Margin debt is borrowed money used to purchase or hold securities in margin accounts. At the aggregate market level, it can help show how much financed exposure exists in the system, but it is not a standalone crash forecast, timing signal, or instruction to buy or sell.

Simple definition: margin debt is the outstanding borrowed exposure tied to securities held on margin.

Market-structure meaning: aggregate margin debt can reflect the scale of leveraged participation, positioning confidence, and potential sensitivity to falling prices or collateral pressure.

Key limitation: the number does not prove future market direction. Its meaning depends on trend, liquidity, volatility, collateral pressure, funding conditions, and how concentrated the exposure is.

Key Points About Margin Debt

- Margin debt measures borrowed securities exposure, not total market leverage.

- Rising margin debt can reflect confidence, speculation, crowding, or easier financing conditions.

- Falling prices can make margin debt more fragile when collateral support weakens.

- Margin calls and forced liquidation can turn borrowed exposure into forced selling pressure.

- Margin debt needs context. It should be read with liquidity, volatility, market size, funding conditions, and positioning concentration.

What Margin Debt Shows

Margin debt shows the amount of securities exposure financed with borrowed money through margin accounts. For a single account, it describes borrowing against securities. For market interpretation, the aggregate figure is more useful because it can show how much financed exposure is present across a broader group of participants.

The aggregate number is best treated as an observed data point. It can describe the presence of borrowed exposure, but interpretation starts only after context is added. A high level may look different in a large, liquid, rising market than it does in a thin market with falling prices, rising volatility, and weakening collateral support.

That distinction matters because margin debt is not the same as leverage as a broad concept. Margin debt is one measured form of financed securities exposure. Leverage can also appear through derivatives, balance sheets, structured products, fund financing, and other forms of borrowed or synthetic exposure.

Why Margin Debt Matters for Market Structure

Margin debt matters because borrowed exposure can become sensitive when prices move against the collateral supporting that exposure. If asset prices rise and liquidity is deep, financed exposure may be easy to maintain. If prices fall and liquidity weakens, the same exposure can become harder to support.

The market-structure risk is not the existence of margin debt by itself. The risk is the pressure chain that can appear when financed exposure, falling prices, collateral requirements, volatility, and liquidity conditions interact. Under those conditions, participants may have less choice about when they reduce exposure.

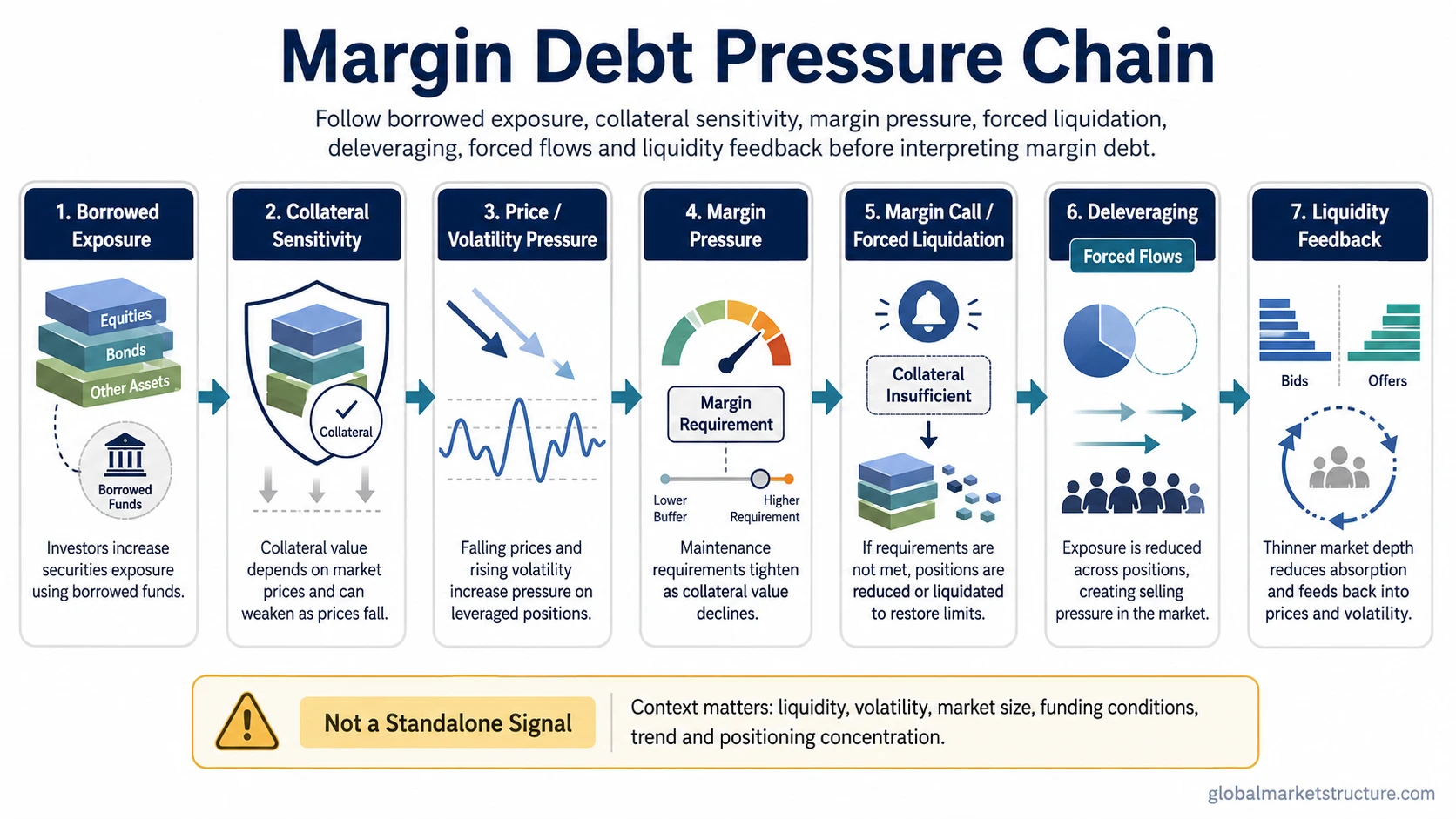

Margin debt pressure chain:

Borrowed exposure → collateral sensitivity → margin pressure → margin calls or forced liquidation → deleveraging → forced flows → liquidity feedback.

A margin call is not the same as margin debt. Margin debt is the outstanding borrowed exposure. A margin call is a demand for more collateral or reduced exposure when account equity becomes insufficient under the applicable margin rules.

How Margin Debt Can Turn Into Forced Flow Pressure

Margin debt becomes more important when the market stops treating borrowed exposure as stable. A decline in asset prices can reduce collateral value. Lower collateral value can increase margin pressure. If the participant cannot add collateral or reduce risk voluntarily, exposure may need to be cut.

That is where forced liquidation enters the mechanism. Forced liquidation is an involuntary reduction of exposure. It can add selling pressure because the trade is driven by collateral and risk constraints rather than by a fresh discretionary market view.

If many participants face similar pressure at the same time, the process can contribute to deleveraging. Deleveraging is the broader reduction of debt-funded or financed exposure. Margin debt is one channel through which that process can appear, not the whole process itself.

Illustrative scenario: a market can show high aggregate margin debt while prices are rising and liquidity is still strong. That condition alone does not prove fragility. The reading changes if prices begin falling, volatility rises, collateral values weaken, and liquidity becomes thin. In that environment, some financed exposure may need to be reduced at the same time, which can create pressure beyond the original price move.

How to Interpret Margin Debt Data

Margin debt data is most useful when separated into three layers: what is observed, what the observation may suggest, and what the observation does not prove. This prevents the common mistake of treating the data as a mechanical market signal.

| Reading layer | What it can show | What it does not prove | Context that changes the interpretation |

|---|---|---|---|

| Raw level | The amount of borrowed securities exposure reported in aggregate. | It does not prove whether the market is overvalued, safe, or near a turning point. | Market size, asset-price level, reporting date, and comparison method. |

| Rising margin debt | More financed exposure may be entering or remaining in the market. | It does not automatically mean markets are bearish or unstable. | Liquidity conditions, trend strength, volatility, breadth, and risk appetite. |

| High margin debt | There may be more exposure that could become sensitive to collateral pressure. | It does not guarantee a crash or forced selling event. | Positioning concentration, funding conditions, collateral quality, and depth of market liquidity. |

| Falling margin debt | Borrowed exposure may be shrinking, either voluntarily or under pressure. | It does not automatically mean risk has cleared or markets are bullish. | Whether the decline reflects orderly risk reduction, forced deleveraging, or a broader liquidity shock. |

Source note: Current aggregate margin debt levels should be checked against the latest dated margin-statistics release from FINRA or another reliable data endpoint before using the number in a market reading. Without date-specific verification, the safer interpretation is the mechanism: borrowed exposure, collateral pressure, forced flows, and liquidity conditions.

Common Misreads of Margin Debt

The most common misread is treating margin debt as a direct forecast. High margin debt can increase vulnerability when it combines with falling prices, thin liquidity, collateral pressure, and crowded positioning. Without those surrounding conditions, the same data can simply describe financed participation in a market that still has enough liquidity to absorb risk.

Margin debt is not a crash signal. It can help identify where borrowed exposure exists, but the pressure depends on what happens next to collateral, volatility, financing conditions, and market liquidity.

Another misread is assuming that rising margin debt is always negative. Rising margin debt can reflect confidence, speculative appetite, easier financing, or broader participation. It becomes more fragile when the exposure is crowded, collateral values weaken, and exit liquidity is poor.

A third misread is assuming that aggregate margin debt explains the whole leverage picture. It does not capture derivative exposure, institutional leverage, synthetic positioning, or forced buying dynamics such as a short squeeze. It is one useful lens inside a wider leverage and liquidity framework.

Margin Debt vs Related Concepts

Margin debt sits near several related concepts, but each one answers a different question. Keeping those boundaries clear prevents one reported number from being mistaken for a full market forecast.

| Concept | What it means | How it relates to margin debt |

|---|---|---|

| Leverage | Broad use of borrowed or synthetic exposure to increase market sensitivity. | Margin debt is one measured form of leverage, not the whole leverage system. |

| Margin call | A collateral demand event when account equity is insufficient under margin rules. | Margin debt can become vulnerable to margin calls when collateral support weakens. |

| Forced liquidation | Involuntary exposure reduction driven by constraints rather than choice. | Margin debt can contribute to forced liquidation if collateral cannot support the borrowed exposure. |

| Deleveraging | Reduction of debt-funded or financed exposure across participants. | Margin debt can be one channel through which deleveraging pressure appears. |

| Short squeeze | Forced buying pressure from short-position stress. | It is a related forced-flow concept, but the direction and mechanics differ from margin-debt selling pressure. |

| Margin requirement | The rule or threshold that defines how much collateral must support margin exposure. | It helps determine when margin debt becomes harder to maintain, but it is not the debt itself. |

A margin requirement deals with the collateral threshold that supports margin exposure, while margin debt describes the borrowed exposure already outstanding.

Where Margin Debt Fits in a Market-Structure Reading

Margin debt is most useful as a context indicator inside a broader market-structure reading. It helps describe financed exposure, but it should be interpreted alongside liquidity, volatility, trend quality, breadth, funding conditions, and collateral pressure.

A stronger reading usually requires alignment across several conditions. Borrowed exposure matters more when market liquidity is thin, volatility is rising, collateral values are falling, and participants are crowded on the same side of the risk trade. It matters less as a standalone number when those pressure conditions are absent.

The cleanest use is therefore conditional: margin debt can identify exposure that may become sensitive, while the surrounding market structure shows whether that exposure is likely to remain stable or become a source of forced-flow pressure.

FAQ

Is margin debt a crash signal?

No. Margin debt can show financed exposure and potential vulnerability, but it does not predict a crash by itself. The interpretation depends on liquidity, volatility, collateral pressure, funding conditions, market trend, and positioning concentration.

Is margin debt the same as leverage?

No. Margin debt is one measured form of borrowed securities exposure. Leverage is broader and can include other forms of debt-funded, derivative, balance-sheet, or synthetic exposure.

How can margin debt lead to forced selling?

Margin debt can lead to forced selling when falling prices reduce collateral value and the borrower cannot add collateral or reduce risk voluntarily. Under those conditions, exposure may need to be liquidated to meet margin requirements.

Should current margin debt levels be included in a market reading?

Current levels can be useful only when they are checked against a reliable data source and dated clearly. Without date-specific verification, the safer approach is to explain the mechanism and avoid current record-level claims.