A margin call is a demand to restore required equity or collateral after a leveraged account falls below a margin or maintenance threshold. It can happen when the value of financed assets declines, when a short position moves against the borrower, or when margin requirements rise. A margin call is not the same as forced liquidation, but an unresolved shortfall can lead to exposure reduction or liquidation depending on the rules of the broker, lender, product, and jurisdiction.

Direct answer: a margin call is a collateral or equity shortfall event. It tells the borrower that the account no longer satisfies the required margin condition.

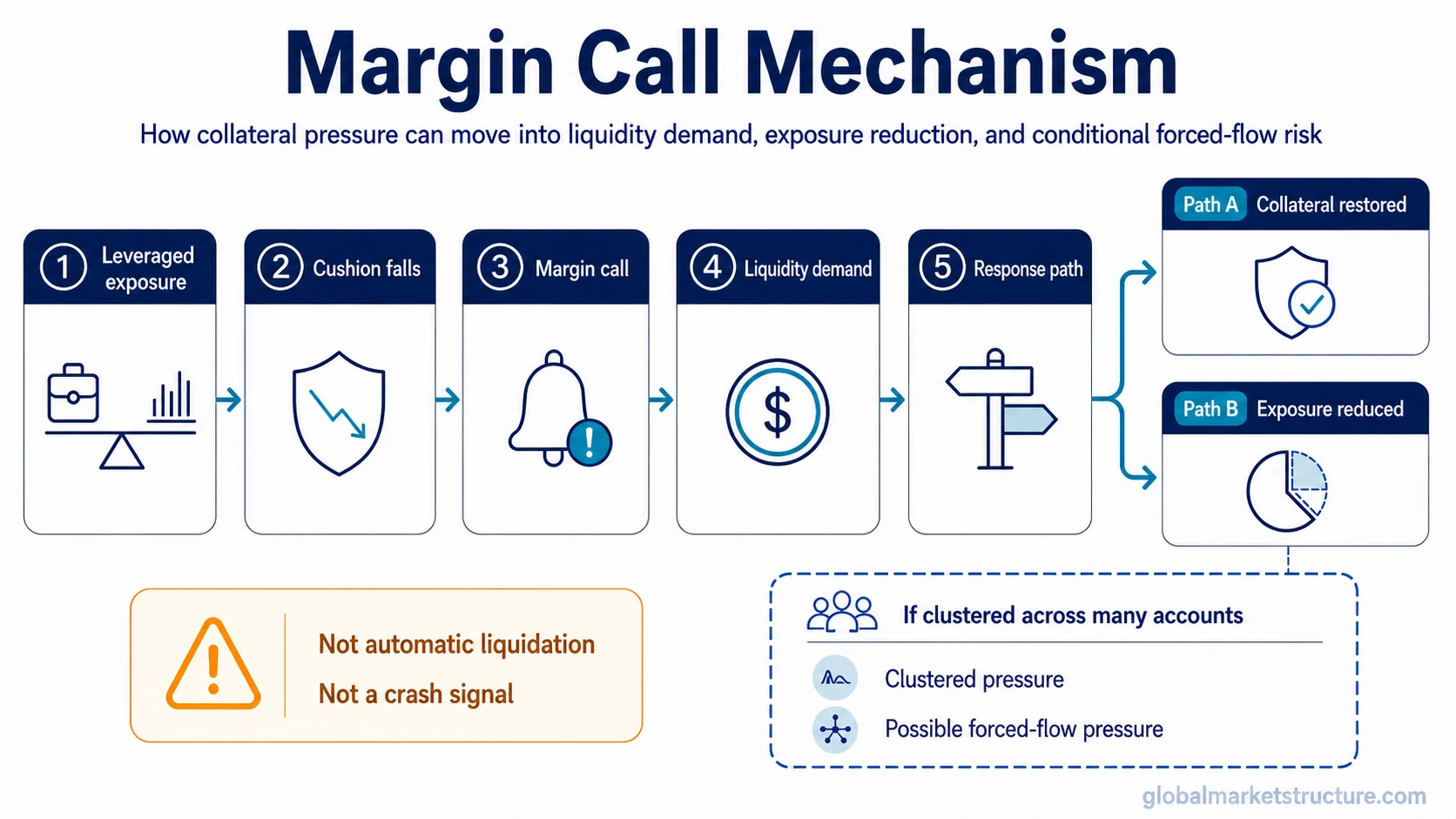

Mechanism: leveraged exposure creates a required equity level. If account equity falls below that level, the margin call appears as a demand to restore the shortfall.

Boundary: the call itself is not a market crash signal, not a sell signal, and not automatically forced liquidation.

Market-structure relevance: when similar collateral pressure appears across many leveraged accounts, price movement can turn into liquidity demand and possible exposure reduction.

Key Points

- A margin call is triggered by insufficient equity or collateral relative to a required threshold.

- The threshold is set by margin rules that can vary by broker, lender, asset class, product, and jurisdiction.

- The call may be resolved before liquidation, so the call and the liquidation are separate events.

- Market impact depends on scale, concentration, liquidity conditions, and whether many participants need cash or exposure reduction at the same time.

How a Margin Call Happens

A margin call begins with borrowed exposure. The account holds assets, positions, or collateral while using financing from a broker or lender. That financing creates a required equity buffer. If the buffer becomes too small, the account no longer satisfies the required margin condition.

Basic sequence: leveraged exposure → asset value decline, adverse short-position move, or higher requirement → equity or collateral shortfall → margin call → possible collateral restoration, exposure reduction, or liquidation if the shortfall remains unresolved.

The trigger is not limited to a falling long position. A short position can also create margin pressure if the borrowed asset rises in price and the account needs more equity to support the exposure. Provider, exchange, or product rules may also be adjusted when risk conditions change. Those details are rule-dependent, so a general definition should not be treated as a universal account procedure.

Margin Call vs Margin Requirement, Margin Debt, Forced Liquidation, and Deleveraging

Several nearby terms are often used together, but they describe different parts of the leverage structure. Keeping them separate prevents the margin call from being misread as the whole process.

| Term | What it means | Role in the process |

|---|---|---|

| Margin call | An event or demand created by an equity or collateral shortfall. | Signals that the account no longer satisfies the required condition. |

| Margin requirement | The rule or threshold that determines required equity or collateral. | Defines the line that the account must stay above. |

| Margin debt | The borrowed amount or financed exposure supported by the account. | Shows the size of the leverage, not whether a call has occurred. |

| Forced liquidation | A possible consequence if the shortfall is not resolved. | May reduce positions without the account holder choosing the timing. |

| Deleveraging | The broader process of reducing borrowed exposure. | Can follow margin pressure, but a single margin call does not prove broad deleveraging. |

Simple Margin Call Example

Consider a simplified account with financed exposure and a required equity buffer. If the account starts with enough equity but the financed asset declines, the equity buffer can shrink. When that buffer falls below the required threshold, a margin call can occur.

For example, an account may hold financed exposure worth 100 units with 40 units of equity and 60 units of borrowed funding. If the exposure falls to 80 units while the borrowing remains 60 units, equity falls to 20 units. If the required equity level is above that amount, the account has a shortfall. The exact response depends on the applicable rules, but the mechanism is the same: the collateral cushion became too small for the financed exposure.

This example is illustrative only. It is not a broker rule, not a universal margin formula, and not a historical market episode. Real requirements can differ across asset classes, account types, brokers, lenders, exchanges, and jurisdictions.

Why Margin Calls Matter for Market Structure

A margin call matters beyond the individual account when collateral pressure becomes clustered. One isolated call may only be an account-level event. Many similar shortfalls can create broader demand for liquidity because participants may need cash, eligible collateral, or exposure reduction at the same time.

The market-structure path is conditional. A price move reduces collateral capacity. Lower collateral capacity can create margin calls. Margin calls can create liquidity demand. Liquidity demand can lead to position reduction. If the same pressure appears across many leveraged accounts, it can contribute to forced-flow behavior.

Conditional transmission path: price move → lower collateral cushion → margin call → liquidity demand → possible exposure reduction → possible forced-flow pressure.

This does not mean every margin call becomes a systemic event. Scale, liquidity depth, concentration, financing terms, and the ability to restore collateral all affect whether the pressure remains local or becomes part of a broader market adjustment.

What Can Happen After a Margin Call

The next step depends on the rules of the account, broker, lender, exchange, product, and jurisdiction. A margin call is best understood as a shortfall event, not as one fixed outcome.

| Possible response | What it changes | Market-structure relevance |

|---|---|---|

| Additional cash or eligible collateral | Restores the account buffer without reducing exposure. | Creates liquidity demand but may avoid selling pressure. |

| Voluntary position reduction | Lowers financed exposure and required support. | Can add supply to the market if many accounts reduce exposure together. |

| Provider-driven liquidation | Reduces exposure if the shortfall remains unresolved under applicable rules. | Can become forced-flow pressure when it occurs across many participants or illiquid assets. |

| Requirement adjustment | Changes the required equity or collateral level. | Can tighten or loosen pressure depending on how rules are applied. |

Margin Calls in Long and Short Exposure

Most simple explanations focus on a financed long position that falls in value. That is only one version of the mechanism. A short position can also create margin pressure because a rising borrowed asset increases the cost of maintaining the short exposure.

In short exposure, the pressure can connect with short covering. If the short seller must reduce the position, buying back the borrowed asset may become part of the adjustment process. That still does not make every margin call a squeeze. The broader effect depends on position concentration, liquidity, and whether many participants face the same pressure.

Common Misunderstandings

Misunderstanding 1: a margin call is the same as forced liquidation.

Correction: the call is the shortfall event or demand. Liquidation is a possible later consequence if the shortfall is not resolved under the applicable rules.

Misunderstanding 2: a margin call automatically means the market will fall.

Correction: one margin call is usually account-level information. Broader market impact requires scale, concentration, liquidity stress, or clustered exposure reduction.

Misunderstanding 3: all brokers and products use the same margin rules.

Correction: requirements can differ by account type, asset class, product, provider, exchange, and jurisdiction. Provider or exchange rules may be stricter than a general regulatory minimum.

Where This Fits in the Leverage and Forced-Flow Cluster

Margin call is the entity page for the shortfall event itself. For the broader process of reducing borrowed exposure, use the page on deleveraging. For the threshold that determines whether an account has enough equity or collateral, use the page on margin requirement.

For a more detailed process view, see how margin calls work.

Margin Call FAQ

Is a margin call the same as forced liquidation?

No. A margin call is the demand or warning created by an equity or collateral shortfall. Forced liquidation is a possible later consequence if the shortfall is not resolved under the applicable rules.

Does a margin call always mean positions will be sold?

No. A margin call can be resolved in different ways depending on the account, broker, product, and rules involved. Selling or liquidation is possible, but it is not automatic in every case.

Can short positions trigger margin calls?

Yes. If a short position moves against the borrower, the account may require more equity or collateral to support the exposure. That pressure can create a margin call if the account falls below the required level.

Why do margin calls matter for broader markets?

They matter when collateral pressure is clustered. If many leveraged participants need liquidity or exposure reduction at the same time, margin pressure can contribute to forced-flow dynamics. The broader impact remains conditional, not automatic.