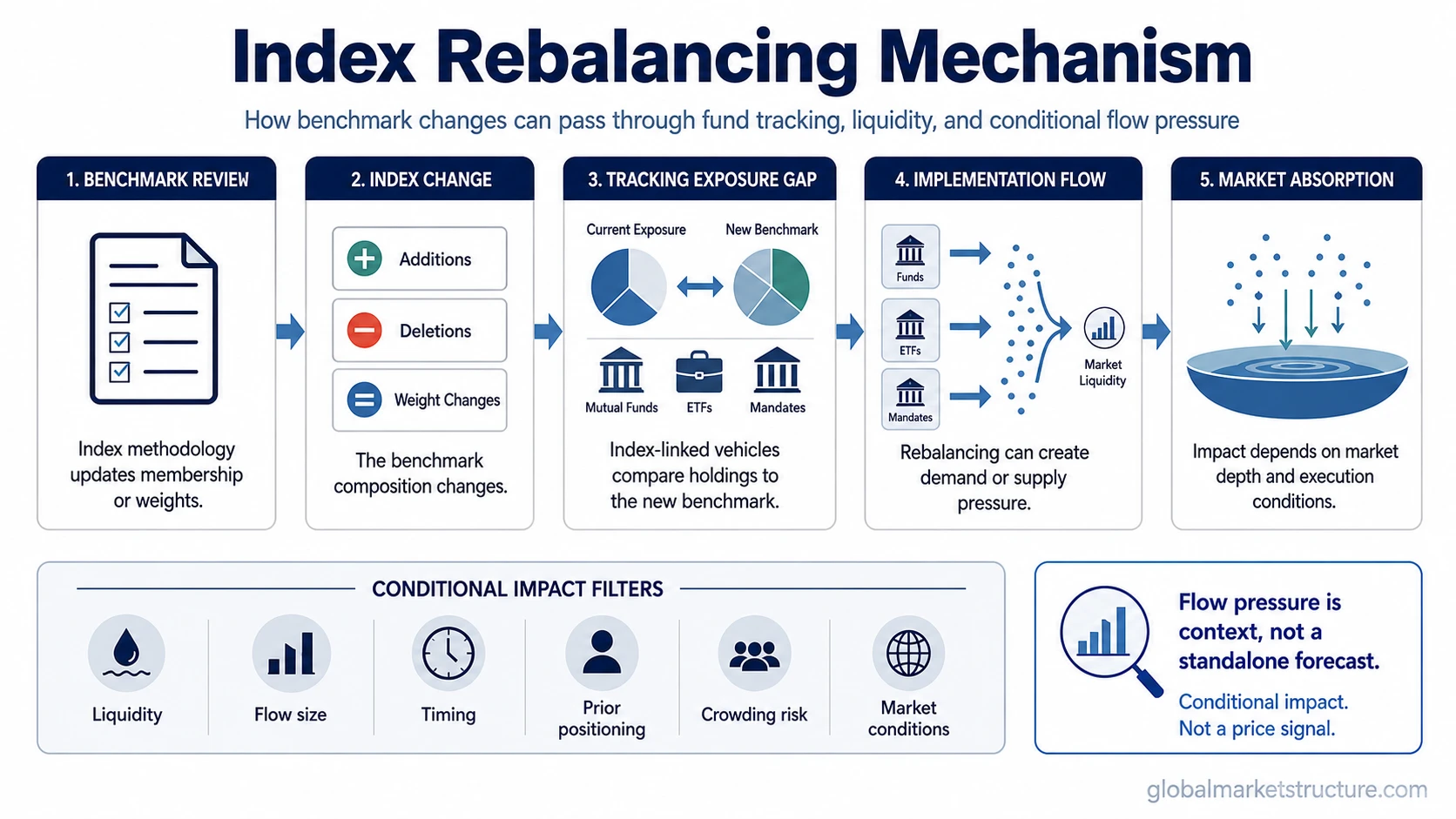

Index rebalancing is the rule-based adjustment of an index’s constituents or weights. When a benchmark changes, funds and other vehicles that track that benchmark may need to adjust exposure, which can create temporary demand or supply pressure. The market impact is conditional: liquidity, flow size, timing, prior positioning, and implementation all matter.

Core idea: index rebalancing begins as a benchmark mechanism and can become a market-flow mechanism when benchmark-linked exposure has to adjust. It can help explain why trading pressure appears around certain securities or sectors, but it does not predict price direction by itself.

Key Points

- Index rebalancing changes benchmark membership or weights according to index rules.

- Benchmark-tracking vehicles may adjust exposure when those changes become effective.

- Flow pressure depends on liquidity, benchmarked exposure, timing, and prior crowding.

- Additions and deletions can matter, but the outcome depends on market absorption.

- The useful reading is market-structure pressure, not a standalone forecast.

What Index Rebalancing Is and Is Not

Index rebalancing belongs to the benchmark layer. The benchmark methodology defines what should be included and how it should be weighted. The market effect comes later, when funds, mandates, derivatives, or other benchmark-linked exposures respond to the revised composition.

| Reading | Correct interpretation | Not the same as |

|---|---|---|

| Index composition changes | A benchmark may add, delete, or resize exposure to securities or groups. | A discretionary investment thesis. |

| Benchmark-tracking adjustment | Index-linked vehicles may need to align holdings or exposure with the revised benchmark. | A guaranteed trade in every related security. |

| Temporary demand or supply pressure | Flow pressure can appear when required adjustment is large relative to available liquidity. | A price forecast or buy/sell signal. |

| Event timing | Announcement and effective dates can concentrate attention and execution. | A complete explanation of price movement before or after the event. |

| Capital-flow route | Index rebalancing is one route through which benchmark rules can influence market flow. | Corporate demand, personal portfolio rebalancing, or ETF share creation by itself. |

How Index Rebalancing Can Create Flow Pressure

Step 1: a benchmark review changes index composition, membership, or weights.

Step 2: funds, mandates, or instruments linked to that benchmark compare current exposure with the new benchmark structure.

Step 3: implementation can create demand for securities with higher benchmark weight and supply for securities with lower benchmark weight or deletion risk.

Step 4: the market absorbs that flow through regular trading, block activity, auctions, or other execution channels.

Step 5: price pressure may appear if required flow is large relative to liquidity, but the effect can be muted, anticipated, delayed, or offset by other participants.

The stronger market-structure question is whether benchmark-linked flow is large enough to matter against available liquidity, and whether other participants have already positioned for the event.

What Traders and Investors Can Observe

Index rebalancing becomes easier to interpret when the mechanics are separated from the market read. The event may be known, but the price effect still depends on how much exposure must move, how liquid the affected securities are, and how crowded the trade has become before implementation.

| Observable area | Why it matters | Interpretation limit |

|---|---|---|

| Announcement date | Starts the period when market participants can anticipate additions, deletions, or weight changes. | Awareness does not prove that all flow has occurred. |

| Effective date | Concentrates benchmark implementation pressure around a specific window. | Some participants may trade before or after the effective date. |

| Additions and deletions | Show where benchmark membership changes may create demand or supply. | Membership change does not automatically determine price direction. |

| Weight change size | Larger weight changes can require more exposure adjustment. | Large weights matter less if the market is deep enough to absorb flow. |

| Benchmarked exposure | More assets tracking or referencing the benchmark can increase potential implementation flow. | Exact exposure requires source verification before adding figures or estimates. |

| Liquidity and average trading activity | Thin liquidity can make the same required flow more disruptive. | Liquidity can change during the event window. |

| Closing-auction activity | Some implementation can concentrate near benchmark pricing windows. | Auction activity can reflect many motives, not only index rebalancing. |

| Prior crowding | Anticipatory positioning can pull forward part of the expected move. | Crowding can reverse, continue, or be absorbed without a clean pattern. |

| Broader market liquidity | Market-wide liquidity affects how easily rebalance flow is absorbed. | Macro liquidity does not isolate the effect of one index event. |

Why Rebalancing Can Be Misread

Common mistake: treating index additions as automatic upside and deletions as automatic downside.

Index rebalancing can create demand and supply pressure, but the visible result depends on liquidity, execution timing, prior positioning, valuation context, and other market flows. If traders buy the expected addition before implementation, the effective-date flow may already be partly reflected in price. If liquidity is deep, even a large benchmark change may be absorbed with limited disruption.

The same event can therefore produce different outcomes. A security can be added to an index and still weaken if the broader market is under pressure, if expected flow was crowded in advance, or if unrelated sellers dominate. A deletion can create supply pressure without producing a clean decline if buyers are already prepared to absorb it.

Index Rebalancing vs Related Flow Routes

Index rebalancing should be separated from ETF flows. ETF flows describe capital entering or leaving ETF wrappers and how that can connect to secondary-market trading, primary-market creation and redemption, and underlying exposure. Index rebalancing is about benchmark composition or weight changes.

It also differs from stock buybacks, where the demand route comes from corporate capital allocation rather than benchmark methodology. Both can create structural demand, but the source of the flow is different.

Adjacent rebalancing routes need their own interpretation. Pension fund rebalancing pressure can come from allocation drift between asset classes, while month-end and quarter-end rebalancing flows usually relate to calendar-driven portfolio adjustment. Index rebalancing is narrower because the benchmark itself changes.

Example Scenario

A benchmark announces several additions and deletions ahead of an effective date. Securities expected to receive higher benchmark weight attract attention because index-linked vehicles may need more exposure. The incomplete read is to assume that the additions must rise into the event.

If many participants already anticipated the change, part of the expected demand may have been pulled forward. If liquidity is thin, pressure may still appear near implementation. If broader market liquidity weakens, unrelated selling may dominate the rebalance flow. The stronger interpretation compares the expected benchmark adjustment with liquidity, crowding, timing, and surrounding market conditions.

FAQ

What is index rebalancing?

Index rebalancing is the rule-based adjustment of an index’s constituents or weights. It can include additions, deletions, or changes in how much influence each component has inside the benchmark.

Does index rebalancing force funds to trade?

Funds or mandates that closely track a benchmark may need to adjust exposure, but implementation can vary. Some may trade before the effective date, some may use different execution methods, and some exposure may be managed through instruments rather than simple cash equity trades.

Do stocks added to an index always rise?

No. An addition can create potential demand, but price direction depends on liquidity, prior positioning, broader market pressure, valuation context, and whether the expected flow was already anticipated.

How is index rebalancing different from ETF flows?

Index rebalancing starts with benchmark composition or weight changes. ETF flows start with money moving into or out of an ETF wrapper. The two can interact, but they are not the same mechanism.

Why can rebalancing pressure fade after the event?

Pressure can fade when the required benchmark-linked adjustment has been completed, when liquidity absorbs the flow, or when anticipatory positioning unwinds. The result is conditional, not automatic.