Deleveraging is the reduction of debt, leverage, or borrowed exposure. In market-structure terms, it matters when that reduction changes positioning, asset sales, funding demand, liquidity pressure, or risk appetite.

It describes the reduction process, not leverage itself, and not every forced sale is automatically a full deleveraging cycle.

Definition: Deleveraging means reducing borrowed exposure. That reduction can happen through debt repayment, lower borrowing, asset sales, refinancing, restructuring, write-offs, or forced exposure cuts when funding or collateral conditions become tighter.

Deleveraging does not by itself mean a crisis, a market forecast, or a one-way rule for asset prices. The same process can be orderly when balance sheets are repaired gradually, or disorderly when many leveraged participants need liquidity at the same time.

Key Points

- Deleveraging means reducing debt, leverage, or borrowed exposure.

- Market stress can rise when deleveraging requires asset sales, lower risk exposure, or urgent liquidity.

- Forced deleveraging is narrower than deleveraging itself because voluntary balance-sheet repair can also reduce leverage.

- Margin pressure, collateral values, funding costs, and market depth shape whether deleveraging stays orderly or becomes disorderly.

- Deleveraging is best read as a transmission process, not as a standalone market-timing rule.

What Deleveraging Means

Deleveraging starts with an existing financed position, debt load, or balance-sheet exposure. A company may reduce debt, a household may pay down liabilities, a bank may shrink assets, or a market participant may reduce borrowed exposure.

For market-structure interpretation, the most relevant form is market-positioning deleveraging. The focus is not only whether debt falls on paper, but whether exposure reduction changes liquidity demand, capital flows, crowding, volatility, or cross-asset risk appetite.

Deleveraging becomes more important for market interpretation when the reduction is not isolated. A single participant lowering risk may have little visible market effect. Many participants reducing exposure at the same time can create persistent selling pressure, weaker liquidity, and broader risk reduction.

What Deleveraging Is Not

Several nearby concepts overlap with deleveraging, but they do not mean the same thing. The boundary matters because a balance-sheet repair process, a funding shock, and a forced liquidation can produce different market behavior.

| Concept | Relationship to deleveraging | Boundary |

|---|---|---|

| Leverage | The starting condition: borrowed or financed exposure exists before it can be reduced. | Leverage describes exposure expansion or financing. Deleveraging describes exposure reduction. |

| Forced selling | One possible channel when assets must be sold to reduce exposure or raise cash. | Not all deleveraging requires forced selling. |

| Margin call | A collateral demand that can force exposure reduction if cash or collateral is insufficient. | A margin call can trigger deleveraging, but it is not the whole process. |

| Liquidity spiral | A possible feedback loop when selling pressure weakens prices and liquidity, forcing more reduction. | A liquidity spiral is a broader feedback condition, not every deleveraging episode. |

| Debt cycle or credit cycle | A broader macro framework that can include leverage buildup and later reduction. | Deleveraging is one phase or mechanism inside a wider cycle, not the entire cycle. |

Main Types of Deleveraging

Deleveraging can occur at several levels. The level matters because the market effect is different when one company reduces debt compared with a system-wide reduction in risk exposure.

| Type | What is reduced | Market-structure relevance |

|---|---|---|

| Corporate deleveraging | Company debt, liabilities, or balance-sheet leverage. | Can affect investment, buybacks, credit quality, refinancing needs, and risk appetite toward corporate debt. |

| Household deleveraging | Consumer debt or household balance-sheet leverage. | Can influence consumption, credit demand, and macro growth sensitivity. |

| Financial-system deleveraging | Bank, dealer, fund, or institutional balance-sheet exposure. | Can affect market depth, credit availability, collateral demand, and asset-price transmission. |

| Macro deleveraging | Sector-level or economy-wide debt relative to income, output, or asset values. | Can shape growth, policy sensitivity, capital flows, and risk-environment interpretation. |

| Market-positioning deleveraging | Borrowed exposure in portfolios, funds, carry trades, or crowded market positions. | Can produce positioning unwind, asset sales, volatility, and cross-asset pressure when liquidity is thin. |

How Deleveraging Works in Market Structure

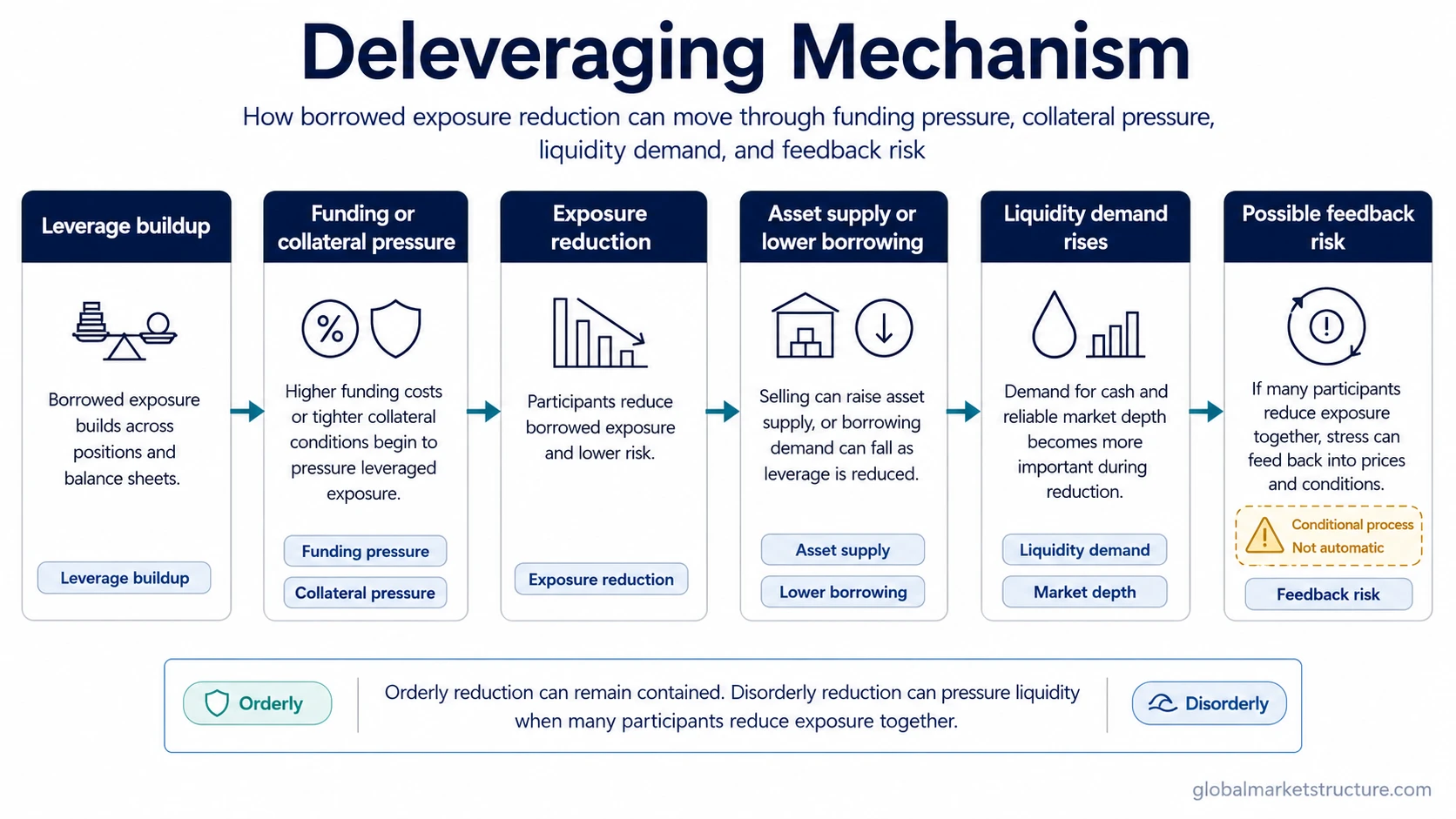

Deleveraging usually becomes visible after a period of leverage buildup. Borrowed exposure expands risk capacity while financing is available, collateral values are stable, and volatility is manageable.

Mechanism sequence:

- Borrowed exposure builds through debt, margin, repo, derivatives, structured financing, or portfolio leverage.

- A pressure point appears, such as higher funding cost, weaker collateral value, wider spreads, lower liquidity, or rising volatility.

- Participants reduce exposure through repayment, refinancing, lower borrowing, hedging, or asset sales.

- Liquidity demand rises because cash, collateral, and balance-sheet room become more valuable.

- If many participants reduce exposure together, selling pressure and weaker market depth can reinforce each other.

The mechanism is conditional. Deleveraging can be gradual when financing remains available and buyers absorb supply. It becomes more unstable when reduced market depth, crowded positioning, and collateral pressure appear at the same time.

Forced Deleveraging, Margin Pressure, and Liquidity Stress

Forced deleveraging occurs when exposure is reduced because funding, collateral, or risk limits no longer support the position. A margin call is one way that pressure can become immediate: more cash or collateral is required, and exposure may need to fall if the requirement cannot be met comfortably.

Forced reduction can make liquidity stress more visible because the participant is not simply choosing to become more conservative. The participant may need cash quickly, and that urgency can lead to sales into weaker market depth.

Important limitation: Margin pressure can intensify deleveraging, but deleveraging is broader than margin pressure. Debt repayment, refinancing, reduced borrowing, and voluntary exposure cuts can all reduce leverage without an immediate collateral call.

Why Deleveraging Can Affect Capital Flows and Positioning

Deleveraging can affect capital flows because exposure reduction changes where capital is held, what needs to be sold, and which assets remain liquid enough to absorb pressure. When many participants hold similar risk exposures, the same reduction process can become a crowding reversal.

The effect is not limited to one asset class. A funding squeeze in one area can lead participants to sell liquid assets elsewhere, reduce carry exposure, cut equity risk, hold more cash, or pull back from credit-sensitive positions. The cross-asset effect depends on financing structure, collateral quality, market depth, and the degree of crowding.

Risk appetite can weaken during deleveraging because participants prioritize balance-sheet repair over return-seeking exposure. That does not mean all risky assets must fall. It means liquidity preference and exposure discipline can become more important than the original investment thesis.

Simple Deleveraging Scenario

A leveraged participant holds several risk positions financed with borrowed money. Funding costs rise while collateral values weaken. The participant reduces exposure to lower financing needs and protect available liquidity.

The first sales may be manageable if market depth is strong and other buyers absorb the supply. The same reduction can become more disruptive if several similar participants hold crowded positions, funding terms tighten at the same time, and buyers demand a larger discount to provide liquidity.

The market-structure reading is not that deleveraging guarantees a crash. The diagnostic issue is whether exposure reduction remains isolated and orderly, or whether it starts linking funding pressure, collateral pressure, asset sales, and weaker liquidity into one feedback loop.

Common False Readings and Limitations

- False reading 1: Treating deleveraging as automatically bearish. Exposure reduction can weigh on risk appetite, but the market effect depends on liquidity depth, policy environment, buyer demand, and whether the process is broad or isolated.

- False reading 2: Treating every debt reduction as distress. Some deleveraging is planned balance-sheet repair and can reduce fragility over time.

- False reading 3: Treating forced selling and deleveraging as identical. Forced selling can be one channel, but deleveraging also includes repayment, refinancing, lower borrowing, restructuring, or voluntary risk reduction.

- False reading 4: Treating deleveraging as proof that systemic risk is active. Systemic risk requires broader evidence across funding markets, collateral behavior, credit conditions, volatility, and cross-asset liquidity.

Deleveraging as a Market-Structure Process

The most useful interpretation separates balance-sheet action from market transmission. The action is exposure reduction. The transmission depends on how that reduction affects cash demand, asset supply, funding conditions, collateral values, and the ability of markets to absorb sales without large price impact.

Orderly deleveraging can reduce future fragility. Disorderly deleveraging can create a feedback loop when lower prices reduce collateral values, weaker collateral forces more exposure reduction, and lower liquidity makes each sale more disruptive.

The practical distinction is conditional rather than predictive: deleveraging deserves closer attention when it appears with rising funding stress, weaker market depth, crowded positioning, collateral pressure, and cross-asset risk reduction.

Related Market Structure Concepts

Leverage explains the starting exposure that deleveraging later reduces. Margin call explains one specific collateral mechanism that can force faster exposure reduction. Forced selling, forced liquidation, liquidity spiral, debt cycle, and credit cycle are adjacent ideas that should remain separate unless the evidence shows that the reduction process has become broader and self-reinforcing.

FAQ

What is deleveraging in simple terms?

Deleveraging means reducing debt, leverage, or borrowed exposure. In markets, it matters when that reduction affects asset sales, funding demand, liquidity, positioning, or risk appetite.

Is deleveraging always bad for markets?

No. Deleveraging can be orderly when exposure is reduced gradually and liquidity remains available. It becomes more risky when many participants reduce exposure at the same time into weak market depth.

Is deleveraging the same as a margin call?

No. A margin call can force deleveraging, but deleveraging is broader. It can also happen through repayment, refinancing, reduced borrowing, asset sales, restructuring, or voluntary risk reduction.

How does deleveraging affect liquidity?

Deleveraging can increase demand for cash and reduce risk-taking capacity. If asset sales occur into thin markets, liquidity pressure can rise and price impact can become larger.