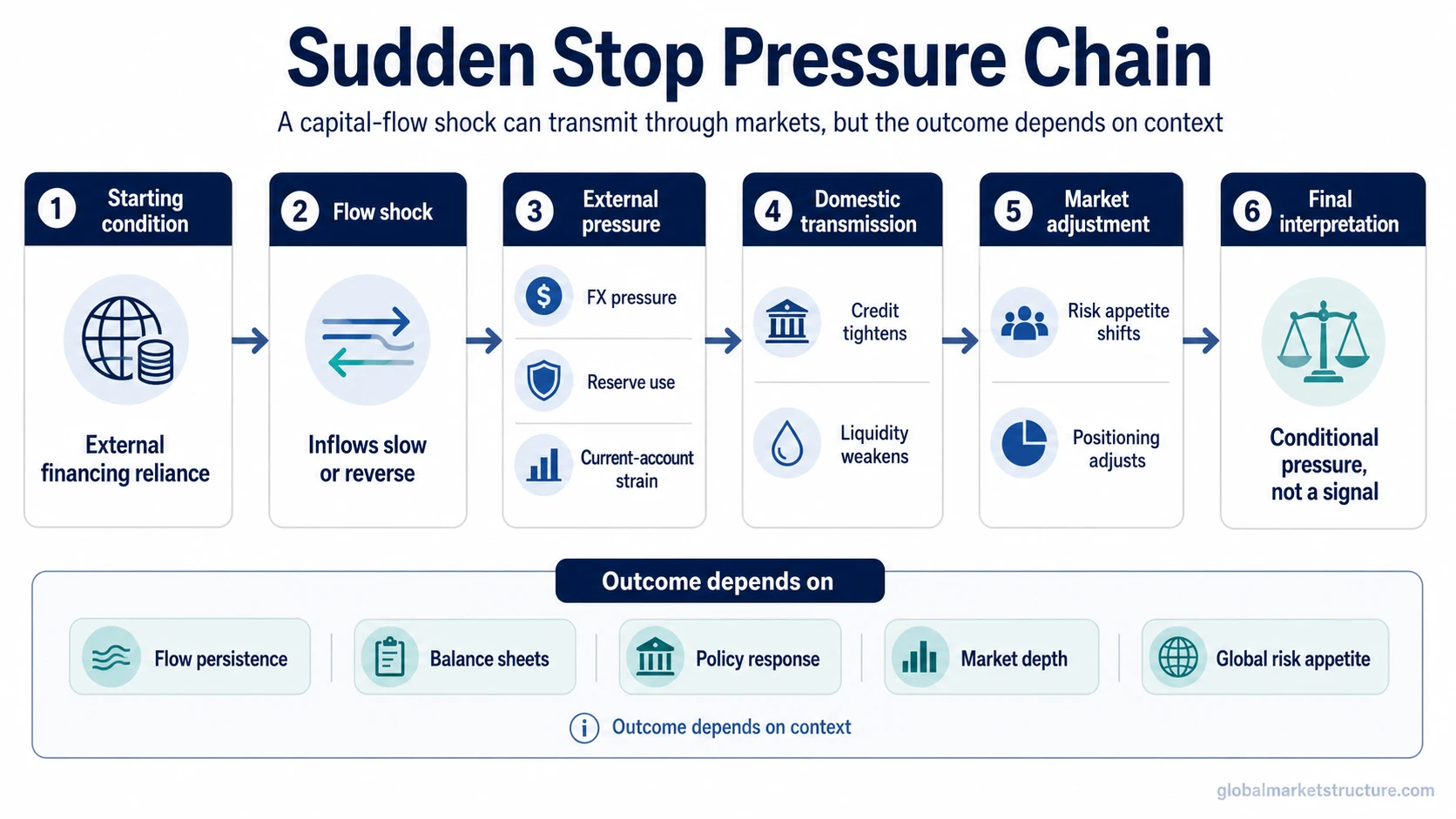

Condition: An economy or market segment depends on external financing, then capital inflows slow abruptly, stop, or reverse.

Pressure channel: FX demand can shift, reserves may be used, current-account adjustment can become more urgent, credit conditions can tighten, and liquidity can weaken.

Interpretation limit: The sudden-stop label is stronger when the evidence is broad and persistent. It is weaker when the evidence is limited to one temporary outflow or one isolated exchange-rate move.

The concept is often discussed in emerging-market contexts because external financing dependence, foreign-currency liabilities, reserve adequacy, and policy credibility can affect how quickly a funding shock spreads. The same label should still be handled carefully: sudden-stop dynamics describe a conditional pressure mechanism, not a forecast of a currency crisis or a direct market signal.

Key Points

- A sudden stop begins with an abrupt slowdown or reversal in external capital inflows.

- The shock can move through FX markets, reserves, current-account adjustment, credit conditions, liquidity, and risk appetite.

- The interpretation is stronger when the disruption is persistent and visible across several channels.

- A single outflow, currency decline, or reserve change does not prove a sudden stop.

- Policy response, balance-sheet resilience, market depth, and global risk appetite can soften or amplify transmission.

How Sudden Stop Dynamics Become Market Pressure

The chain usually starts before visible stress. External financing reliance builds during calmer conditions. When inflows slow or reverse, the adjustment can move from the balance of payments into market pricing and domestic financial conditions.

- External financing reliance: The economy or market depends on foreign capital to fund spending, investment, deficits, refinancing, or portfolio demand.

- Inflow stop or reversal: New financing becomes harder to attract, or previous inflows reverse as foreign investors reduce exposure.

- FX and reserve strain: Currency demand can shift, reserves may be used to smooth adjustment, and exchange-rate pressure can become more visible.

- Current-account or balance-of-payments adjustment: The economy may need to reduce external financing needs through weaker imports, lower domestic demand, or other adjustment channels.

- Credit and liquidity tightening: Banks, firms, and borrowers can face more difficult funding conditions, especially where foreign-currency liabilities or refinancing needs are material.

- Risk appetite and positioning adjustment: Investors may reduce exposure more quickly when crowded positioning, leverage, or weak policy credibility adds strain.

- Policy and balance-sheet response: Reserves, interest-rate policy, capital-flow tools, fiscal response, and balance-sheet resilience can change how far the shock travels.

The sequence is not automatic. Sudden-stop dynamics can remain contained if reserve buffers are strong, external debt is manageable, policy credibility is high, and global risk appetite stabilizes. They can become more severe when several channels deteriorate together.

Sudden Stop vs Related Capital-Flow Concepts

Cross-border flows are the broader category. They include capital moving into and out of economies through portfolio investment, direct investment, banking flows, lending, and other financial channels.

Capital flight emphasizes confidence-loss pressure and capital leaving a country or market, often involving domestic or resident exit as well as foreign-investor withdrawal. A sudden stop focuses more narrowly on the interruption or reversal of external inflows.

Hot money flows describe short-term mobile capital that can move quickly across markets. They can intensify sudden-stop pressure when short-term investors withdraw together, but short-term flow volatility is not identical to a full sudden-stop episode.

Useful boundary: A sudden stop is not simply “money leaving.” It is a financing shock where the loss or reversal of inflows becomes large enough to affect broader external adjustment and financial conditions.

Condition, Implication, and Limitation

| Condition | Possible implication | Interpretation limit |

|---|---|---|

| External financing was important before the shock | A loss of inflows can force faster adjustment | Low external financing reliance can reduce transmission |

| Capital inflows slow abruptly or reverse | FX demand, reserve use, and funding strain may become visible | One short-lived outflow is not enough by itself |

| Currency strain appears alongside reserve drawdown | Authorities may be smoothing adjustment or defending confidence | Reserve movements can have several causes and do not prove a sudden stop alone |

| Credit conditions tighten after the flow shock | The external shock may be moving into domestic liquidity and lending | Credit tightening can also come from domestic policy, banking stress, or cyclical weakness |

| Current-account adjustment becomes sharper | The economy may be reducing external financing needs | Current-account adjustment is an accounting and macro process, not a market signal by itself |

| Risk appetite deteriorates while positioning is crowded | De-risking can amplify the visible market move | Crowding can amplify strain, but it does not guarantee a reversal or crisis |

| Policy credibility is strong and buffers are available | The shock may be contained or slowed | Policy response changes transmission, but persistence still matters |

Evidence Quality Checklist for Sudden-Stop Risk

A sudden-stop interpretation is more defensible when several independent channels deteriorate together. One symptom can still be noise. A cluster of symptoms can indicate that the capital-flow shock is spreading through the broader market environment.

- Scale: The inflow slowdown or reversal is large relative to normal flow variation.

- Persistence: The disruption lasts beyond a brief portfolio adjustment or one-off event.

- FX strain: Currency strain appears alongside broader external-financing stress.

- Reserve strain: Reserve use or reserve concern appears together with other stress channels.

- Credit tightening: Banks, borrowers, or firms face more difficult financing conditions.

- External debt exposure: Foreign-currency liabilities or refinancing needs increase system sensitivity.

- Current-account adjustment: The economy may need sharper adjustment to reduce external financing needs.

- Policy credibility: Confidence in the policy response affects whether the disruption stabilizes or spreads.

- Domestic outflow behavior: Resident capital exit can add strain if confidence weakens at the same time.

- Global risk appetite: A global risk-off environment can make external financing harder to replace.

- Leverage and crowding: Crowded exposure or leverage can amplify de-risking when the shock becomes visible.

Interpretation rule: Macro and liquidity conditions define the environment. They do not create a mechanical signal. Sudden-stop analysis is strongest when flow persistence, FX strain, reserve stress, credit tightening, policy credibility, and risk appetite are read together.

Common Misreadings

Common mistake: Treating one market symptom as proof of a sudden stop can create a false reading.

- A capital outflow does not automatically equal a sudden stop.

- A currency decline does not automatically prove a sudden stop.

- A reserve movement does not automatically prove a sudden stop.

- A current-account adjustment is not a direct market signal.

- A stronger dollar or weaker global risk appetite can increase strain, but it does not guarantee a sudden stop.

The more useful approach is to ask whether the flow shock is large enough, persistent enough, and broad enough to alter financing conditions. If the evidence remains isolated, the label should stay tentative.

Sudden Stop Economics Example in Context

An economy has relied on foreign portfolio inflows and external borrowing during a calmer risk environment. External funding conditions tighten, new foreign inflows slow, and some investors reduce exposure. The currency comes under strain, reserves are used to smooth the adjustment, and local borrowers face higher refinancing costs.

The interpretation becomes more serious if the strain persists, credit conditions tighten, domestic capital also starts leaving, and policy response fails to restore confidence. The reading remains tentative if the outflow is brief, reserves remain adequate, credit markets stabilize, and inflows resume after the initial shock.

This scenario is illustrative, not a historical case. It shows how a capital-flow shock can move from external financing into FX, reserves, credit, liquidity, and positioning without implying that every similar episode has the same outcome.

Where Sudden Stops Fit in Capital-Flow Analysis

Sudden-stop dynamics are most useful when they are treated as one part of a broader capital-flow map. Cross-border financing, resident confidence, short-term mobile capital, reserve policy, and credit conditions can overlap during the same episode, but each concept explains a different part of the adjustment.

When the main question is whether domestic confidence is breaking down, capital flight is the cleaner concept. When the main question is how capital moves across borders in general, cross-border flows are the broader category. When the main issue is short-term mobile capital entering or leaving quickly, hot money flows give the narrower short-term lens.

FAQ

What is a sudden stop in economics?

A sudden stop in economics is a sharp interruption or reversal of external capital inflows. It matters because the financing shock can affect FX, reserves, current-account adjustment, credit conditions, liquidity, and risk appetite.

Is every capital outflow a sudden stop?

No. A capital outflow becomes more relevant to sudden-stop analysis when it is large, persistent, and connected to broader financing strain. A temporary outflow by itself is not enough.

Is a sudden stop the same as capital flight?

No. A sudden stop focuses on the interruption or reversal of external inflows. Capital flight focuses more on confidence-loss pressure and capital leaving a country or market, including domestic or resident exit.

Does a sudden stop guarantee a currency crisis?

No. Sudden-stop pressure can affect the currency, but the outcome depends on reserves, balance sheets, policy credibility, external debt exposure, market depth, and global risk appetite.