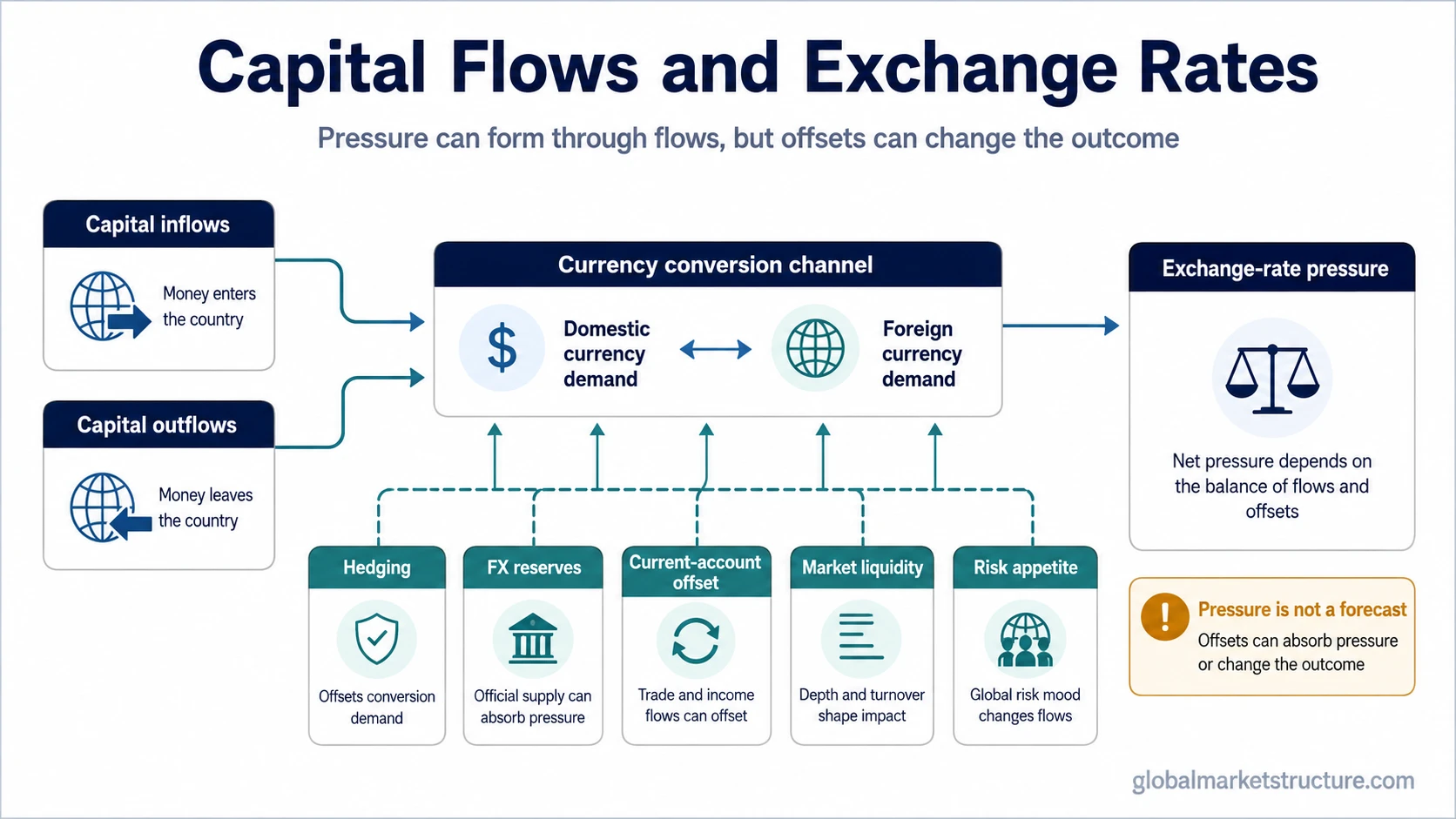

Capital flows can pressure exchange rates when cross-border buying, selling, lending, investing, or hedging changes demand for one currency relative to another. The effect is not automatic.

Flow persistence, hedging behavior, policy reaction, reserve use, current-account balances, market liquidity, and risk appetite can all change whether capital movement becomes visible currency pressure or is absorbed elsewhere.

Key Points

- Capital inflows can create demand for domestic currency, but the exchange-rate effect may be offset by hedging, policy action, or external deficits.

- Capital outflows can create pressure for foreign currency, but reserves, exporter FX sales, safe-haven demand, or liquidity conditions can soften the move.

- The useful reading is not “inflows equal strength” or “outflows equal weakness.” The useful reading is which pressure channel is active and what can absorb it.

- Flow type matters because foreign direct investment, portfolio flows, bank flows, official flows, and hedging flows can affect currencies differently.

Why Capital Flows Can Pressure Exchange Rates

Capital flows describe money moving between markets, economies, or currencies. When those flows cross currency borders, they can create buying demand for one currency and selling demand for another.

An inflow may require foreign investors to buy domestic currency before purchasing local bonds, equities, real estate, or other assets. An outflow may require domestic investors, banks, companies, or funds to sell domestic currency and acquire foreign currency. That conversion channel is the simplest link between cross-border flows and exchange-rate pressure.

The pressure is strongest when flows are large, persistent, and unhedged. A one-day portfolio adjustment is different from a multi-month shift in foreign demand for local assets. A fully hedged bond purchase is different from an unhedged equity inflow. A central-bank reserve operation is different from private capital moving because investors are changing risk exposure.

Exchange rates therefore respond not only to the direction of flow, but also to the kind of flow. Portfolio capital can move quickly and reverse suddenly. Foreign direct investment is usually slower and more durable. Bank funding flows can become important during stress. Official-sector flows may reflect reserve management or policy defense rather than private investor confidence.

Why Flow Direction Does Not Mechanically Determine FX

Flow direction alone is a weak currency forecast because exchange rates clear many forces at once. A country can receive capital inflows while its currency fails to strengthen if the inflow is hedged, if import demand creates offsetting foreign-currency demand, or if the central bank resists appreciation through reserve accumulation.

The reverse can also happen. Capital outflows may rise, but depreciation pressure can be softened if exporters sell foreign currency, reserves are used to smooth volatility, or global investors still treat the currency as a liquidity or safe-haven instrument. In that case, outflow pressure exists, but it is not the only force in the exchange-rate setting.

Policy reaction is one of the main offsets. Higher interest rates may attract capital, but they can also signal inflation stress, growth pressure, or a policy defense that investors do not fully trust. Reserve intervention may absorb pressure for a time, but it can also reveal that private demand is not strong enough on its own.

Market liquidity changes the visible effect. In deep FX markets, a large flow may be absorbed with limited price impact. In thinner markets, smaller flow imbalances may move the exchange rate more sharply. Liquidity conditions therefore decide how much price movement is needed to clear the same flow pressure.

Conditions That Change the Exchange-Rate Effect

| Condition | Possible exchange-rate pressure | Limitation |

|---|---|---|

| Persistent unhedged inflows | Can increase demand for domestic currency. | The effect can be reduced if the central bank accumulates reserves or if import demand offsets the flow. |

| Persistent unhedged outflows | Can increase demand for foreign currency. | Reserve use, exporter FX sales, or safe-haven demand can soften the visible move. |

| Hedged portfolio flows | May create weaker spot-currency pressure than headline flow data suggests. | The asset purchase and the currency hedge can point in different directions. |

| Policy defense or intervention | Can absorb some currency pressure for a period. | Intervention may not remove the underlying private-sector imbalance. |

| Current-account offset | Trade payments can offset capital-account pressure. | A country can receive capital inflows while still needing foreign currency for imports or external liabilities. |

| Risk appetite shift | Can amplify or reverse capital-flow pressure. | Global risk behavior may dominate local flow data during stress or relief phases. |

Common Mistake: Treating Flows as a Currency Forecast

The common mistake is treating capital-flow direction as a direct exchange-rate prediction. Inflows can create appreciation pressure, but they do not guarantee appreciation. Outflows can create depreciation pressure, but they do not guarantee depreciation.

A cleaner interpretation separates pressure from outcome. Capital flows can reveal who needs to buy or sell currency, how persistent that need may be, and whether the market is absorbing the pressure easily. The exchange-rate outcome still depends on hedging, policy, reserves, liquidity, trade flows, and global risk appetite.

The strongest reading usually comes from convergence. Flow pressure is more meaningful when it aligns with liquidity conditions, policy credibility, external balances, and broader risk behavior. The reading weakens when one large offset is visible, such as heavy hedging or official reserve activity.

Failure-Mode Example: Inflows Without Clear Currency Strength

A market attracts foreign capital because local yields have risen. Headline inflow data looks supportive for the domestic currency, but many investors hedge the currency exposure. At the same time, import demand keeps creating foreign-currency demand, and the central bank resists sharp appreciation by adding to reserves.

The sequence matters. The asset inflow creates one source of domestic-currency demand. The hedge reduces the spot FX effect. Import payments create foreign-currency demand. Reserve accumulation absorbs part of the remaining pressure.

The inflow still matters because it shows external demand for local assets. The currency response is muted because the spot FX pressure is partly offset before it becomes a clean exchange-rate move. The better reading is not that inflows failed. The better reading is that the flow channel was absorbed by hedging, external payments, and policy behavior.

Capital Flows, Cross-Border Flows, and FX Pass-Through

Capital flows are the broader category. They can include domestic and international movement across asset classes, institutions, sectors, and risk environments. This page focuses only on the part of that movement that can create currency demand or currency supply.

Cross-border flow analysis narrows the focus to capital moving between economies. That distinction matters because exchange-rate pressure usually appears when the flow crosses a currency boundary or changes hedging demand.

Currency movement can then transmit into prices, margins, import costs, external debt pressure, and inflation channels. That downstream link belongs to FX pass-through, where exchange-rate changes affect economic and market variables after the currency move has already occurred.

FAQ

Do capital inflows always strengthen a currency?

No. Capital inflows can support domestic-currency demand, but the effect can be reduced by hedging, current-account deficits, central-bank reserve accumulation, weak policy credibility, or broader risk conditions.

Can capital outflows pressure an exchange rate without causing a large depreciation?

Yes. Outflows can create foreign-currency demand, but reserves, exporter FX sales, safe-haven demand, and deep market liquidity can soften or delay the visible exchange-rate effect.

Which capital flows matter most for exchange rates?

The most relevant flows are usually large, persistent, and unhedged. Portfolio flows, bank funding flows, official-sector flows, and foreign direct investment can all matter, but they affect currencies through different channels.