Stock buybacks are company share repurchases: a company uses cash to buy back its own shares. They can reduce shares outstanding and influence per-share metrics, but authorization is not the same as execution, and market impact depends on whether real repurchases reach the market in size that matters relative to liquidity and absorption.

Definition: A stock buyback, also called a share repurchase, is a corporate action where a company repurchases shares that it previously issued. The company may retire those shares or hold them as treasury shares, depending on the accounting and corporate structure.

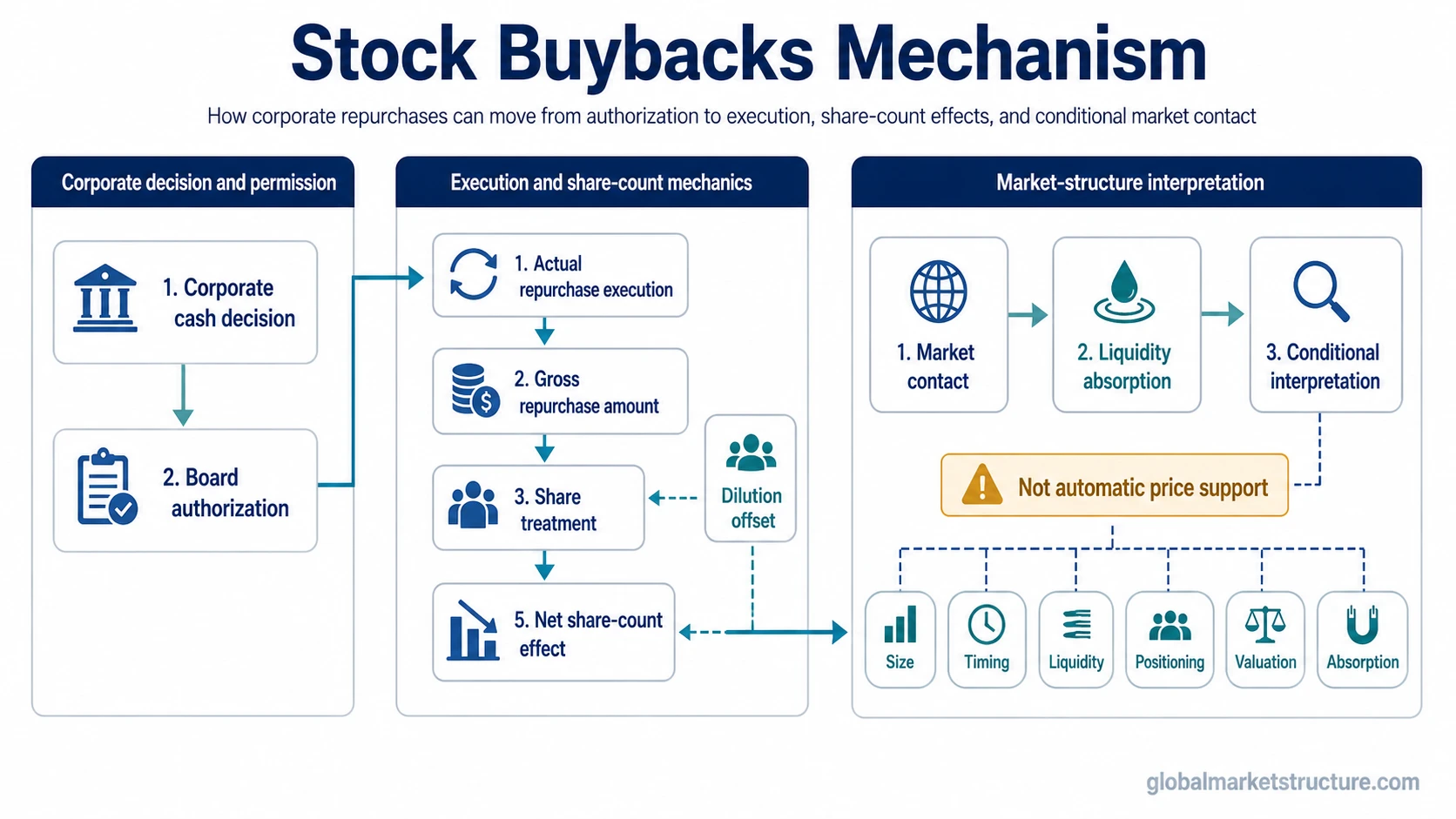

The useful distinction is simple: a buyback announcement gives permission, while actual repurchase activity is the part that can touch the market. Even then, the effect is conditional. Execution scale, timing, liquidity, valuation, prior positioning, and new share issuance can all change the interpretation.

Key Points

- Stock buybacks are company repurchases of their own shares.

- A buyback authorization does not guarantee that the full amount will be executed.

- Gross repurchase spending is different from net share-count reduction because dilution can offset part of the effect.

- Buybacks can become an equity-demand flow only when actual purchases reach the market and matter relative to liquidity.

What Are Stock Buybacks?

Stock buybacks are a form of capital return. Instead of distributing cash directly through a dividend, the company uses cash to repurchase its own shares. If the repurchased shares are retired, the remaining ownership base can become smaller.

The basic share-count effect is mechanical, but the market interpretation is not. A lower share count can raise per-share metrics such as earnings per share if net income stays the same, but that does not mean the business itself improved. It means the same total earnings are being divided across fewer shares.

That distinction matters because buybacks are often discussed as if they automatically create shareholder value or price support. A cleaner interpretation separates the accounting effect, the capital-allocation decision, and the market-flow effect.

How Stock Buybacks Work

A buyback usually begins with board authorization. The authorization sets a maximum amount, share count, or program structure, but it does not force the company to buy every share immediately. Management may execute the program gradually, pause it, accelerate it, or leave part of it unused.

Execution can happen through open-market repurchases, tender offers, accelerated share repurchase agreements, or other approved methods. Open-market repurchases are common because they allow the company to buy shares over time rather than in one single transaction.

The full mechanism has several steps:

| Step | What happens | Why it matters |

|---|---|---|

| Authorization | The company approves a repurchase program. | The headline creates permission, not guaranteed market demand. |

| Execution method | The company buys shares through open-market activity, a tender offer, or another structure. | Only executed purchases can become direct market contact. |

| Gross repurchase amount | The company spends cash to acquire shares. | Gross spending can look large before dilution and issuance are considered. |

| Share treatment | Shares may be retired or held as treasury shares. | The share-count effect depends on how the repurchased shares are handled. |

| Net share-count effect | Shares outstanding may decline if repurchases exceed new issuance and compensation-related dilution. | Net reduction matters more than the headline buyback amount. |

| Market-flow interpretation | Executed repurchases may add demand during the period when they are carried out. | The market effect depends on execution scale and the market’s ability to absorb the flow. |

Authorization, Execution, and Net Share Count

The headline authorization is often the least precise part of a buyback program. A company can authorize a large repurchase plan, but the market-flow effect depends on actual execution, not the headline number alone.

Gross repurchases also need to be separated from net share-count reduction. A company may buy back shares while also issuing shares through stock-based compensation, option exercises, acquisition-related issuance, or employee plans. In that case, part of the buyback offsets dilution rather than reducing the ownership base meaningfully.

| Term | Clean interpretation | Common mistake |

|---|---|---|

| Buyback authorization | Permission to repurchase up to a stated amount or structure. | Treating the full authorization as already executed demand. |

| Actual repurchase | Shares bought back during a period. | Ignoring whether the buying occurred gradually or only partially. |

| Gross buyback amount | Total cash spent on repurchases before dilution adjustments. | Assuming gross dollars equal net shareholder benefit. |

| Net share-count reduction | The actual decline in shares outstanding after issuance and dilution. | Ignoring stock compensation or new issuance. |

| Dilution offset | Repurchases used to neutralize new shares issued elsewhere. | Calling every buyback a full reduction in the ownership base. |

| Market-flow effect | Potential demand created when real purchases enter the market. | Assuming accounting activity always creates price pressure. |

Why Companies Use Stock Buybacks

Companies may use buybacks for several reasons. A repurchase can return excess cash, adjust capital structure, offset dilution, support per-share metrics, or reflect a capital-allocation choice when management decides that repurchasing shares is preferable to other uses of cash.

Those motives should not be treated as automatic proof of value. A buyback can be sensible when the balance sheet remains healthy, reinvestment needs are not being starved, and shares are repurchased at reasonable prices. It can be weaker when it is debt-funded, poorly timed, used mainly to mask dilution, or done at valuations that reduce future shareholder benefit.

Capital-allocation lens: A buyback can convert corporate cash into reduced share count or per-share metric support, but only under conditions where execution is real, dilution does not offset the effect, and the company is not weakening its balance sheet or reinvestment capacity.

Buybacks, EPS, and Share Count

The earnings-per-share effect is one of the most common reasons buybacks receive attention. If net income is unchanged and the share count falls, earnings per share can rise because the same earnings are spread over fewer shares.

That effect is not the same as operating improvement. Revenue, margins, cash flow, competitive position, and balance-sheet quality can remain unchanged while EPS rises mechanically. The useful question is whether EPS support comes from genuine business strength, capital allocation, or mostly from share-count math.

Share-count quality matters more than the headline. A company that spends heavily on buybacks while issuing many new shares may show less net reduction than the repurchase amount suggests. That is why gross repurchase dollars should be read alongside shares outstanding, dilution, cash flow, and balance-sheet context.

Stock Buybacks vs Dividends

Buybacks and dividends are both ways to return capital, but they work differently. A dividend sends cash directly to shareholders. A buyback uses corporate cash to repurchase shares, which may reduce share count and change per-share metrics.

| Feature | Stock buybacks | Dividends |

|---|---|---|

| Capital-return form | Company repurchases its own shares. | Company distributes cash directly to shareholders. |

| Flexibility | Programs can be adjusted, paused, or executed opportunistically. | Regular dividends can create a stronger expectation of continuity. |

| Per-share effect | Can reduce shares outstanding if repurchases exceed dilution. | Does not directly reduce share count. |

| Market-flow relevance | Can create market contact when shares are actually repurchased. | Primarily a cash-distribution event, not direct corporate share buying. |

| Main interpretation risk | Confusing authorization with execution or gross spending with net reduction. | Assuming a dividend policy is always permanent or risk-free. |

Neither method is automatically superior. The interpretation depends on business quality, valuation, balance sheet, reinvestment opportunity, tax context, and how consistently the capital-return policy is funded.

Why Buybacks Are Not Automatically Bullish

A buyback can add demand, reduce share count, and improve per-share metrics, but those effects are conditional. The strongest mistake is treating the announcement as if the market has already absorbed the full program.

Limitation: Stock buybacks are not automatically bullish. An authorization may not be fully used, execution may be slow, repurchases may only offset dilution, and the buying may be too small relative to market liquidity to create meaningful pressure.

Valuation also changes the interpretation. Repurchasing shares at attractive prices can be different from repurchasing aggressively when the stock is expensive or when the company has better uses for capital. Funding matters as well. A buyback financed by excess cash is not the same as one that increases balance-sheet risk.

Market conditions matter because even real buying can be absorbed. If liquidity is deep and selling pressure is large, corporate repurchases may have limited visible effect. If liquidity is thin and execution is large relative to traded volume, the same program can matter more for flow interpretation.

Simple Stock Buyback Example

A company authorizes a large repurchase program, but executes only part of it over several quarters. During the same period, new shares are issued through stock-based compensation. The headline buyback amount looks large, yet the net share-count reduction is smaller because part of the repurchase offsets dilution.

The market-flow effect can also be muted if normal liquidity absorbs the buying. The cleaner reading separates four layers: the authorization, the executed repurchases, the net change in shares outstanding, and whether the actual buying was large enough to influence supply-demand conditions during execution.

How Buybacks Fit Market-Structure Interpretation

Buybacks matter for market-structure interpretation because executed repurchases can become one source of equity demand. The important word is “can.” A corporate repurchase program has to move from approval to execution before it becomes market contact.

When actual repurchases are meaningful, they can affect the flow backdrop. They may absorb some supply during execution and reduce the share count over time if repurchases are not offset by issuance or dilution. The interpretation becomes stronger when execution is large relative to liquidity, persistent across reporting periods, and visible in shares outstanding rather than only in announcements.

When repurchases are small, delayed, offset by dilution, or absorbed by normal liquidity, the market-structure relevance is weaker. In those cases, buybacks remain part of the capital-allocation picture, but they should not be treated as a decisive market force.

Buyback yield compares repurchases with market value, which makes the size of a repurchase program easier to compare across companies and periods.

Related Flow Mechanisms

Stock buybacks are corporate capital-allocation flows. They are not passive, benchmark-linked, or rules-based fund flows because the decision begins inside the company rather than inside an index methodology, fund mandate, or volatility rule.

Index rebalancing begins with benchmark changes that can force tracking portfolios to adjust exposures. A stock buyback begins with a corporate decision to repurchase shares.

Volatility targeting adjusts exposure through a rules-based response to realized or expected volatility. Buybacks are not rules-based exposure targeting, but they can still matter as a conditional demand source when actual repurchases are executed.

Clean distinction: Buybacks are corporate repurchase flows. Index rebalancing is benchmark-linked flow. Volatility targeting is rules-based exposure adjustment. All three can affect market structure, but the trigger, timing, and interpretation are different.

FAQ

What is a stock buyback?

A stock buyback is a company repurchasing its own shares. It can reduce shares outstanding if the repurchased shares are retired and if new issuance or dilution does not offset the effect.

Is a buyback authorization the same as an actual buyback?

No. A buyback authorization gives the company permission to repurchase shares, but actual execution depends on whether the company buys shares, how much it buys, and when the purchases occur.

Do stock buybacks always increase EPS?

No. EPS can rise if net income is unchanged and the share count falls, but the effect depends on actual net share-count reduction. New issuance, stock compensation, or weaker earnings can offset the mechanical benefit.

Are stock buybacks automatically bullish?

No. Buybacks can add demand or reduce share count under the right conditions, but market impact depends on execution, size, timing, valuation, dilution, liquidity, positioning, and absorption.