Capital flight is the movement of capital out of a country, market, or currency area when investors, companies, or households lose confidence in the local environment. In market-structure terms, it matters because stress-driven outflows can pressure currencies, reserves, funding conditions, domestic asset liquidity, and risk appetite. The interpretation is conditional: capital flight is not automatically a crash signal, a guaranteed devaluation, or proof that capital will never return.

What Is Capital Flight?

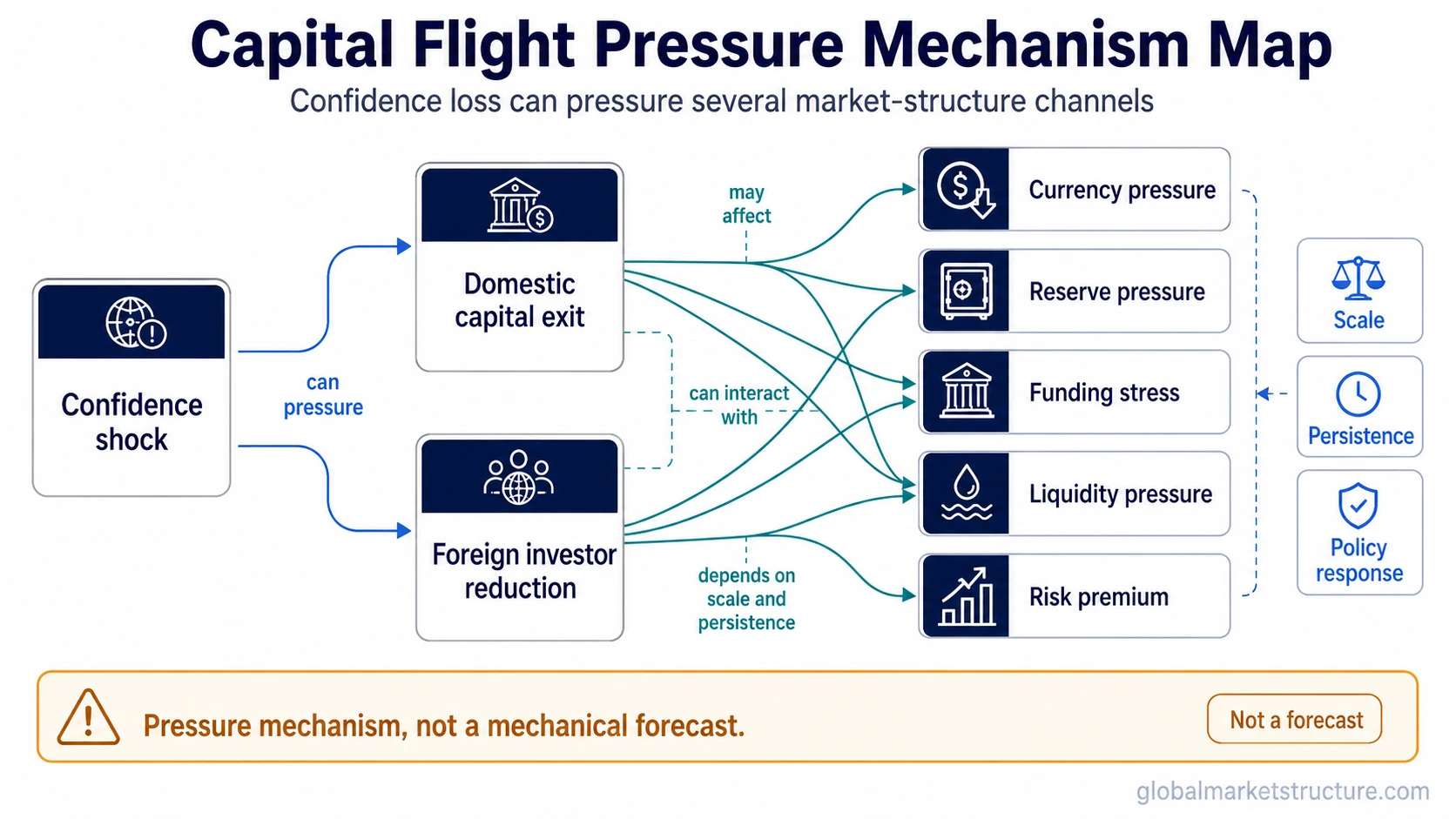

Capital flight describes capital leaving a domestic market because the perceived risk of staying has increased. The pressure may come from policy credibility concerns, currency instability, inflation risk, default risk, political uncertainty, capital-control fears, or a broader loss of confidence. Unlike ordinary international allocation, capital flight is usually stress-driven. The key feature is not simply that money crosses a border, but that it leaves because the source environment is becoming less trusted.

Key Points

- Capital flight is a stress-driven form of capital outflow, not every cross-border investment flow.

- It can appear through currency pressure, reserve pressure, domestic funding stress, weaker asset liquidity, or a rising local risk premium.

- The signal becomes more meaningful when outflows persist and interact with positioning, liquidity, and confidence.

- It should not be read as a mechanical market forecast or direct trading signal.

Where Capital Flight Fits in Capital Flows

Capital flight belongs inside the broader capital-flows category, but it is narrower than the full movement of money across borders. Normal portfolio allocation, foreign direct investment, hedging activity, and trade-related financial movement can all create cross-border flows without implying stress.

The distinction is the reason for the movement. A pension fund increasing foreign bond exposure, a company investing abroad, or a global manager rebalancing toward another region may be part of ordinary allocation. Capital flight points to a more defensive decision: capital is trying to reduce exposure to a place where confidence, convertibility, purchasing power, or institutional stability is being questioned.

What Can Trigger Capital Flight?

Capital flight can be triggered when investors begin to doubt whether local assets, deposits, or currency exposure are safe enough to hold. The trigger does not have to be one single event. It can develop as a sequence of credibility problems that changes how market participants view the risk of remaining exposed.

Common trigger categories include policy uncertainty, inflation pressure, fiscal stress, default concerns, currency depreciation risk, fear of capital controls, confiscation concerns, and loss of confidence in domestic institutions. These forces can overlap. For example, currency weakness can raise inflation risk, inflation risk can undermine policy credibility, and weak credibility can accelerate demand for foreign assets or harder currency exposure.

The mechanism should still be treated carefully. A country, currency, or market can face outflow pressure without entering a full capital-flight episode. The label becomes more appropriate when the movement is defensive, persistent, and tied to confidence loss rather than normal allocation choice.

How Capital Flight Shows Up in Market Structure

Capital flight is usually observed indirectly. It may appear through pressure on the exchange rate, falling foreign-exchange reserves, wider local funding stress, weaker domestic asset liquidity, higher yields, or a rising risk premium demanded by investors. None of these signals proves capital flight on its own, but together they can show that capital is becoming less willing to remain exposed to the local system.

The market-structure effect depends on the balance between outflows, policy response, available reserves, foreign-currency liabilities, domestic liquidity, and investor positioning. If outflows are small and temporary, markets may absorb them. If outflows persist while local liquidity weakens, the pressure can become self-reinforcing because defensive behavior reduces confidence further.

In some cases, capital flight can overlap with sudden-stop dynamics, especially when external financing dries up at the same time that domestic capital is trying to exit. The two concepts are related, but not identical. Capital flight emphasizes the exit of capital from the stressed source environment; a sudden stop emphasizes the abrupt interruption of financing or inflows.

Capital Flight vs Safe-Haven Flows

Capital flight and safe-haven flows can happen during the same risk episode, but they describe different sides of the process. Capital flight focuses on why capital leaves a stressed source. Safe-haven flows focus on where capital may go when investors seek perceived safety.

For example, if confidence weakens in one market, capital may leave that market and move toward assets or currencies seen as more stable. The exit pressure is the capital-flight side. The destination preference is the safe-haven-flow side. Separating the two helps avoid a common mistake: treating every move into safer assets as capital flight from a specific source.

Capital Flight Compared With Nearby Concepts

Capital flight is easiest to interpret when it is separated from adjacent flow concepts. Several market movements can look similar on the surface because they involve money moving across borders, but their causes and implications are different.

| Concept | Core Meaning | Main Interpretation Risk |

|---|---|---|

| Capital flight | Stress-driven outflow caused by loss of confidence, currency risk, policy risk, or fear of domestic exposure. | Reading it as an automatic crash or devaluation signal. |

| Cross-border flows | Any movement of capital between countries, including normal investment, hedging, and allocation activity. | Assuming every international flow reflects stress. |

| Safe-haven flows | Movement into assets or currencies perceived as safer during uncertainty. | Confusing destination preference with the source of stress. |

| Sudden-stop dynamics | Abrupt interruption of external financing or inflows, often during stress. | Treating every outflow as a sudden stop. |

Practical Scenario

A practical example is a market where policy credibility begins to weaken while inflation pressure remains high. Local investors may increase foreign-currency hedges, foreign investors may reduce domestic exposure, and companies may try to hold more liquidity outside the country. The result can be pressure on the exchange rate, weaker domestic asset demand, and tighter local funding conditions.

That sequence still does not prove a permanent crisis. If policy credibility improves, reserves remain adequate, liquidity stabilizes, or positioning becomes less one-sided, the pressure can fade. That makes capital flight a pressure mechanism rather than a single-point prediction.

Common False Readings

Capital flight is not automatically a market crash signal. Outflows can weaken risk appetite, but the outcome depends on scale, persistence, liquidity, policy response, and external financing conditions.

Capital flight does not guarantee currency devaluation. Currency pressure may appear, but reserves, policy credibility, interest-rate response, capital controls, and external balances can change the path.

Capital flight is not always illicit finance. Illicit flows can be part of some discussions, but the market-structure meaning is broader. Legal investors, companies, and households may all shift exposure when confidence deteriorates.

Capital flight does not mean all capital permanently leaves. Flows can reverse if confidence, policy credibility, valuation, or liquidity conditions change.

Why Persistence Matters

A one-off outflow is less informative than persistent pressure. Markets often absorb temporary rebalancing, hedging, or portfolio adjustment. The interpretation becomes stronger when outflows continue across several channels and begin to affect liquidity, funding, currency stability, or domestic asset pricing.

The difference is duration and motive: temporary allocation may reflect rebalancing, while capital-flight pressure becomes more serious when the outflow is tied to confidence loss and continues across several channels.

Persistence also matters because positioning can amplify the move. If many participants are already defensively positioned, an additional shock may create less pressure than expected. If investors are still heavily exposed to the stressed market, a confidence break can force a larger adjustment. This is why capital flight should be read with positioning, liquidity, policy response, and confidence together rather than as a standalone label.

Related Concepts

Capital flight sits next to several flow concepts that can look similar in market data. Cross-border flows describe the broader movement of money between countries. Safe-haven flows describe destination preference during stress. Sudden-stop dynamics describe an abrupt interruption of financing or inflows. Capital flight is narrower: it focuses on confidence-driven exit pressure from the stressed source environment.

FAQ

What does capital flight mean?

Capital flight means capital leaves a country, market, or currency area because confidence in the local environment has weakened. It is usually associated with stress, policy risk, currency risk, inflation risk, default concerns, or fear that domestic exposure has become less safe.

Is capital flight the same as normal foreign investment?

No. Normal foreign investment can reflect allocation, diversification, business expansion, or portfolio rebalancing. Capital flight is more defensive. It describes capital leaving because the source environment is perceived as riskier or less trustworthy.

Does capital flight always cause currency depreciation?

No. Capital flight can pressure a currency, but depreciation is not automatic. The outcome depends on policy response, reserves, external balances, liquidity, interest rates, positioning, and whether confidence stabilizes.

Why does capital flight matter for market structure?

Capital flight matters because persistent outflows can affect currency pressure, domestic liquidity, funding conditions, asset demand, reserve use, and risk appetite. It helps explain pressure inside a market, but it should not be treated as a mechanical forecast.