Leverage, deleveraging and forced flows describe a pressure chain in which financed exposure can become market pressure when funding, collateral, volatility, liquidity or positioning conditions force participants to reduce risk.

Leverage is the exposure layer. Deleveraging is the reduction layer. Forced flows are the market-impact layer that can appear when risk reduction becomes less discretionary and more mechanical.

The useful market-structure question is not whether leverage exists. The better question is which pressure point is active: financing, collateral, volatility, liquidity, positioning or a forced exit channel.

Which Concept Explains Which Pressure?

The table separates the main pressure questions so exposure, risk reduction, collateral stress, liquidity strain and position reversal are not collapsed into one explanation.

| Reader question | Main concept | Why it matters | Read next |

|---|---|---|---|

| How much exposure is being carried? | Leverage | Shows how borrowed money, derivatives or financed positions can magnify sensitivity to price moves and funding changes. | leverage |

| Are participants reducing exposure? | Deleveraging | Shows the process of shrinking risk, repaying financing, closing positions or reducing gross exposure. | deleveraging |

| Is collateral pressure forcing action? | Margin call | Shows when a participant must add collateral or reduce exposure because account equity, volatility or margin rules have changed. | margin call |

| Are rules or constraints forcing position closure? | Forced liquidation | Shows when selling or position reduction is driven by constraints rather than a discretionary market view. | forced liquidation |

| Is leverage building across margin accounts? | Margin debt | Can help frame whether financed exposure has been building before a stress event, without proving forced selling by itself. | margin debt |

| Are short positions being closed? | Short covering | Shows buying pressure that can come from short sellers reducing or closing positions. | short covering |

| Is short positioning creating a squeeze dynamic? | Short squeeze | Shows how concentrated short exposure can create forced or urgent buying when price moves against shorts. | short squeeze |

| Which rules determine required collateral? | Margin requirement | Shows how collateral rules can change the pressure on leveraged exposure. | margin requirement |

| How does a margin call process work? | Margin-call mechanics | Shows the operational path from collateral shortfall to added funds, position reduction or liquidation risk. | how margin calls work |

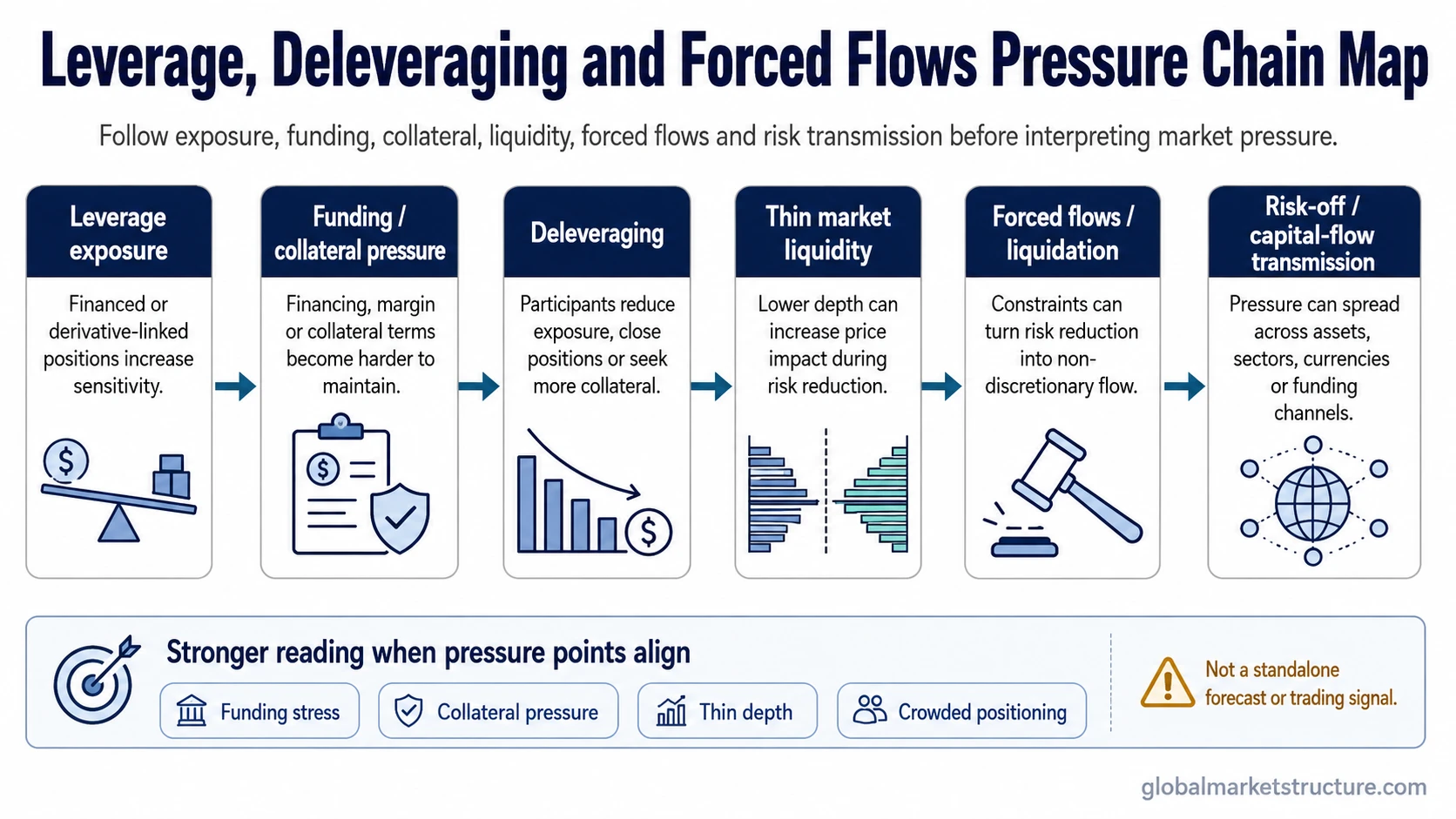

The Pressure Chain

A leverage cycle becomes more fragile when exposure, financing and market liquidity start interacting. The chain is strongest when several links appear together rather than when one metric looks elevated in isolation.

- Exposure builds: Investors, funds or other participants carry positions using borrowing, derivatives, margin or other forms of financed exposure.

- Funding or collateral pressure rises: Higher volatility, tighter financing, weaker collateral values or stricter margin rules make the exposure harder to maintain.

- Deleveraging begins: Participants reduce gross exposure, cut position size, sell assets, close derivatives or seek more collateral.

- Market liquidity becomes important: If trading depth is thin, the same reduction in exposure can create larger price impact.

- Forced flows appear: Liquidations, margin-driven selling, urgent short covering or systematic risk reductions can push prices beyond what discretionary views alone would suggest.

- Risk transmission broadens: Pressure can move across assets, sectors, currencies or funding markets when participants reduce risk at the same time.

Funding Liquidity and Market Liquidity Are Different

Funding liquidity is about the ability to obtain or maintain financing. Market liquidity is about the ability to trade without large price impact. Forced-flow risk often rises when both become strained at the same time.

| Pressure type | What it asks | Market-structure implication |

|---|---|---|

| Funding liquidity | Can participants finance or maintain positions? | Weak funding can push leveraged participants toward exposure reduction even before the market fully reprices the risk. |

| Market liquidity | Can participants exit or rebalance without moving price sharply? | Weak trading depth can turn normal risk reduction into larger price impact. |

| Collateral pressure | Can participants meet changing margin or collateral demands? | Collateral stress can accelerate deleveraging when participants cannot or will not add capital. |

| Positioning pressure | Are many participants exposed in a similar direction? | Crowded positioning can make the adjustment faster if the same side of the market needs liquidity at once. |

Key Pressure Groups

Exposure build-up: Leverage changes sensitivity. A small price move can create a larger portfolio, collateral or risk-control response when exposure is financed.

Collateral stress: A margin call does not always lead to liquidation, but it can force a decision: add capital, reduce risk or accept position closure.

Funding strain: When financing becomes harder to obtain or more expensive to maintain, participants may reduce positions even if their original market view has not changed.

Execution strain: Market liquidity determines whether exposure reduction can happen smoothly or whether selling, hedging or covering creates visible price impact.

Short-position reversal: Short covering can create buying pressure. A short squeeze is a more intense version where positioning, price movement and urgency interact.

Crowding risk: A crowded trade is not automatically a forced-flow event, but it can make a reversal more fragile if many participants need the same exit path.

Common Misreads

Leverage is not automatically dangerous. It becomes more fragile when financing, collateral, volatility or liquidity conditions reduce the ability to hold exposure.

Deleveraging is not always forced. Some exposure reduction is deliberate, gradual and orderly.

Forced flows are not a market forecast. They can explain pressure, but they do not guarantee the next direction of a market.

Crowding is not proof of liquidation. Crowding becomes more important when it lines up with funding strain, collateral pressure, poor liquidity or rapid position reversal.

A pressure reading is not a buy or sell signal. It is a market-structure lens for understanding why price movement may become unstable or self-reinforcing.

Neighbor Distinctions

These adjacent concepts often appear in the same market episode, but they do not mean the same thing.

| Distinction | Clean separation |

|---|---|

| Margin call vs forced liquidation | A margin call is a collateral demand. Forced liquidation is the position closure that can follow if the collateral problem is not resolved. |

| Short covering vs short squeeze | Short covering is position reduction by shorts. A short squeeze is a more pressured process where rising prices and concentrated short exposure can force urgent buying. |

| Funding liquidity vs market liquidity | Funding liquidity is about financing access. Market liquidity is about trading depth and price impact. |

| Crowded trade vs confirmed forced flow | Crowding shows exposure concentration. Forced flow requires a pressure mechanism that turns exposure into non-discretionary buying, selling, hedging or liquidation. |

How the Chain Can Appear

A common scenario is that leveraged exposure builds while volatility is low and funding is easy. If volatility rises and collateral demands increase, some participants may reduce positions. If the market is deep, that reduction may be absorbed. If market depth is thin, the same reduction can create sharper price movement. The reading becomes stronger when financing pressure, collateral stress, weak liquidity and crowded positioning appear together.

Where Each Pressure Point Fits

Each pressure point has a different mechanism, so the next useful concept depends on whether the issue is exposure, collateral, funding, liquidity, liquidation or short-position reversal.

Exposure and build-up: Leverage and margin debt explain how financed exposure can accumulate.

Risk reduction: Deleveraging explains how exposure is reduced before or during stress.

Collateral pressure: Margin calls, margin requirements and margin-call mechanics explain the collateral path.

Mechanical exit pressure: Forced liquidation explains non-discretionary position closure.

Short-position reversal: Short covering and short squeeze explain pressure from short exposure being reduced.

Broader liquidity stress: liquidity crisis and liquidity spiral apply when stress extends beyond one position or market segment.