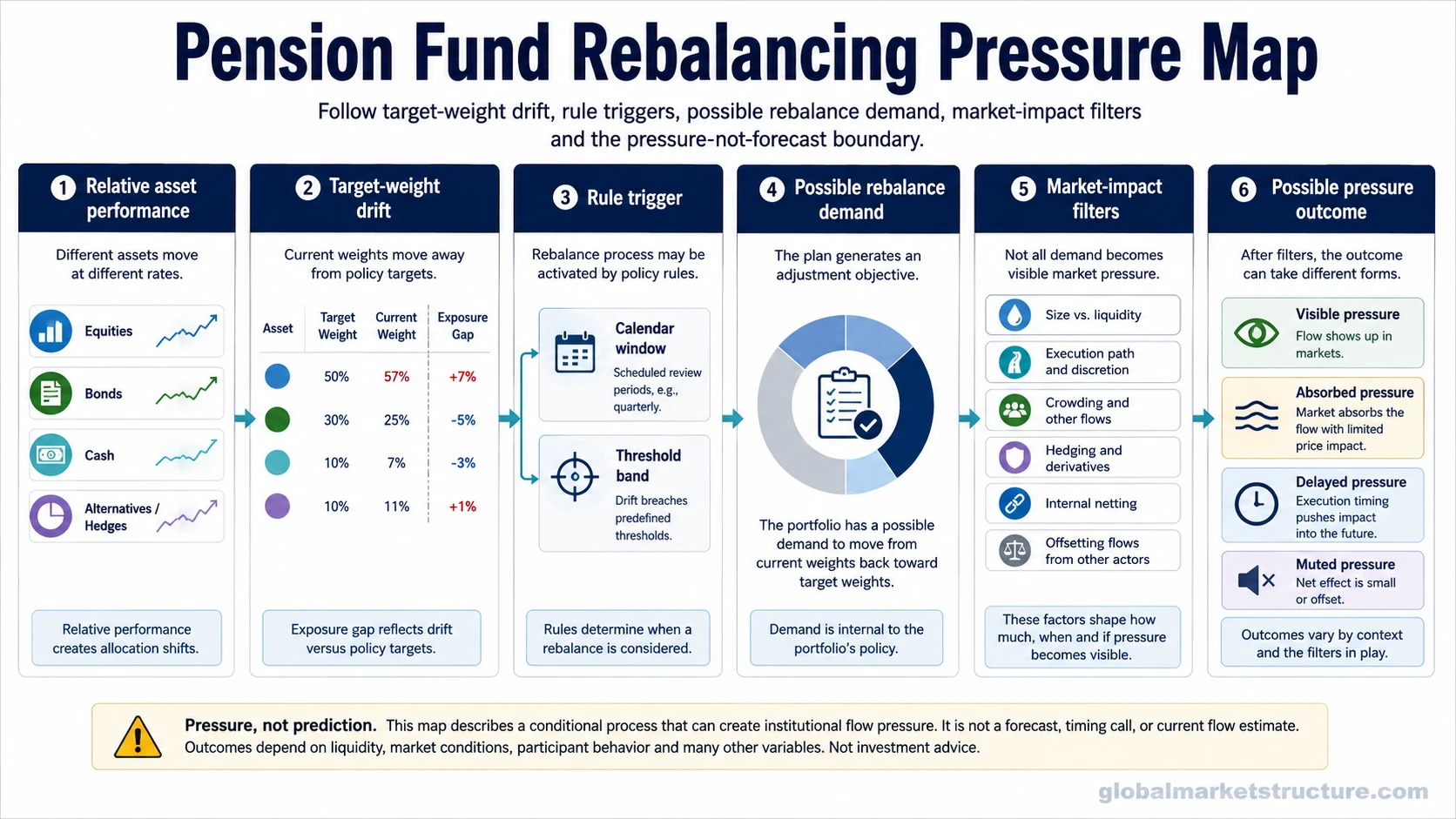

Pension fund rebalancing means an institutional portfolio may adjust exposures after market performance moves its asset weights away from target allocations. In market-structure analysis, the useful reading is possible flow pressure, not a forecast, because trade size, liquidity, execution, timing, crowding, and offsetting flows shape whether the pressure becomes visible.

Definition: Pension fund rebalancing is the process of moving a pension portfolio back toward its target exposure after relative performance, cash flows, hedge adjustments, or policy rules create an allocation gap.

The market-structure question is not simply whether a pension fund has a target allocation. The stronger question is whether the gap between current weights and target weights is large enough to create demand that matters relative to market depth.

Key Points

- Pension fund rebalancing can create institutional flow pressure when target weights drift after relative asset performance.

- Calendar windows and threshold rules may help identify timing, but they do not prove direction, size, or visible impact.

- Market impact depends on liquidity, execution discretion, crowding, hedging, and offsetting flows.

- The concept is pressure evidence, not a standalone market forecast or allocation instruction.

Pension Fund Rebalancing Meaning

A pension fund usually manages assets against a policy mix, such as a target balance between equities, bonds, alternatives, cash, and hedges. When one asset class rises or falls faster than another, the portfolio weight can drift away from that target.

If equities rise sharply while bonds lag, the equity share of the portfolio may move above target. A rebalance rule can then create possible equity-sale demand, bond-buy demand, hedge adjustment, or internal cash movement. The same logic can work in the opposite direction after equity weakness or bond strength.

Rebalance demand is not the same as visible price pressure. Large institutions may spread execution, use derivatives, adjust hedges, net flows internally, or meet the rebalance against other market participants taking the other side.

The Common Mistake: Treating Rebalancing As A Forecast

Common mistake: A quarter-end or month-end date does not automatically mean pension funds will push markets in one direction.

Better reading: Calendar timing can define a possible window. The pressure reading still needs evidence of asset-weight drift, rule sensitivity, trade size, liquidity conditions, execution behavior, and offsetting flows.

Rebalancing can be predictable enough for market participants to discuss, but predictability does not remove uncertainty. A known window may also reduce visible impact if dealers, asset managers, hedge funds, or other institutions position ahead of it or absorb the flow.

Pension rebalancing belongs inside capital-flow interpretation because it helps classify a possible source of institutional demand without turning the reading into a market call.

How Target-Weight Drift Can Create Flow Pressure

The mechanism starts with relative performance. A large equity rally can lift the equity share of a pension portfolio above its policy target. A large bond rally, equity drawdown, or currency move can create a different gap. The rebalance question begins only after current exposure no longer matches intended exposure.

Mechanism sequence: relative performance drift, target exposure gap, calendar or threshold rule, possible rebalance demand, execution and liquidity filter, then visible, absorbed, delayed, or offset pressure.

Each step can weaken the final reading. A large exposure gap may not matter if execution is slow. A scheduled rebalance may not matter if the drift is small. A visible imbalance may not move prices if liquidity is deep or if other flows offset it.

Calendar Rules vs Threshold Rules

Calendar rules are tied to scheduled review points, often around month-end, quarter-end, or other policy dates. They matter because many institutions evaluate exposures at similar points in time, which can concentrate attention around a visible window.

Month-end and quarter-end are review windows, not proof that the final trade occurs on one date. Execution can be gradual, discretionary, or partly handled through instruments that do not create a single visible cash-market event.

Threshold rules are tied to the size of the allocation drift. A fund may tolerate small deviations but rebalance when an asset class moves beyond a policy band. Threshold logic can make rebalancing less tied to the calendar and more tied to market movement.

| Rule type | What it can show | What it cannot prove |

|---|---|---|

| Calendar rule | Timing may be visible around a review window. | The amount of demand still depends on the size of the drift. |

| Threshold rule | The trigger depends on whether exposure moves outside a policy band. | Exact execution timing may be less visible. |

| Shared limitation | Both rules can help identify possible pressure. | Neither rule proves final market impact without liquidity, size, and execution context. |

What Decides Whether Pressure Becomes Visible

A pension rebalancing estimate becomes more useful when the pressure can be separated into conditions, implications, and limitations. The same headline number can mean different things in a deep market, a thin market, a crowded positioning window, or a period with strong offsetting flows.

| Condition | Possible implication | Limitation |

|---|---|---|

| Large asset drift | Current exposure may sit far from policy target. | Drift alone does not prove immediate execution. |

| Target exposure gap | A rebalance rule may create possible demand. | The fund may use bands, discretion, derivatives, or internal netting. |

| Calendar window | Attention may cluster around month-end or quarter-end. | A visible date does not prove direction or magnitude. |

| Size versus liquidity | Pressure matters more when demand is large relative to market depth. | Deep liquidity can absorb flows with limited visible impact. |

| Crowding and predictability | Other participants may anticipate the rebalance window. | Anticipation can amplify, dilute, or shift the timing of the final pressure. |

| Offsetting flows | Other institutions may take the opposite side. | Net market impact can be much smaller than gross demand. |

| Execution discretion | Trades can be spread across time, instruments, or venues. | Reported pressure may not appear as a single visible market event. |

Pension Rebalancing Example In Market Context

Equities rally strongly into a quarter-end window while bonds lag. A pension portfolio that targets a balanced equity and bond exposure may now sit above its equity target and below its bond target. That creates a plausible rebalancing-pressure reading: some equity exposure may need to be reduced and some bond exposure may need to be restored.

The reading remains incomplete unless market depth, trade size, execution path, hedge use, and offsetting flows are checked. The pressure may become visible if several large funds face similar gaps in a thin liquidity window. It may weaken if execution is gradual, if derivatives absorb part of the adjustment, or if other institutions provide the opposite demand.

A similar exposure gap can produce visible pressure, muted pressure, or no clear market effect depending on the surrounding flow environment.

How It Relates To Passive Flows And Index Rebalancing

Pension rebalancing is one part of broader institutional allocation behavior. Passive flows describe broader rule-based or allocation-driven movement into and out of market exposure, while pension rebalancing focuses on target-weight drift inside large retirement pools.

Index rebalancing is different because it usually comes from benchmark membership, float, weight, or methodology changes. Pension rebalancing comes from an institutional portfolio moving back toward its own target exposures.

Current rebalancing estimates, named cost figures, and claims about a specific month-end or quarter-end flow need dated source support before they are used as evidence.

FAQ

Does pension fund rebalancing predict market direction?

No. It can identify a possible source of institutional flow pressure, but direction, timing, size, and visible market impact depend on liquidity, execution, crowding, and offsetting flows.

Why do month-end and quarter-end windows matter?

They can matter because some institutions review exposure near scheduled reporting or policy windows. The date alone is not enough to prove that a large trade or market move will occur.

When is pension rebalancing pressure more likely to matter?

The pressure reading carries more weight when asset-weight drift is large, multiple funds face similar exposure gaps, market depth is thin, and offsetting demand is limited.

How is pension fund rebalancing different from index rebalancing?

Pension fund rebalancing comes from portfolio exposure drifting away from target weights. Index rebalancing comes from benchmark rules such as membership, float, or index-weight changes.