International capital flows are cross-border movements of financial capital between residents, institutions, governments, and markets in different countries. They include investment, lending, portfolio allocation, banking flows, reserve activity, and official financial movements that can affect currencies, yields, liquidity, risk appetite, and stress transmission.

Capital does not move through one channel or carry one meaning. A long-term investment into productive assets, a short-term bond outflow, and a central bank reserve adjustment can all cross borders, but each one can create different pressure in markets. The key distinction is which type of capital is moving, how persistent it is, and which market channel it is pressuring.

International Capital Flows vs Broader Capital Flows

Broad capital flows can describe many movements of money across investors, funds, sectors, or asset classes. International capital flows specifically involve financial capital moving across national borders.

That border distinction changes the interpretation. Cross-border flows can affect exchange-rate demand, domestic funding conditions, bond yields, reserve behavior, and external vulnerability. A domestic rotation from one sector to another may show allocation preference. A cross-border flow can also change the balance between local and foreign demand for a currency, asset market, or funding system.

What International Capital Flows Are and Are Not

| What they are | What they are not |

|---|---|

| Cross-border investment, lending, portfolio, banking, reserve, and official-flow movement. | A direct forecast for currencies, bonds, equities, or growth. |

| A balance-of-payments and market-pressure concept. | Automatically the same thing as capital flight. |

| A way to understand how external capital can affect currencies, yields, liquidity, and risk appetite. | Always a risk-on or risk-off signal. |

| A classification problem where flow type and persistence matter. | One uniform signal that can be read the same way in every market regime. |

| A macro-finance lens for interpreting external funding and asset-demand pressure. | A trading system or standalone timing tool. |

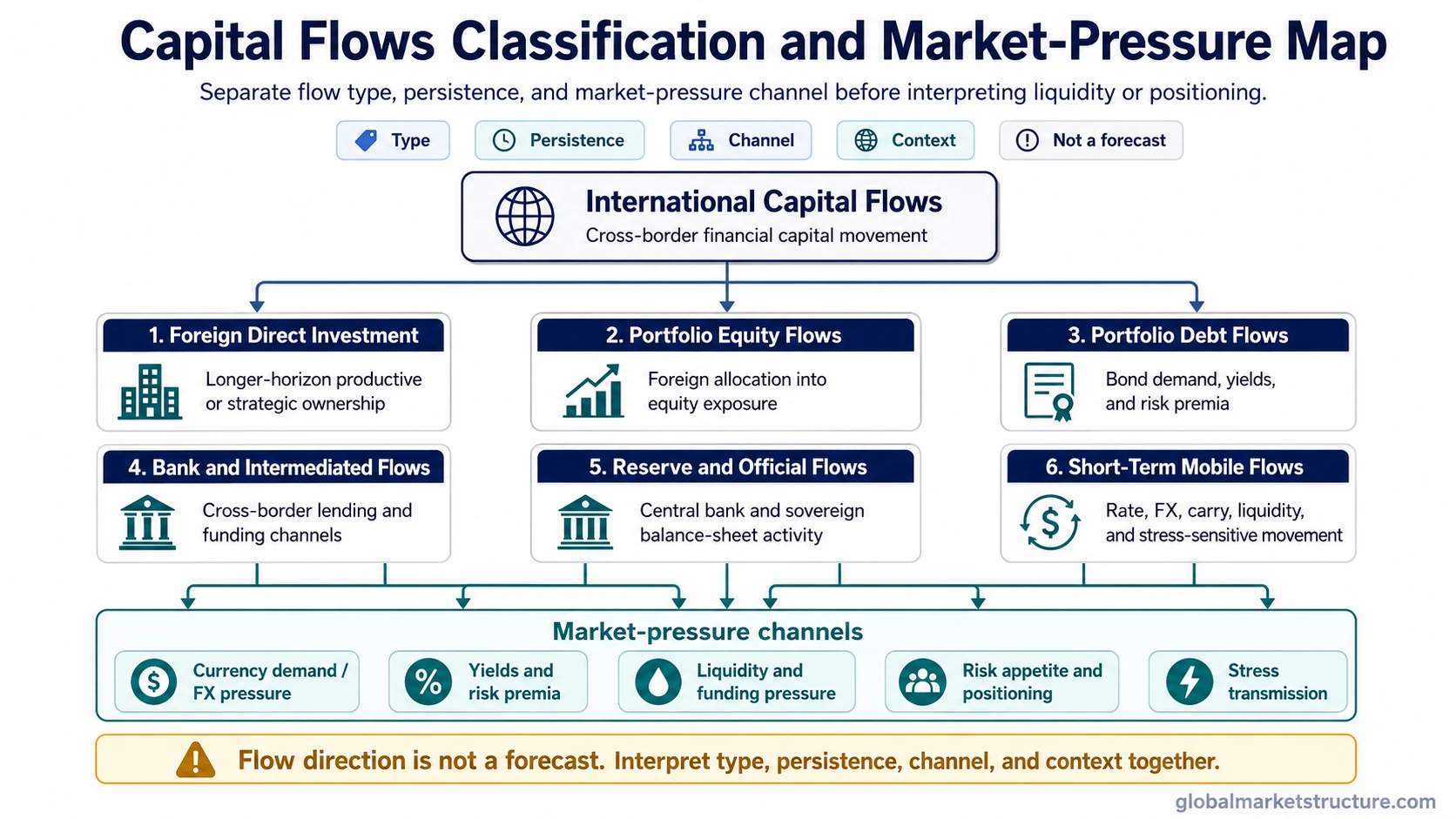

Main Types of Cross-Border Capital Flows

International capital flows become easier to interpret when the flow category is separated before the market conclusion is made. The same headline direction can hide very different behavior underneath.

| Flow type | Typical persistence | Main pressure channel | Interpretation limit |

|---|---|---|---|

| Foreign direct investment | Usually longer horizon | Productive investment, strategic ownership, local capacity, and long-term external commitment. | It may say more about structural investment than near-term market risk appetite. |

| Portfolio equity flows | Can shift with valuation, liquidity, and global risk appetite | Equity demand, index exposure, sector allocation, and foreign participation in local stock markets. | Equity inflows can reverse if liquidity, earnings expectations, or currency conditions change. |

| Portfolio debt flows | Often sensitive to rates, inflation expectations, credit risk, and currency hedging costs | Bond yields, term premia, sovereign funding, and foreign demand for fixed-income assets. | A bond inflow may reflect yield attraction, safety demand, policy credibility, or currency positioning. |

| Bank and intermediated flows | Can become more sensitive during funding stress | Cross-border lending, wholesale funding, credit availability, and banking-system liquidity. | These flows may become more important during stress than during calm periods. |

| Reserve and official flows | Policy-driven and institutionally managed | Central bank reserves, sovereign balance sheets, currency management, and official asset allocation. | Official flows may reflect policy objectives rather than private risk appetite. |

| Short-term mobile flows | Often less persistent | Rate differentials, FX expectations, carry conditions, liquidity preference, and stress response. | Short-term flows should not be interpreted like long-term productive investment. Related short-horizon pressure is better separated through hot money flows. |

How International Capital Flows Create Market Pressure

Cross-border flows can influence markets through several channels at the same time. The channel matters because a flow can support one part of the market while creating pressure somewhere else.

| Pressure channel | How the flow can show up | Interpretation boundary |

|---|---|---|

| Currency demand and FX pressure | Foreign investors may need local currency to buy domestic assets, while outflows may increase demand for foreign currency. | Currency pressure depends on hedging, central bank activity, current-account conditions, and market depth. |

| Yields and risk premia | Foreign demand for bonds can affect yields, while outflows can raise the compensation investors require to hold local debt. | Yield moves also reflect inflation, policy expectations, fiscal risk, and global duration demand. |

| Liquidity and funding pressure | Cross-border banks and intermediaries can expand or restrict credit availability across markets. | Funding pressure is strongest when flow changes interact with leverage, collateral needs, and balance-sheet constraints. |

| Risk appetite and positioning | Portfolio flows can show whether foreign investors are increasing or reducing exposure to local risk assets. | Positioning needs confirmation from liquidity, currency conditions, policy context, and later market behavior. |

| Crisis and stress transmission | Sudden outflows can transmit stress through FX, funding markets, reserves, bond yields, and credit conditions. | Stress interpretation requires context. Outflows are more serious when they are fast, broad, funding-sensitive, and hard to absorb. |

Common Misreads of International Capital Flows

A capital inflow is not automatically bullish. An inflow may support asset demand, but it can also reflect yield stress, defensive positioning, reserve management, or temporary carry interest.

A capital outflow is not automatically capital flight. Some outflows are normal portfolio rebalancing, debt repayment, foreign acquisition activity, or reserve adjustment. The term capital flight should be reserved for more urgent loss-of-confidence or safety-seeking behavior.

A flow direction is not a forecast. Flows describe movement and pressure. They do not prove what a currency, bond market, equity market, or economy will do next.

A short-term flow should not be interpreted like long-term FDI. Short-term capital can respond quickly to rates, FX volatility, funding stress, and risk appetite. Long-term direct investment usually carries a different time horizon and motive.

Net flows can hide offsetting gross-flow pressure. A calm net number can mask large inflows and outflows happening at the same time. That matters because gross flows can still affect FX liquidity, funding channels, and market depth.

Practical Scenario: Mixed Flow Signals

A country can receive long-term foreign direct investment while short-term portfolio capital is leaving local bonds. The first flow may reflect productive investment or strategic ownership. The second may reflect rate pressure, currency risk, weaker confidence, or changing risk premia.

Reading both together as a simple “capital is entering” signal would blur the market channels. The better interpretation separates flow type, time horizon, and pressure point: long-term investment may support structural activity, while bond outflows may still pressure yields, currency demand, and domestic funding conditions.

Related Capital-Flow Concepts

Several nearby concepts should be kept separate from international capital flows. Current account and capital account comparisons help separate trade, income, and transfer balances from capital-account classification. Capital account and financial account comparisons help clarify why many market-relevant cross-border asset and liability movements sit in the financial-account side of balance-of-payments analysis.

Capital flight and hot money flows are narrower concepts. They can be important when cross-border movement becomes fast, confidence-sensitive, or funding-sensitive, but they should not replace the broader classification of international capital flows.