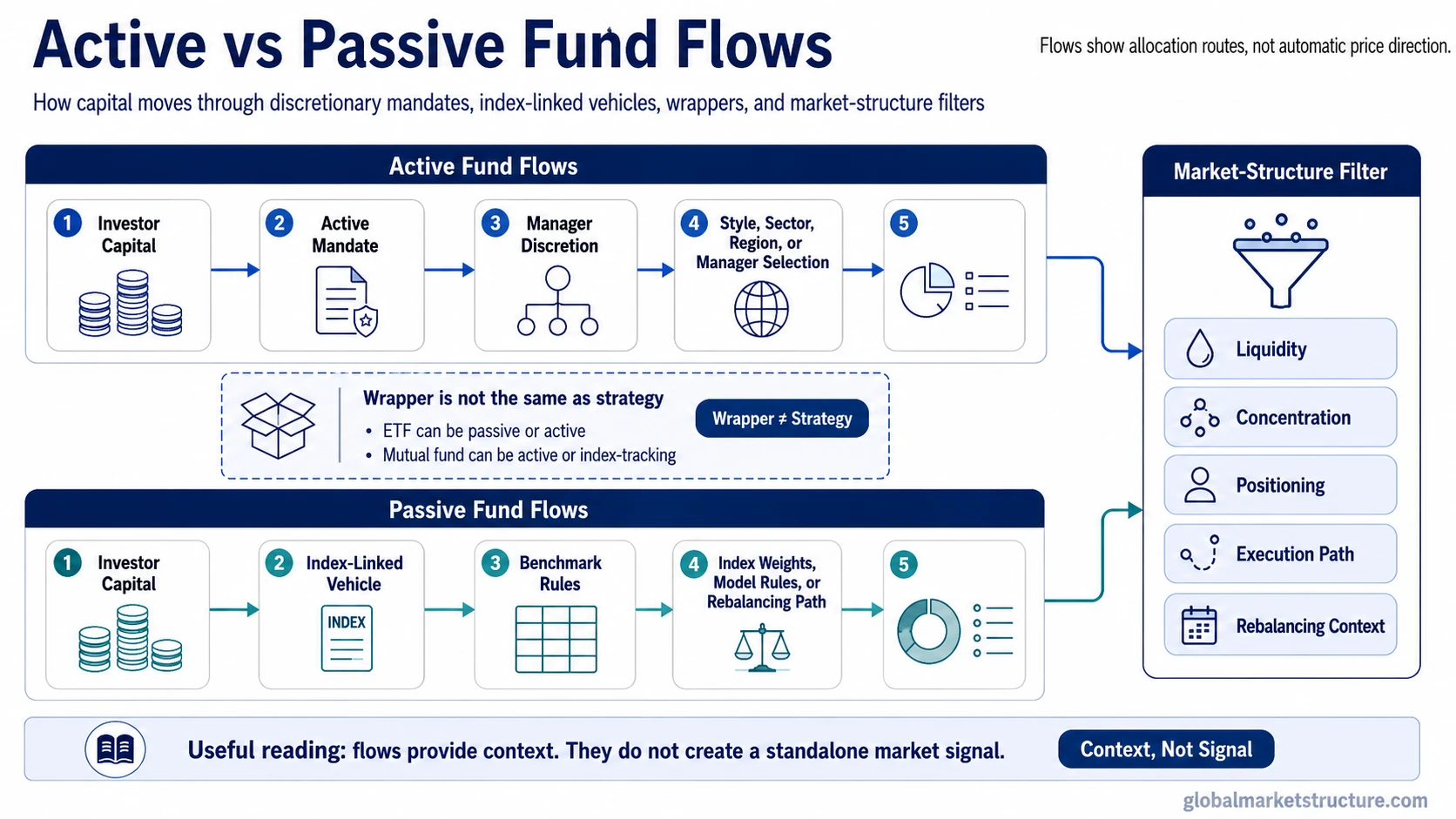

Active fund flows and passive fund flows both describe capital moving into or out of investment funds, but they measure different allocation routes. Active fund flows reflect capital moving through funds where managers or allocators make discretionary positioning choices. Passive fund flows reflect capital moving through index-tracking, benchmark-linked, or rules-based vehicles where exposure is shaped by a benchmark, allocation rule, or model rather than by security-by-security judgment. The label still needs context: a passive-labeled vehicle can be used for an active allocation choice, while some active-labeled funds can remain close to benchmark exposure.

Key Points

- Active fund flows show capital moving into or out of discretionary active mandates.

- Passive fund flows show capital moving into or out of index-tracking, benchmark-linked, or rules-based vehicles.

- ETF flows are not automatically passive flows because an ETF is a product wrapper, not a strategy type.

- Mutual fund flows are not automatically active flows because mutual funds can also track indexes.

- Flow direction is not the same as price direction. Market impact depends on liquidity, concentration, positioning, and execution path.

Active vs Passive Fund Flows at a Glance

| Question | Active Fund Flows | Passive Fund Flows |

|---|---|---|

| What is being tracked? | Capital moving into or out of discretionary active fund mandates. | Capital moving into or out of index-tracking, benchmark-linked, or rules-based vehicles. |

| Who shapes the exposure? | A manager, allocator, strategy team, or investor selecting an active mandate. | An index, benchmark, allocation rule, model portfolio, or rules-based exposure design. |

| What can the flow reveal? | Demand for active management, category rotation, manager selection, or discretionary risk allocation. | Demand for benchmark exposure, index participation, model allocation, or rules-based market exposure. |

| What can the flow hide? | The reason for the movement, such as fees, taxes, manager replacement, or category rotation. | Whether the investor is making a broad passive allocation or using a passive wrapper for an active exposure choice. |

| Common misread | Active outflows automatically mean bearish market conviction. | Passive inflows automatically mean mechanical market support. |

| Market-structure relevance | Can matter when redemptions, category shifts, or discretionary de-risking affect liquidity and positioning. | Can matter when flows interact with index weights, concentration, liquidity, rebalancing, or persistent benchmark-linked demand. |

What Active Fund Flows Show

Fund flows describe capital entering or leaving fund vehicles. Active fund flows are the part of that picture tied to active mandates, where exposure is shaped by manager discretion, allocator preference, or investor selection of an active strategy.

An active inflow may show demand for a manager, style, asset class, sector mandate, region, or strategy category. An active outflow may show redemptions, fee pressure, tax timing, weak confidence in a manager, or a shift toward cheaper benchmark exposure. The number alone does not explain the motive.

Clean Reading

Active fund flows are best read as discretionary allocation movement. They can show where investors are adding or removing capital from active mandates, but they do not automatically prove a market view or future price direction.

For market-structure analysis, active-flow data becomes more useful when it is checked against liquidity, positioning, credit conditions, volatility, and broader cross-asset behavior. A large active outflow may reflect true de-risking, but it may also reflect vehicle migration if the same capital remains invested through passive products.

What Passive Fund Flows Show

Passive flows describe capital moving through index-tracking, benchmark-linked, or rules-based exposure channels. Once money enters a passive vehicle, exposure is usually distributed according to the vehicle’s rules rather than a manager’s security-level judgment.

Passive inflows can create demand for benchmark exposure. Passive outflows can remove exposure according to the same benchmark-linked logic. The effect can become more important when the benchmark is concentrated, when underlying securities are less liquid, or when the flow overlaps with other positioning pressure.

Important Limitation

Passive fund flows are not automatic market support. A market can absorb large passive inflows quietly when liquidity is deep and offsetting supply is available. A smaller flow can matter more when liquidity is thin, benchmark concentration is high, or many participants are positioned in the same direction.

Why Flow Charts Are Easy to Misread

Flow charts often compress several different ideas into one label. A chart may classify flows by fund wrapper, management style, product category, asset class, investor channel, or reporting provider methodology. Those categories can overlap, but they are not identical.

The most common error is treating ETF flows as passive flows. ETF flows describe money moving into or out of ETF products. An ETF is a wrapper. It can hold passive index exposure, active exposure, sector exposure, thematic exposure, leveraged exposure, inverse exposure, or factor-based exposure.

The reverse mistake also matters. A mutual fund is not automatically active. An index mutual fund can behave like a passive exposure vehicle even though it is not an ETF. A flow chart that separates ETF flows from mutual fund flows may therefore be showing product-wrapper migration rather than a clean active versus passive strategy split.

Wrapper Versus Strategy Type

| Label | What It Actually Describes | What It Does Not Automatically Prove |

|---|---|---|

| ETF flow | Money entering or leaving ETF products. | That the strategy is passive. |

| Mutual fund flow | Money entering or leaving mutual fund products. | That the strategy is active. |

| Passive flow | Money routed through index-tracking, benchmark-linked, or rules-based exposure. | That the investor has no active allocation intent upstream. |

| Active flow | Money routed through discretionary active mandates. | That the fund is meaningfully different from the benchmark in every case. |

Same Scenario, Different Reading

Example Scenario

Suppose money leaves active equity mutual funds while broad index ETFs receive inflows during the same period. The surface-level reading may look like active outflows and passive inflows. That does not automatically prove a bullish or bearish market view.

Several interpretations may coexist. Investors may be replacing higher-fee active vehicles with lower-fee benchmark exposure. Model portfolios may be routing new contributions into index products. Retirement-plan contributions may be adding steady passive demand. At the same time, some investors may be redeeming from underperforming active managers without reducing total equity exposure.

The useful distinction is that active outflows can show pressure on discretionary active mandates, while passive inflows can show benchmark-linked demand. The market impact depends on where the flows land, how concentrated the benchmark is, and whether liquidity can absorb the adjustment.

Boundary Cases That Confuse the Label

| Boundary Case | Why It Confuses the Label | Cleaner Interpretation |

|---|---|---|

| Active ETF | The wrapper is an ETF, but the strategy may use active discretion. | Classify wrapper and strategy separately. |

| Index mutual fund | The wrapper is a mutual fund, but the strategy may be passive. | Do not assume mutual fund equals active management. |

| Smart beta or factor product | The vehicle may follow rules, but those rules express an active design choice. | Treat it as rules-based exposure and check the index methodology. |

| Model portfolio allocation | The end vehicle may be passive, but the upstream allocation decision may be active. | Separate investor allocation choice from exposure engine. |

| Closet-index active fund | The mandate is active, but the portfolio may stay close to the benchmark. | Check actual holdings and benchmark deviation, not only the label. |

How to Read Market Impact Without Overstating It

Fund flows become market-structure relevant only after they pass through several filters. The first filter is the exposure engine. If a flow enters a broad index-tracking product, the buying or selling pressure is distributed according to the benchmark. If it enters an active mandate, the manager may hold cash, rotate sectors, change security weights, or delay deployment.

The second filter is liquidity. A large flow into highly liquid securities may have limited visible price impact. A smaller flow into less liquid securities can matter more if the order flow arrives when depth is thin or when other investors are already crowded in the same direction.

The third filter is concentration. Passive flows into a concentrated benchmark can direct more capital toward the largest index weights. Active flows into a narrow style, sector, or region can concentrate pressure in a different way. The label alone does not show where the actual pressure appears.

The fourth filter is execution path. Some fund flows are absorbed through primary-market creation and redemption mechanisms, internal cash buffers, derivatives, futures, or portfolio rebalancing. Others reach underlying securities more directly. This is why reported flow data should be connected to liquidity and positioning before drawing conclusions.

Active and Passive Flows in a Broader Capital-Flow Map

Active versus passive fund flows are one layer of the broader capital-flow system. They sit alongside retirement contributions, ETF creations and redemptions, institutional rebalancing, model portfolio allocation, buybacks, dealer hedging, volatility targeting, and other routes that can affect market demand or supply.

The active versus passive distinction is useful because it separates discretionary allocation movement from benchmark-linked exposure movement. It becomes more useful when paired with index rebalancing, because passive vehicles may need to adjust exposure when benchmark weights, index membership, or portfolio rules change.

Market-Structure Reading

The question is not whether active or passive flows are better. The stronger question is how capital is routed, whether the route is discretionary or rules-based, whether the wrapper label hides the exposure engine, and whether liquidity conditions make the flow more or less important.

When Active Flow Data Is More Useful

Active flow data becomes more useful when the question is about discretionary allocation behavior. Large active outflows from a category may show reduced appetite for a manager, style, sector, region, or strategy type. Large active inflows may show renewed demand for a mandate or a shift toward a particular allocation theme.

The data is less useful when it is read as a direct market call. Active outflows can reflect fee pressure, fund closure, tax timing, platform changes, institutional mandate shifts, or migration to passive exposure. The same reported flow can therefore represent de-risking, vehicle substitution, or administrative movement depending on context.

| Active Flow Reading | Possible Interpretation | What to Check Before Concluding |

|---|---|---|

| Active equity fund outflows | Reduced demand for active equity mandates. | Whether broad equity exposure is also falling or simply moving to passive vehicles. |

| Active sector fund inflows | Demand for a specific discretionary sector mandate. | Whether the same sector is also receiving passive index or ETF demand. |

| Active bond fund outflows | Possible risk reduction, duration concern, credit concern, or manager rotation. | Whether money is moving to cash, short duration, passive bond funds, or another active mandate. |

When Passive Flow Data Is More Useful

Passive flow data becomes more useful when the question is about benchmark-linked demand. Inflows into index-tracking products can show demand for exposure to a benchmark. Outflows can show reduced exposure to that benchmark. The effect depends on the benchmark’s construction and the liquidity of the underlying securities.

Passive flow data is especially relevant when it overlaps with concentration, index membership changes, portfolio rebalancing, or mechanical allocation rules. In those cases, the flow may not reflect a security-level view, but it can still affect how demand is distributed across the market.

Passive Flow Interpretation Filters

- Benchmark: Which index or rule set determines the exposure?

- Concentration: Are flows directed toward a small group of large weights?

- Liquidity: Can underlying securities absorb the adjustment?

- Rebalancing: Are index or model changes forcing mechanical buying or selling?

- Offsetting supply: Are other investors selling into the flow or buying alongside it?

What the Distinction Does Not Tell You

The active versus passive distinction does not reveal the full investor motive. It does not prove whether investors are bullish, bearish, defensive, fee-sensitive, tax-driven, performance-chasing, or simply following a model allocation. It also does not show whether flows have already been absorbed by the market.

The distinction also does not settle the active versus passive investing debate. A fund-flow page is not the same as a performance comparison. Flow data shows where capital is moving. Performance analysis asks whether one approach has delivered better returns, after fees, over a specific period and benchmark.

Interpretation Boundary

Fund-flow direction is context, not a standalone signal. It can help explain demand routes and positioning pressure, but it should not be used by itself to forecast prices, recommend funds, or infer complete investor intent.

How to Use the Distinction Safely

A safer reading starts by asking four questions. First, is the flow classified by strategy type, product wrapper, asset class, or reporting category? Second, does the flow change total market exposure or mostly shift exposure from one wrapper to another? Third, does the flow route through a discretionary manager, a benchmark, or a rules-based model? Fourth, do liquidity and concentration make the flow likely to matter for market structure?

Those questions prevent the two biggest errors: treating all ETF flows as passive and treating all passive flows as automatic market support. They also prevent the opposite error of dismissing passive flows entirely. Rules-based exposure can still matter when it is large, persistent, concentrated, or aligned with other market pressures.

Market-Structure Filters to Check

Liquidity is the first filter. If liquidity is deep, flows may be absorbed with limited visible effect. If liquidity is thin, the same type of flow can have a larger price impact because less opposing supply or demand is available at nearby prices.

Concentration is the second filter. Broad passive inflows into a highly concentrated index may have a different effect than passive inflows into a more diversified benchmark. Active redemptions from a concentrated style category may affect a narrower set of securities than broad market outflows.

Persistence is the third filter. A short-term flow reversal may be noise. Persistent multi-period movement can reveal more durable allocation preference, product migration, or benchmark-linked demand. Even then, the flow still needs to be interpreted alongside liquidity and positioning rather than treated as a standalone market signal.

Common Mistakes

Misreadings to Avoid

- ETF flows equal passive flows: ETFs are products. Passive investing is a strategy type. The two can overlap, but they are not identical.

- Mutual fund flows equal active flows: Mutual funds can be active or passive, so the wrapper alone is not enough.

- Passive inflows are automatically bullish: Passive inflows can add demand, but they do not guarantee higher prices.

- Active outflows are automatically bearish: Active outflows may reflect vehicle migration rather than full market de-risking.

- Flow charts prove investor psychology: Flow charts show reported capital movement, not the complete reason behind that movement.

Related Capital-Flow Concepts

How to Route the Concept

Active versus passive fund-flow analysis is strongest when it is connected to the broader capital-flow map. Fund-flow analysis explains where money is entering or leaving fund vehicles. Passive-flow analysis explains benchmark-linked exposure routes. ETF-flow analysis separates product-wrapper movement from strategy type. Index-rebalancing analysis explains when rule-based exposure changes can create mechanical adjustment.

The practical question is not whether active or passive is better. The useful question is what route the capital is taking, what the label hides, and whether liquidity, concentration, and positioning make that route important for market structure.

FAQ

Are active fund flows the same as active investing performance?

No. Active fund flows show capital moving into or out of active mandates. They do not prove that active managers are performing well or poorly, and they do not settle the active versus passive performance debate.

Are passive fund flows the same as ETF flows?

No. ETF is a product wrapper. Passive is a strategy type. Some ETFs are passive, but ETFs can also be active, thematic, leveraged, inverse, sector-focused, or factor-based.

Can active funds have outflows while passive funds have inflows?

Yes. That can happen when investors reduce exposure to discretionary active mandates while still adding money to broad benchmark-linked or rules-based vehicles.

Do passive inflows always push markets higher?

No. Passive inflows can add demand through benchmark-linked routes, but market impact depends on liquidity, concentration, positioning, valuation, and how much of the flow is absorbed by other participants.

Why does the active versus passive flow distinction matter?

It matters because the two flow types describe different allocation routes. Active flows emphasize discretionary allocation behavior, while passive flows emphasize benchmark-linked or rules-based exposure mechanics.