Forced liquidation means the involuntary closing, sale, or reduction of leveraged exposure when margin, collateral, or risk requirements are breached. It is a forced-flow mechanism: private account stress can turn into public market pressure, but it is not automatically a crash signal, forecast, or trading instruction.

Definition: forced liquidation occurs when a broker, exchange, clearing process, lender, or risk system reduces exposure because the position no longer has enough support to remain open under the required rules.

- Forced liquidation starts from leverage, margin, collateral, or risk-limit pressure.

- The forced flow can be selling or buying, depending on whether the exposure being closed is long or short.

- A margin call is usually a warning, demand, or deficiency notice; forced liquidation is the enforcement stage.

- Market impact becomes more important when liquidations are clustered and liquidity is thin.

What forced liquidation means in market structure

Forced liquidation sits at the intersection of leverage, collateral, margin rules, and forced flows. The important market-structure point is that the decision to reduce exposure may no longer be voluntary. Once the required support fails, the position can be closed, reduced, or sold to bring risk back inside the allowed boundary.

That makes forced liquidation different from ordinary selling, voluntary deleveraging, or portfolio rebalancing. The flow is not mainly caused by a discretionary view on value. It is caused by a constraint: collateral is insufficient, margin support has weakened, a risk rule has been breached, or the position can no longer remain open under the relevant process.

| Concept | Meaning | Forced liquidation boundary |

|---|---|---|

| Leverage | Exposure is larger than the capital directly supporting it. | Creates the condition where collateral or margin pressure can force exposure reduction. |

| Margin debt | Borrowed money or financed exposure used to hold market positions. | Can increase sensitivity to price moves, collateral pressure, and forced reduction. |

| Margin call | A warning, demand, or deficiency notice that support must be restored. | May come before liquidation, but it is not the same as forced liquidation. |

| Forced liquidation | Involuntary closing, sale, or reduction of exposure. | The enforcement stage when the position is reduced because support is no longer sufficient. |

| Liquidation cascade | Clustered liquidations that can reinforce pressure across positions. | A possible clustered outcome, not the definition of forced liquidation itself. |

| Forced liquidation value | An asset valuation term often used in appraisal or distressed sale contexts. | A different meaning from market-position forced liquidation. |

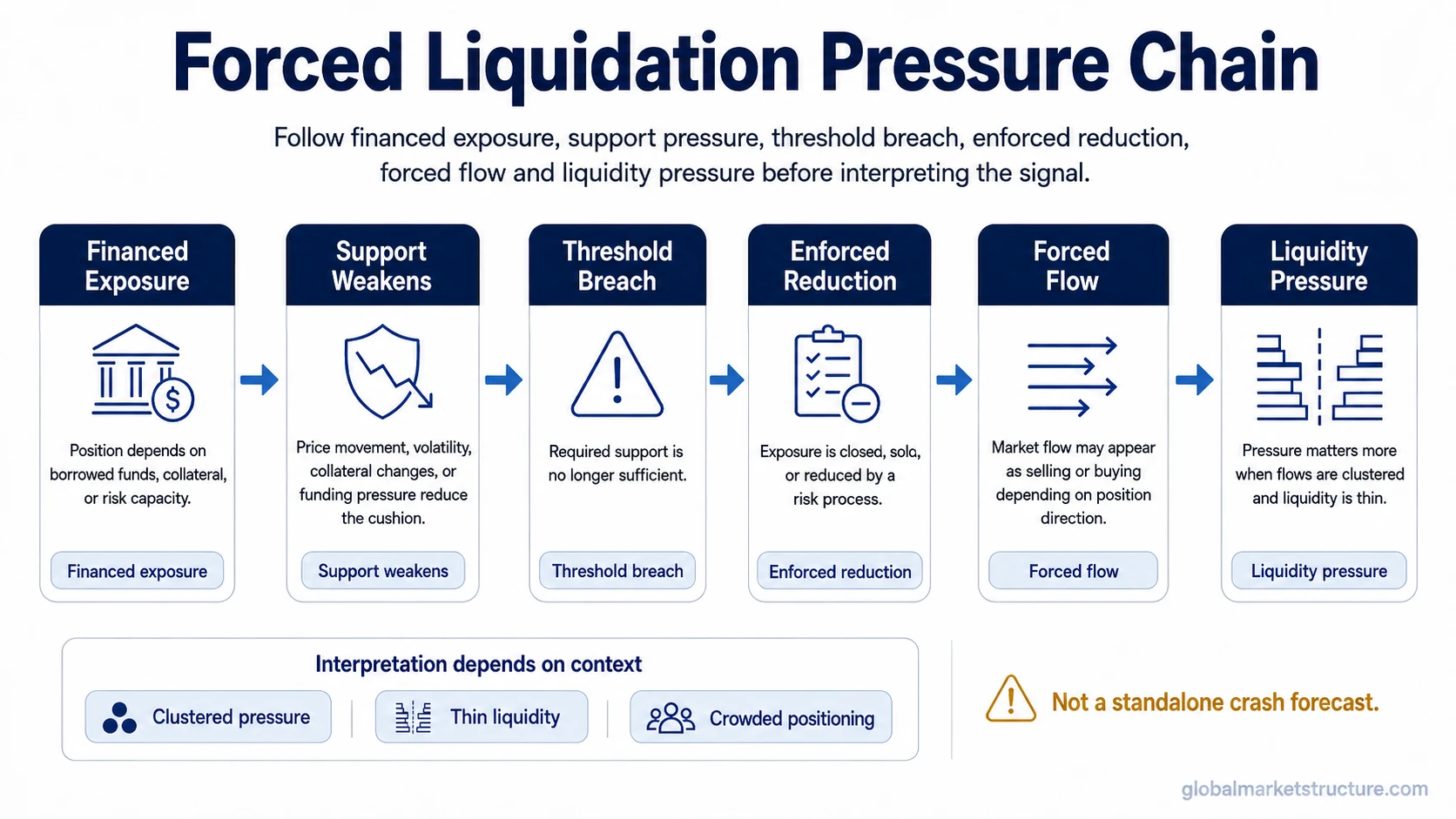

How forced liquidation works

The mechanism follows a pressure chain: leveraged exposure loses support, a threshold is breached, reduction is enforced, and the resulting flow reaches the market. The impact depends on whether the pressure is isolated or clustered across similar positions.

- Leveraged exposure exists: a position depends on borrowed funds, margin, collateral, or risk capacity.

- Support weakens: price movement, volatility, collateral changes, or funding pressure reduces the cushion behind the position.

- A threshold is breached: the position no longer meets margin, collateral, or risk requirements.

- Reduction is enforced: a broker, exchange, lender, clearing process, or risk system closes or reduces exposure.

- Market flow appears: the forced action reaches the market as selling, buying, or a reduction in liquidity-taking exposure.

The key distinction is that the final flow is constrained. The position is not being reduced only because the holder changed their opinion. It is being reduced because the position can no longer be supported under the applicable margin, collateral, or risk framework.

Forced liquidation vs margin call

A margin call and a forced liquidation are related, but they are not identical. A margin call usually signals that additional capital, collateral, or position reduction is needed. Forced liquidation is the point where exposure is reduced involuntarily because the requirement has not been met, cannot be met, or is enforced by the applicable risk process.

| Question | Margin call | Forced liquidation |

|---|---|---|

| What is happening? | A deficiency is identified and support is requested or required. | Exposure is closed, sold, or reduced without relying on a voluntary decision. |

| Is there still a chance to restore support? | Often yes, depending on the rule set and timing. | Usually no for the portion being liquidated. |

| What reaches the market? | Not necessarily a market order by itself. | A forced flow may reach the market through selling or buying. |

| Main interpretation risk | Assuming every warning becomes liquidation. | Assuming every forced liquidation becomes a crash signal. |

Forced selling, forced buying, and position direction

Forced liquidation is often described as forced selling, but that is only one side of the mechanism. If a leveraged long position is liquidated, the flow can appear as selling pressure. If a leveraged short position is liquidated, the position may need to be bought back, which can create forced buying pressure.

This is why position direction matters. Forced closure of shorts can overlap with short-covering, while forced closure of longs can add supply to the market. In both cases, the common feature is not the direction of the trade. The common feature is involuntary exposure reduction.

Why forced liquidation can matter for market pressure

Forced liquidation becomes more important when many positions share similar leverage, collateral, funding, or volatility exposure. A single account liquidation may have little broader meaning. Clustered liquidations can matter because private stress becomes public flow: positions are reduced, orders reach the market, liquidity is consumed, and other participants may react to the pressure.

The market-structure reading is strongest when forced liquidation appears alongside thinner liquidity, crowded positioning, rising volatility, collateral pressure, or funding stress. Under those conditions, forced flows can transmit pressure beyond the original account or venue. Without clustering or liquidity stress, forced liquidation may remain a contained account-level event.

What forced liquidation is not

Not a crash signal by itself: forced liquidation can add pressure, but it does not automatically mean a market crash is coming.

Not always forced selling: long liquidation can create selling, while short liquidation can require buying.

Not always preceded by a manual margin call: depending on the venue, account, or risk framework, some processes may move quickly from deficiency to enforced reduction.

Not a broker tutorial: platform-specific margin rules, liquidation prices, and account procedures vary and should not be generalized across markets.

Not forced liquidation value: valuation or appraisal usage is a separate meaning from leveraged market-position liquidation.

A practical forced liquidation scenario

A common scenario is that a group of leveraged participants holds similar long exposure while liquidity is already thin. If prices fall and collateral support weakens, some accounts may breach margin or risk thresholds. Forced reductions then add sell orders into a weaker market. If other leveraged holders face the same pressure, the flow can become clustered and may amplify short-term market stress.

The same logic can work in the opposite direction. If crowded short exposure is forced to close, the required action may be buying rather than selling. The broader lesson is that forced liquidation should be read through exposure direction, leverage, liquidity, and clustering, not through the word liquidation alone.

How to interpret forced liquidation without overreading it

Forced liquidation is useful as a market-structure concept because it shows when exposure reduction is no longer fully discretionary. It helps explain how leverage can turn losses, collateral pressure, or margin stress into visible market flow.

The interpretation remains conditional. The signal becomes more meaningful when forced liquidation is clustered, liquidity is thin, positioning is crowded, and related markets show stress. It becomes weaker when the event is isolated, liquidity is deep, and there is no broader evidence of forced-flow transmission.

Related concepts

Nearby concepts become clearer when each one is placed in the pressure chain. Leverage creates exposure sensitivity. Margin debt reflects financed exposure. A margin call signals a support problem. Deleveraging describes the broader reduction of exposure. Forced liquidation is the involuntary enforcement point where exposure is closed, sold, or reduced.

FAQ

Is forced liquidation the same as a margin call?

No. A margin call usually signals that more capital, collateral, or position reduction is needed. Forced liquidation is the enforcement stage where exposure is reduced involuntarily.

Can forced liquidation cause buying instead of selling?

Yes. Liquidation of long exposure can create selling pressure, while liquidation of short exposure can require buying to close the short position.

Is forced liquidation value the same thing?

No. Forced liquidation value usually refers to an asset valuation or appraisal context. Forced liquidation in market structure refers to involuntary reduction of leveraged market exposure.

Does forced liquidation mean a crash is coming?

No. Forced liquidation can add pressure when clustered and when liquidity is thin, but it is not a standalone crash forecast or trading signal.