Passive flows are capital flows created when money moves through passive, index-linked, benchmark-linked, or rules-based investment vehicles and mandates. They matter for market structure because allocation rules can translate contributions, withdrawals, benchmark weights, and rebalancing needs into demand for baskets, sectors, or securities. They do not predict price direction by themselves because any market impact depends on liquidity, flow size, timing, prior positioning, and market absorption.

A passive flow is not the same as passive income, and it is not simply a statement that passive investing is good or bad. In market-structure analysis, the useful question is narrower: how does capital that follows an index, benchmark, basket, or rule pass into markets, and when can that flow become large enough to matter?

What Passive Flows Mean

Passive flows describe capital movement linked to a predefined allocation process rather than a discretionary security-by-security decision. The source can be investor contributions, redemptions, portfolio rebalancing, benchmark tracking, mandate rules, or exposure targets. The destination is usually a basket, index, sector, asset class, or group of securities that the passive vehicle or mandate is designed to hold.

The word “passive” can be misleading. The investor or mandate may not be making a fresh active view on each underlying security, but the resulting flow can still create demand or supply pressure when implementation reaches the market.

Key Points

- Passive flows are allocation-linked flows, not passive income.

- Their market effect is conditional, not automatic.

- ETF flows, index rebalancing, and active-vs-passive fund flows are related concepts, but they are not identical to passive flows.

Passive Flows Are a Flow Category, Not a Product Wrapper

Passive flows should be understood as a flow category. They can appear through index funds, ETFs, model portfolios, pension allocations, benchmark-aware mandates, systematic allocation rules, and other vehicles that follow a predetermined exposure map. The wrapper matters because it changes how the flow reaches the market, but the core idea is the same: capital is being routed according to a rule, benchmark, or allocation structure.

This distinction keeps the concept narrower than a broad passive investing guide. A long-term investor buying an index fund, an institution rebalancing to a policy benchmark, and a rules-based portfolio changing exposure can all create flow pressure. The mechanics differ, but each case involves capital being directed by a predefined structure rather than a fresh discretionary view on every underlying holding.

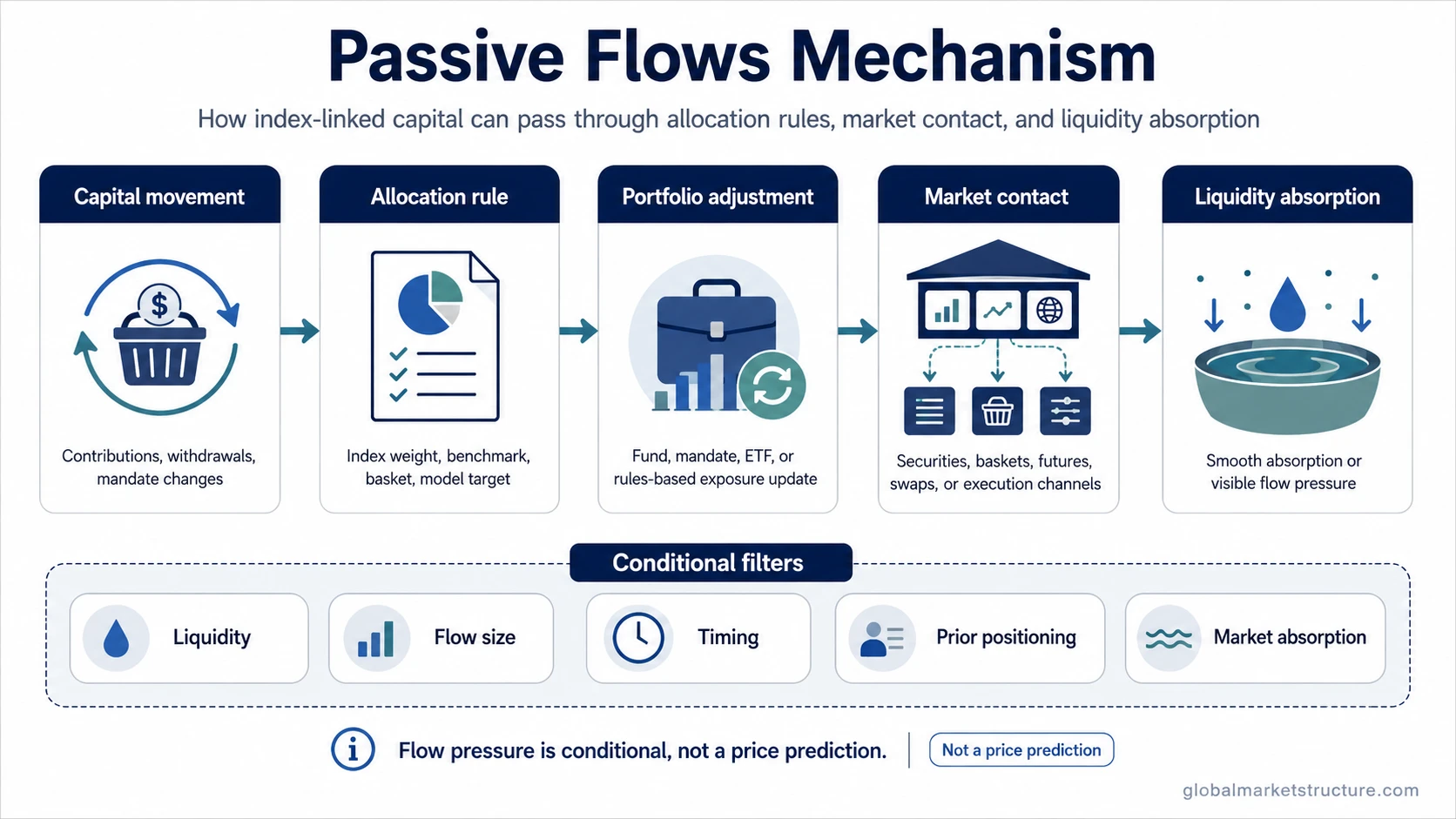

How Passive Flows Move Through Market Structure

The mechanism is easiest to read as a sequence. Passive flows usually start with capital entering or leaving a vehicle or mandate. The vehicle then maps that capital to a benchmark, basket, asset-class weight, or rule. Execution can translate the allocation into market orders, basket trades, derivatives exposure, or other implementation adjustments. The final market effect depends on whether liquidity can absorb that demand or supply without major price disturbance.

- Capital movement: money enters or leaves a passive vehicle, benchmark-linked account, or rules-based allocation program.

- Allocation rule: the vehicle or mandate translates that movement into required exposure by index weight, basket composition, model weight, or policy target.

- Portfolio adjustment: the manager, issuer, account, or execution process adjusts positions or exposures to match the required allocation.

- Market contact: demand or supply can reach underlying securities, futures, baskets, swaps, or other implementation channels.

- Liquidity absorption: the market either absorbs the flow smoothly or shows more visible price pressure, spread widening, execution cost, or crowding effects.

Some rules-based channels sit near passive flows without being identical to them. For example, volatility targeting adjusts exposure based on volatility inputs, so it belongs to the broader rules-based flow universe, but it is not the same thing as passive index allocation.

Where Passive Flows Become Observable

Passive flows can become visible where the allocation rule meets the market. Index funds may need to buy or sell baskets when investor money enters or leaves. ETFs may show wrapper-level creations, redemptions, or secondary-market pressure, although ETF flows are only one channel inside the broader passive-flow discussion. Benchmark-aware mandates can create demand when portfolio weights drift from target. Rebalancing windows can concentrate activity when many vehicles adjust around similar reference points.

The important point is not that every passive allocation creates visible market pressure. Many flows are absorbed quietly, especially when they are small relative to market depth. The flow becomes more relevant when it is large, synchronized, predictable, or concentrated in less liquid securities or crowded exposures.

When Passive Flows Can Matter More

Passive flows can matter more when flow size is large relative to available liquidity. A large inflow into a liquid index basket may be absorbed with little visible stress, while a smaller flow into a less liquid segment can create more noticeable pressure. Timing also matters. Flow that arrives near benchmark events, month-end or quarter-end rebalancing, or crowded positioning windows can interact with existing market pressure.

Prior positioning changes the interpretation. If many participants already hold the same exposure, additional passive demand may reinforce crowding. If the market is already thin, even rule-based flow can appear more forceful. If liquidity is deep and opposing supply is available, the same flow may have little visible impact.

Illustrative Scenario

A common scenario is a benchmark-linked allocation receiving steady inflows while liquidity in one part of the basket is weaker than usual. The first read may be that passive demand is automatically pushing prices higher. That read is incomplete. A stronger case would compare the size of the flow with available liquidity, check whether related baskets are moving together, and ask whether the pressure appears around an allocation or rebalancing window. A weaker case would be a price move with no clear flow channel, no timing cluster, and enough market depth to absorb the activity without visible stress.

What Passive Flows Do Not Prove

Passive flows do not prove future price direction. They can create demand or supply pressure, but that pressure still has to pass through liquidity, execution, positioning, hedging, and market absorption. A passive-flow explanation is strongest when the flow channel, timing, affected basket, and liquidity condition can be identified. It is weakest when the phrase is used as a broad explanation for any market move after the fact.

Passive flows also do not explain market concentration, volatility, or trend behavior by themselves. They may contribute to those conditions under some circumstances, but causal claims require stronger evidence. Current flow totals, passive ownership shares, market-on-close statistics, concentration measures, or historical case claims should be sourced and dated before they are used as factual support.

Passive Flows Versus Nearby Concepts

Passive flows sit near several related ideas. The concepts overlap in market discussion, but they answer different questions.

| Concept | Main meaning | How it differs from passive flows |

|---|---|---|

| Passive flows | Capital moving through passive, index-linked, benchmark-linked, or rules-based allocation channels. | This is the broad flow category being defined on this page. |

| ETF flows | Flows visible through ETF trading, creations, redemptions, or wrapper-level demand. | ETF flows are one possible channel, not the full passive-flow universe. |

| Index rebalancing | Benchmark changes or scheduled weight adjustments that can create buying or selling needs. | Index rebalancing is an event or methodology-driven mechanism, not the entire category of passive flows. |

| Active vs passive fund flows | Comparison of capital moving between discretionary active funds and passive fund categories. | Active vs passive fund flows is a comparison frame, while passive flows define the passive or rules-based side as a market-structure channel. |

| Volatility targeting | Rules-based exposure adjustment tied to volatility conditions. | It can create systematic flow pressure, but its trigger is volatility control rather than passive benchmark ownership alone. |

Related Concepts to Read Next

Use passive flows as the starting point for the broader flow category. Use ETF flows when the question is specifically about ETF wrapper behavior, creations, redemptions, or secondary-market pressure. Use active-vs-passive fund flows when the question is about allocation style categories and how capital shifts between active and passive management. Use volatility targeting when the flow pressure comes from rules-based exposure changes tied to volatility inputs.