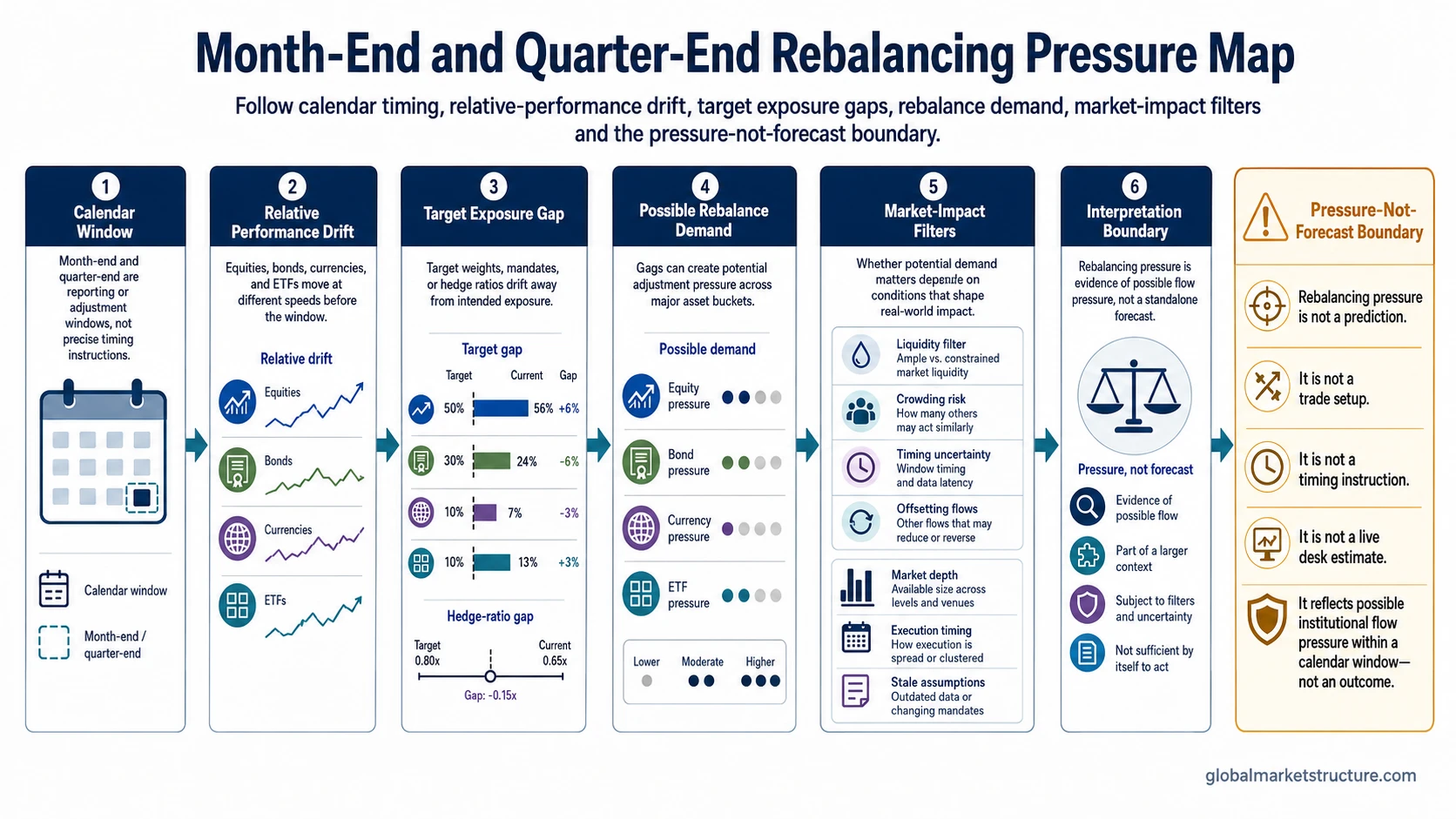

Month end rebalancing is a calendar-linked market-flow window when institutions, pensions, balanced funds, passive vehicles, ETFs, or hedged portfolios may adjust exposures after relative performance changes target weights or hedge ratios. The pressure can affect equities, bonds, currencies, or ETFs, but it is not a standalone forecast.

Definition: Month-end and quarter-end rebalancing refers to exposure adjustment near a reporting or calendar window after market moves create drift from intended weights, benchmarks, or hedge settings. The flow can create temporary demand or supply pressure, while final market impact still depends on size, liquidity, pre-positioning, execution timing, and opposing flows.

Key Points

- Month-end and quarter-end rebalancing can create allocation or hedge-adjustment flow pressure.

- The likely direction often depends on relative performance before the rebalance window.

- Target weights, hedge ratios, pension allocations, passive mandates, ETFs, and index-linked exposures can contribute to adjustment demand.

- Market depth, positioning, execution timing, and opposing demand can weaken or change the visible impact.

- Rebalancing pressure is evidence of possible flow, not a standalone forecast.

What Month End Rebalancing Means

In market-flow analysis, month end rebalancing describes the adjustment that can occur when portfolio weights, hedge ratios, or passive allocations drift away from their intended settings before a month-end or quarter-end window closes. If one asset class strongly outperforms another, the resulting weight change can create a need to reduce the outperforming exposure and add to the underweighted exposure.

Quarter-end can attract more attention than an ordinary month-end window because several adjustment processes may overlap. Pension allocations, balanced-fund reweights, passive exposure changes, ETF-related flows, hedge adjustments, and reporting-period positioning can cluster near the same window. The calendar window identifies where pressure may concentrate, not where price must move.

How Rebalancing Pressure Forms

Rebalancing pressure usually begins with relative performance drift. When equities, bonds, currencies, or other exposures move at different speeds, the actual mix can move away from the intended exposure. A mandate, target weight, benchmark, or hedge ratio can then create possible demand to restore the exposure mix.

The mechanism is conditional. A strong equity rally into quarter-end may create estimated equity-reduction and bond-addition pressure for some target-weighted investors. A sharp currency move may create hedge-ratio adjustment pressure for currency-hedged portfolios. A large move in ETF or passive exposures may also interact with broader passive flows if allocation-driven demand appears near the same window.

The useful distinction is between possible flow and realized market impact. A rebalance estimate can identify where demand or supply may appear, but it cannot determine how much has already been executed, how much has been anticipated, or how much opposing demand exists on the other side.

Condition vs Interpretation Table

A stronger rebalancing read separates the condition, the possible flow pressure, and the interpretation limit. The same calendar window can mean very different things when market depth, positioning, timing, or opposing flows change.

| Condition | Possible Pressure | Interpretation Limit |

|---|---|---|

| Equities outperform bonds before quarter-end. | Target-weighted institutions or balanced funds may need to reduce equity exposure and add bond exposure. | The pressure can be absorbed if equity demand remains strong, liquidity is deep, or other flows offset the imbalance. |

| Bonds outperform equities before quarter-end. | Some allocation models may imply bond reduction and equity addition. | The actual effect depends on mandate size, tolerance bands, execution method, and whether managers adjust immediately or gradually. |

| FX hedge ratios drift after currency or cross-asset moves. | Hedged portfolios may need to adjust currency exposure near month-end or quarter-end windows. | FX liquidity, dealer positioning, fixing-window behavior, and unrelated currency flows can blur the impact. |

| A rebalance estimate becomes widely anticipated. | Positioning may adjust before the actual rebalance flow appears. | Crowding can reduce the clean impact because the expected pressure may already be reflected in positioning. |

| Liquidity is deep and offsetting flows are large. | Estimated demand or supply may still exist, but market depth can absorb it more easily. | A large estimated flow may have limited visible impact when other flows, dealer balance sheets, or risk demand take the opposite side. |

| Execution is spread across several sessions. | Pressure may appear gradually rather than in one visible burst. | The calendar window can remain relevant while the exact timing of price impact stays uncertain. |

Why Rebalancing Flow Is Not a Forecast

Rebalancing flow is a pressure estimate, not a directional forecast. A possible equity-sell imbalance does not prove that equities must fall, and a possible bond-buy imbalance does not prove that bonds must rise. The final response depends on whether the flow still needs execution, whether positioning already moved ahead of the window, and whether other demand or supply appears at the same time.

Limitation: Rebalancing pressure becomes more relevant when incremental demand or supply still needs to be executed into limited liquidity. It weakens when the expected flow is already crowded, execution is spread over time, market depth is strong, or offsetting flows appear around the same window.

Model staleness is another risk. A rebalance estimate based on earlier market moves can lose relevance if prices, yields, currency levels, hedge ratios, or positioning change before execution. A pressure estimate should be updated by the current structure of liquidity and flow, not treated as a fixed prediction.

Common Failure Mode

Common mistake: Treating a calendar rebalance estimate as a direct market call. The window can draw attention to possible demand or supply, but attention is not the same as executable pressure.

Illustrative scenario: Equities outperform bonds into quarter-end. A target-weighted institutional portfolio may need to reduce equity exposure and add bond exposure to restore allocation. That can create estimated equity-sell and bond-buy pressure, but the visible market effect can be muted if liquidity is deep, other flows offset the pressure, or positioning already adjusted before the window.

The estimate still has value when it clarifies where pressure may appear. The mistake is using the estimate alone, without checking whether the flow remains unexecuted, whether market depth can absorb it, and whether another flow is moving in the opposite direction.

How It Connects to Index Rebalancing and Passive Flows

Month-end and quarter-end rebalancing belongs inside the broader flow landscape, but it is narrower than the full passive-flow universe. It focuses on calendar windows where target weights, hedge ratios, or reporting-period adjustments may create concentrated demand or supply.

Index rebalancing is a different mechanism because it centers on benchmark composition, index additions, deletions, and benchmark-tracking demand. Month-end and quarter-end rebalancing usually center on restoring exposures after relative performance creates drift.

The cleanest reading keeps the mechanisms separate: passive allocation flows explain broad mechanical demand, index rebalancing explains benchmark-event pressure, and month-end rebalancing explains calendar-window adjustment pressure.

FAQ

Does month end rebalancing predict market direction?

No. Month end rebalancing can identify possible flow pressure, but it does not predict final market direction by itself. Market depth, positioning, execution timing, and offsetting flows can all change the visible market impact.

Why can quarter-end rebalancing matter more than month-end rebalancing?

Quarter-end can matter more because pension adjustments, balanced-fund reweights, passive allocation checks, hedge changes, ETF flows, and reporting-period activity may cluster around the same window.

What makes a rebalancing flow estimate weaker?

A rebalancing flow estimate becomes weaker when the expected pressure is already anticipated, when liquidity is deep, when execution is spread across sessions, when model assumptions become stale, or when other flows offset the estimated imbalance.