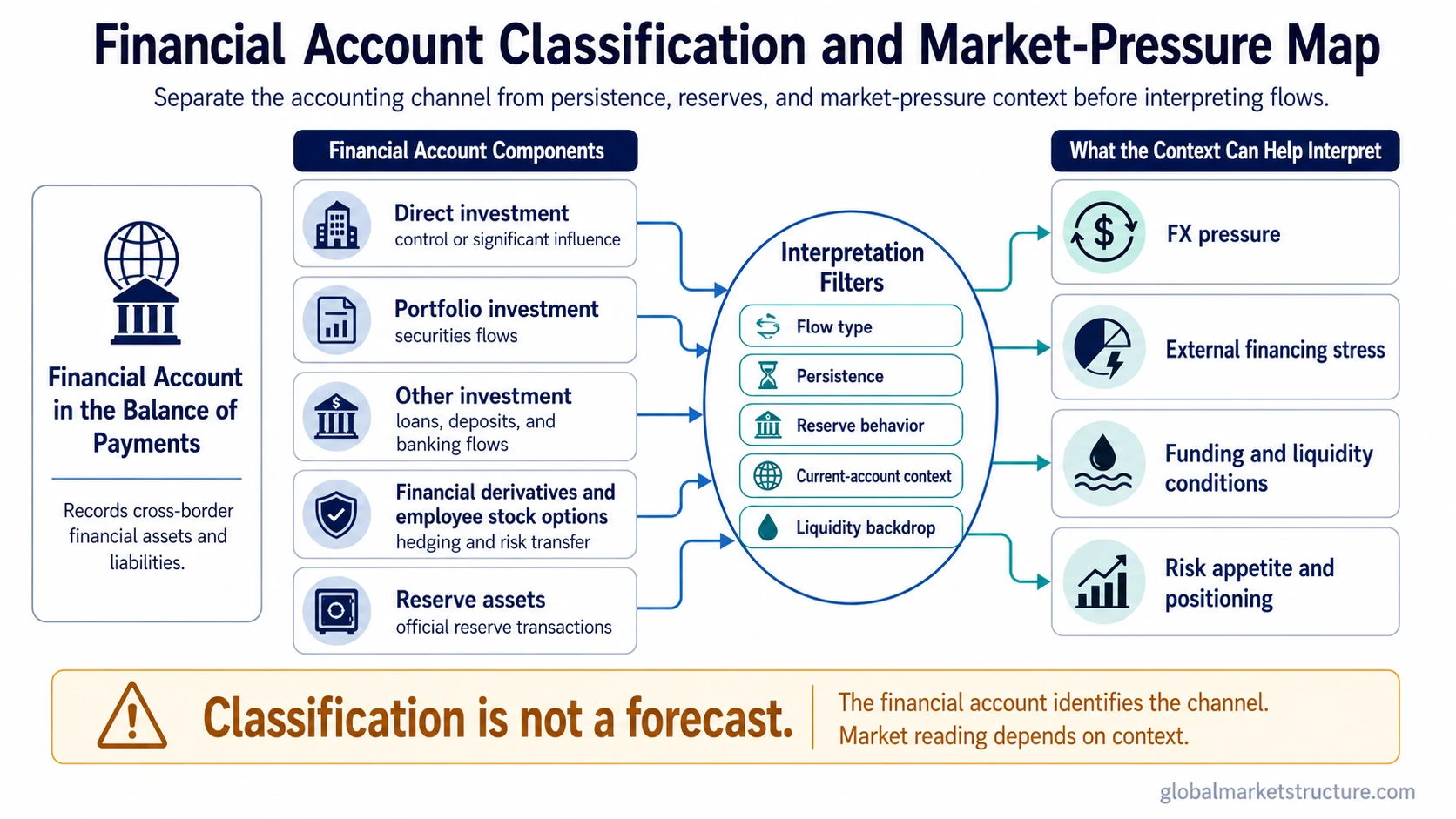

The financial account in the balance of payments records cross-border transactions in financial assets and liabilities. It includes direct investment, portfolio investment, other investment such as loans and deposits, financial derivatives, employee stock options where classified in the financial account, and reserve assets. For market interpretation, it helps classify capital-flow pressure, but it does not by itself forecast currency direction, liquidity stress, or market returns.

Definition: The financial account is the balance-of-payments category that records how residents and non-residents acquire, reduce, or transfer financial claims across borders.

The account separates financial transactions from trade in goods and services, but it does not give every flow the same market meaning. A direct investment flow, a portfolio allocation, a banking-flow adjustment, a derivatives position, and an official reserve transaction can all appear inside the financial account while pointing to different pressures.

Key Points

- The financial account records cross-border financial asset and liability transactions.

- The main components are direct investment, portfolio investment, other investment, financial derivatives and employee stock options, and reserve assets.

- The account helps classify capital flows, but it is not a standalone market signal.

- Market interpretation depends on flow type, persistence, reserve behavior, external balance, and liquidity context.

What the Financial Account Records

The financial account records changes in ownership of financial assets and liabilities between residents of one economy and the rest of the world. In simple terms, it tracks how financial claims move across borders: equity ownership, debt securities, loans, deposits, trade credit, derivatives exposure, employee stock options where relevant, and official reserve assets.

The classification matters because the same headline direction can hide different behavior. A portfolio inflow into government bonds is not the same as a direct investment project. A banking outflow is not the same as a reserve-asset change. The account identifies the channel first; interpretation depends on what drove that channel and whether the movement persists.

Main Financial Account Components

The financial account is best read by component, not as one blended number. Each category records a different type of cross-border financing or financial exposure.

| Financial-account item | What it records | Market-pressure question | Main limitation |

|---|---|---|---|

| Direct investment | Cross-border investment linked to control or a significant degree of influence. | Is the flow linked to persistent capital commitment? | It may say little about immediate FX pressure or short-term market pricing. |

| Portfolio investment | Cross-border purchases and sales of securities such as equities and bonds. | Are flows responding to yields, risk appetite, benchmark allocation, or liquidity preference? | Portfolio flows may be more sensitive to rates, risk appetite, liquidity, and hedging costs than longer-control investment flows. |

| Other investment | Loans, deposits, trade credit, and other banking or financing flows. | Are cross-border funding conditions easing or tightening? | Banking flows need balance-sheet, maturity, and funding-context interpretation. |

| Financial derivatives and employee stock options | Cross-border derivative contracts, employee stock options where classified in the financial account, and related risk-transfer positions. | Is hedging demand or risk transfer changing? | Derivative exposure does not automatically equal spot capital movement. |

| Reserve assets | Official foreign reserve transactions by monetary authorities. | Are authorities absorbing FX pressure, adding buffers, or using reserves during stress? | Reserve changes need policy, FX regime, and external-balance context. |

How the Financial Account Connects to Capital Flows

The financial account is an accounting classification layer for many forms of cross-border flows. It does not convert those flows into one clean market message. It tells which financial channel is moving, then the market reading depends on why that channel is moving and whether the movement is persistent.

A portfolio inflow may reflect yield demand, benchmark allocation, short-term risk appetite, hedged exposure, or temporary positioning. A direct investment inflow may reflect a stronger capital commitment, but it may have limited short-term pricing impact. A banking outflow may reflect funding stress, balance-sheet adjustment, or normal loan repayment. The same financial-account direction can therefore produce different market-pressure readings.

Interpretation sequence: identify the component, separate asset and liability movement, check persistence, compare reserve behavior, then place the flow inside the current-account and liquidity backdrop.

Why Reserve Assets Change the Reading

Reserve assets make the financial account especially important for FX and external-balance interpretation. A change in reserves can reflect official activity rather than private investor behavior. That official activity may absorb pressure that would otherwise appear more clearly in the exchange rate or in private capital flows.

Reserve accumulation can indicate that authorities are buying foreign assets or building external buffers. Reserve drawdown can occur when authorities smooth currency pressure, meet external financing needs, or adjust policy operations. None of those readings is automatic. The same reserve movement can have different meaning under a fixed exchange-rate regime, a managed-float system, or a more flexible currency framework.

Why Financial Account Movement Is Not a Market Signal by Itself

A financial-account inflow does not automatically mean a currency should rise. An outflow does not automatically mean a currency should fall. The account records the financial side of cross-border transactions, but market pressure depends on timing, hedging, reserve behavior, investor type, external financing needs, and the broader liquidity environment.

Limitation: Financial-account data classifies flow channels. It does not provide a standalone forecast for currencies, yields, equity markets, policy decisions, or liquidity stress.

The most common mistake is treating the account as a directional indicator instead of a classification tool. A cleaner reading starts with the question: which flow category moved, who likely drove it, how persistent is it, and what pressure is visible in reserves, the current account, funding markets, and exchange-rate behavior?

Illustrative Financial Account Misread

A country can show financial-account inflows through portfolio investment while its currency remains under pressure. The inflow may be short-term, hedged, concentrated in one securities market, or offset by a weak current-account position. At the same time, reserve assets may be used to smooth FX stress. Under those conditions, “inflow equals currency strength” is too simple. The more useful reading is that the financial account identifies the financing channel that needs context from reserves, persistence, and external balance.

How to Read the Financial Account in Market Context

The financial account becomes more useful when it is paired with other external-balance and liquidity signals. Portfolio flows may matter more when they coincide with yield changes, credit-spread movement, or risk-appetite shifts. Banking flows may matter more when funding markets are strained. Reserve movements may matter more when exchange-rate pressure is visible and external financing needs are elevated.

The account is better read as a map of financial channels than as a forecast engine. It helps separate the type of pressure before interpreting whether that pressure is persistent, temporary, private-sector driven, official-sector driven, or mostly an accounting offset to another balance-of-payments item.

Related Concepts

Capital flows describe the broader movement of money between economies, asset classes, and financial systems. The financial account is one formal balance-of-payments classification used to organize part of that movement.

Cross-border flows focus on the direction and character of capital moving between residents and non-residents. That framing helps connect the financial account to market pressure without treating accounting entries as direct signals.