A short squeeze is forced buying pressure that can appear when short sellers buy back borrowed shares as price rises against them. In market-structure terms, it is a positioning, leverage, borrow, margin, and liquidity feedback process, not a forecast, stock tip, or buy signal.

Short squeeze meaning: a short squeeze occurs when pressured short sellers cover their positions by buying shares back, and that buying demand can push price higher when liquidity is limited. The core mechanism is not high short interest by itself. It is the feedback loop between rising price, short-seller pressure, covering demand, and market liquidity.

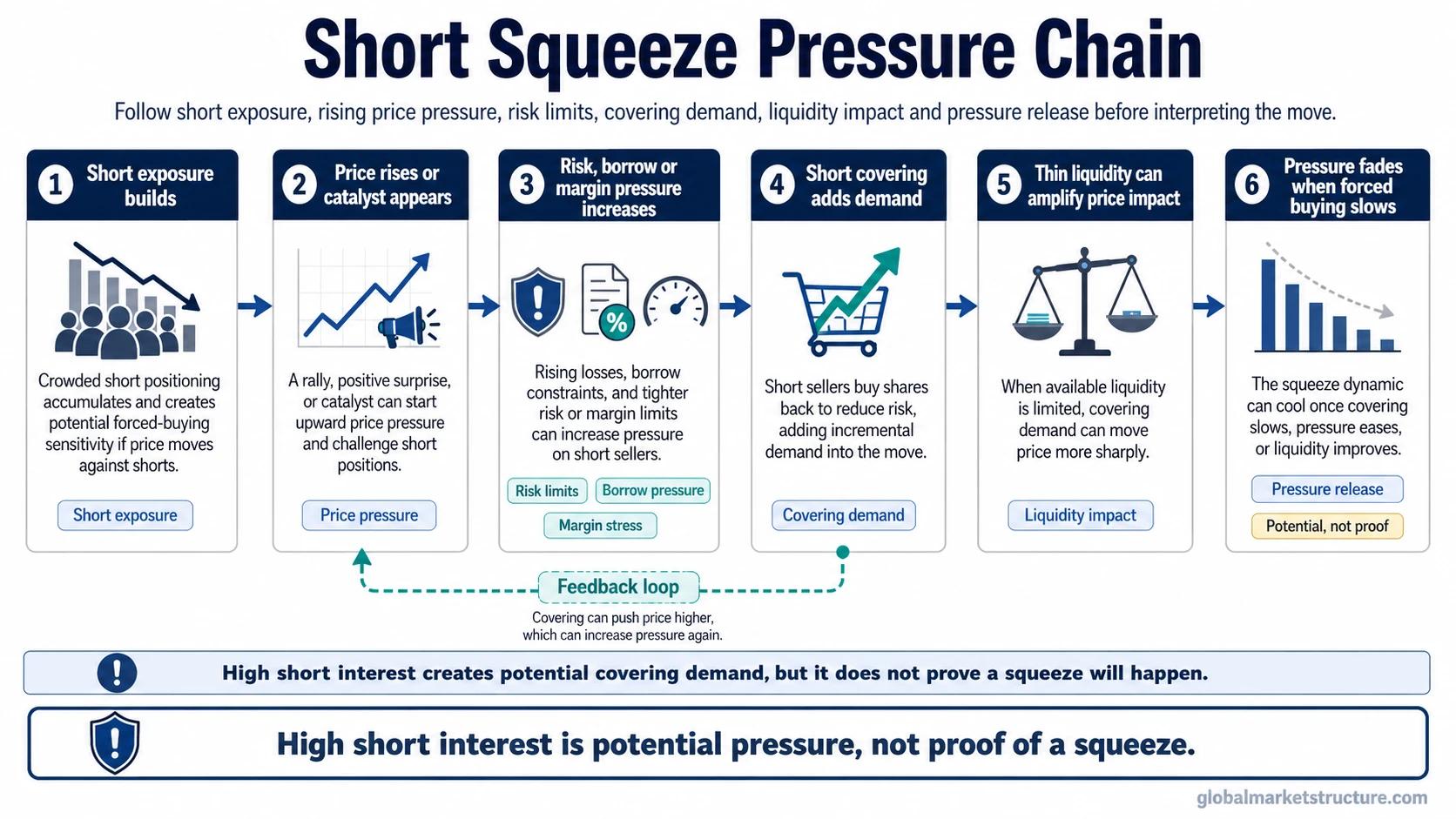

Short Squeeze in One Pressure Chain

- Short exposure exists: traders or funds have borrowed and sold shares, creating future buy-to-cover demand.

- Price rises or a catalyst appears: the move begins to pressure the short side through losses, risk limits, or changing expectations.

- Covering demand appears: short sellers buy shares back to reduce or close exposure.

- Liquidity can amplify the move: if available supply is thin, covering demand can move price faster than normal.

- Pressure eventually fades: once forced or crowded buying slows, the market must rely on normal demand, supply, and liquidity.

What Is a Short Squeeze?

A short squeeze is a market-pressure dynamic caused by short sellers buying back shares under stress. A short position begins when borrowed shares are sold. To close that position, the short seller must buy shares back. When price rises sharply, that future buying need can become urgent.

The squeeze is the feedback loop, not the short position alone. A stock can have high short interest without squeezing. The pressure becomes more important when short exposure meets a rising price, limited float, borrow stress, margin pressure, or thin liquidity.

That makes a short squeeze part of the broader forced-flow family. It is connected to positioning, financing pressure, risk limits, and liquidity feedback rather than to a simple bullish interpretation of the company or asset.

How a Short Squeeze Works

A short squeeze usually starts with meaningful short exposure and a price move that challenges the short thesis. The trigger can be news, a positioning imbalance, stronger buying demand, a liquidity gap, a change in borrow conditions, or a broader shift in risk appetite.

1. Short exposure builds. Market participants hold short positions that must eventually be reduced or closed by buying shares back.

2. Price moves against the short side. Losses rise as the price increases, and the position becomes more expensive or difficult to maintain.

3. Risk pressure increases. Short sellers may face internal risk limits, borrow-cost pressure, share recalls, collateral pressure, or margin stress.

4. Covering adds demand. Short sellers buy shares back, which can add demand into a rising market.

5. Feedback can intensify. Higher prices can pressure remaining shorts, creating more covering demand if liquidity is thin.

The feedback loop is strongest when covering demand arrives faster than the market can supply shares at stable prices. A large short position in a very liquid market may be absorbed with less disruption. A crowded short in a tighter float can create sharper price impact because each wave of covering competes for fewer available shares.

Conditions That Can Increase Short Squeeze Pressure

No single metric confirms a short squeeze. The pressure becomes more meaningful when several conditions point in the same direction: crowded short exposure, a rising price, constrained borrow, limited float, thin liquidity, and pressure on leveraged participants.

| Condition | What it can show | What it does not prove |

|---|---|---|

| High short interest | Many shares have been sold short, creating possible future buy-to-cover demand. | That a squeeze must occur. |

| High days to cover | Short exposure may be large relative to average trading volume. | That all covering will happen at once. |

| Rising borrow cost | Borrowed shares may be harder or more expensive to maintain. | That price must keep rising. |

| Limited float | Available shares may be scarce relative to potential covering demand. | That demand will overwhelm supply in every case. |

| Price momentum or catalyst | A trigger may be pressuring the short side. | That the move is sustainable after covering fades. |

| Thin liquidity | Covering orders can have larger price impact. | That the move is fundamentally justified. |

| Margin pressure | Leveraged short sellers may need to reduce exposure quickly. | That all short sellers will be forced out. |

Why High Short Interest Is Not Enough

High short interest is a condition, not a conclusion. It shows that possible future buying demand exists if short sellers need to cover. It does not show when they will cover, whether they are hedged, whether they can tolerate volatility, or whether new demand will be strong enough to start a feedback loop.

The main limitation: a short squeeze requires pressure, not only positioning. Short interest describes exposure. It does not prove urgency, forced buying, liquidity stress, or a future price path.

This is why squeeze metrics should be read as pressure conditions rather than predictions. The better question is not only whether short interest is high. The better question is what could force covering, whether borrow or margin pressure is rising, and whether the market has enough liquidity to absorb the buying.

Short Covering vs Short Squeeze

Short covering is the act of buying shares back to close or reduce a short position. A short squeeze is the broader pressure dynamic that can form when covering becomes urgent, crowded, or liquidity-sensitive.

| Concept | Meaning | Market-structure role |

|---|---|---|

| Short covering | Buying back shares to close or reduce a short position. | Creates demand from participants who were previously positioned for lower prices. |

| Short squeeze | A feedback loop where pressured covering helps push price higher. | Turns positioning pressure into forced or crowded buying pressure. |

All short squeezes involve covering pressure, but not all covering becomes a squeeze. Covering can be orderly when liquidity is deep, positioning is not crowded, and the price move does not trigger broader risk-control pressure.

Margin, Leverage, Borrow, and Liquidity Feedback

A short squeeze can become more intense when it intersects with financing stress. Short sellers using leverage may need to post more collateral as losses grow. If the position becomes too difficult to maintain, risk managers or brokers may require exposure reduction.

A margin call can add urgency because the short seller may need more equity or collateral to keep the position open. If that pressure cannot be managed, the position may be reduced quickly through buying.

This connects short squeezes to forced liquidation, although the direction is different from a forced sale in a long position. In a short squeeze, reducing exposure often means buying shares back.

The broader process also relates to deleveraging. When participants reduce financed exposure after stress, the market can experience flows driven less by long-term conviction and more by risk limits, financing pressure, and liquidity conditions.

Short Squeeze vs Gamma Squeeze and Long Squeeze

A short squeeze is driven by short sellers buying back shares. A gamma squeeze is usually connected to options hedging, where dealer exposure can require buying or selling the underlying asset as option sensitivity changes. The two can overlap in some situations, but they are different mechanisms.

A long squeeze is the opposite pressure direction. It can happen when leveraged long positions are forced to sell as price falls, risk limits tighten, or collateral pressure rises. The shared theme is forced exposure adjustment, but the direction of flow is different.

Short squeeze: pressured shorts buy back shares, adding upward demand.

Gamma squeeze: options hedging can create additional flow pressure as dealer exposure changes.

Long squeeze: pressured longs sell or reduce exposure, adding downward supply.

Common Misreadings

Misreading 1: high short interest means a squeeze is coming. It only shows potential covering demand.

Misreading 2: every fast rally in a heavily shorted stock is a short squeeze. A rally can also come from ordinary demand, news, revaluation, index flows, or broader risk appetite.

Misreading 3: squeeze metrics are trade signals. Short interest, days to cover, borrow cost, and float describe conditions, not guaranteed outcomes.

Misreading 4: a squeeze proves fundamental strength. A squeeze can be driven by positioning pressure even when the longer-term fundamental picture remains unresolved.

Misreading 5: the pressure lasts forever. Once forced buying slows, price depends on normal demand, supply, liquidity, and the broader market environment.

Related Forced-Flow Concepts

A short squeeze sits inside a wider forced-flow map. Short covering explains the closing action. Margin call explains collateral pressure. Forced liquidation explains exposure reduction under stress. Leverage explains why financed positions are sensitive to adverse movement. Deleveraging explains the broader reduction of exposure after pressure rises.

- Short covering: the buy-back action that closes or reduces a short position.

- Margin call: the collateral pressure that can force a position change.

- Forced liquidation: the process of reducing exposure under stress.

- Leverage: the financed exposure that can magnify sensitivity to price movement.

- Deleveraging: the broader reduction of exposure after risk pressure rises.

- Margin requirement: the equity or collateral threshold that can affect how much pressure a leveraged position can absorb.

- Margin debt: a broader measure of financed exposure that can matter for market-wide leverage context.

FAQ

What causes a short squeeze?

A short squeeze can be caused by a rising price, crowded short exposure, limited float, borrow stress, margin pressure, or a catalyst that forces short sellers to buy back shares. The squeeze forms when that covering demand becomes large enough to add further upward pressure.

Is high short interest enough to cause a short squeeze?

No. High short interest only shows potential covering demand. A squeeze also needs pressure that forces or motivates short sellers to cover, plus market conditions where that buying has meaningful price impact.

Is short covering the same as a short squeeze?

No. Short covering is the act of buying shares back to close or reduce a short position. A short squeeze is the feedback dynamic that can occur when covering becomes urgent, crowded, or liquidity-sensitive.

Is a short squeeze a buy signal?

No. A short squeeze is a pressure dynamic, not a buy signal. It can explain why price is moving quickly, but it does not prove that the move is sustainable or fundamentally justified.

How does liquidity affect a short squeeze?

Liquidity affects how much price impact covering demand can have. When available supply is thin, the same amount of buying can move price more sharply. When liquidity is deep, covering may be absorbed with less dramatic movement.