Leverage in finance means using borrowed money, debt, margin, derivatives, or another financing structure to control exposure larger than the capital directly committed. It can amplify gains and losses. In market structure, leverage matters because financed exposure can become fragile when funding, collateral, volatility, or liquidity conditions force participants to reduce risk.

What leverage means: leverage is financed exposure. A participant uses capital plus some form of financing to carry a larger position, asset base, or risk exposure than its own capital alone would support.

How margin fits: margin is one way leverage can be created, but leverage is the broader financed-exposure concept.

What leverage changes: leverage changes sensitivity. Smaller moves in the underlying asset, funding cost, collateral value, or volatility level can have a larger effect on the leveraged participant.

What leverage does not mean: leverage is not a forecast, a timing signal, or proof that forced selling is about to happen. It describes how exposure is financed and how fragile that exposure may become under pressure.

What Leverage Means in Finance

At the simplest level, financial leverage allows an investor, company, fund, or trading desk to control more exposure than it could control with its own capital alone. The financing can come from borrowing, margin, debt issuance, derivatives, securities lending, or another structure that creates exposure beyond cash paid up front.

The useful market-structure definition is broader than borrowed money. Leverage is the relationship between the capital at risk and the exposure being carried. A lightly financed position may absorb volatility without forced adjustment. A highly financed position may become sensitive to small changes in collateral value, funding terms, or liquidity.

That distinction matters because leverage can look stable while prices are calm. The pressure often appears when asset values fall, volatility rises, financing becomes more expensive, or lenders require more collateral. Under those conditions, the leveraged participant may need to reduce exposure even if the original view has not changed.

What Leverage Changes

Leverage changes the size of exposure relative to committed capital. If a participant controls a larger exposure with a smaller equity cushion, both favorable and unfavorable moves have a larger effect on that cushion.

It also changes the importance of funding conditions. A position that depends on borrowing or margin is not only exposed to price movement. It can also be exposed to financing cost, collateral requirements, volatility adjustments, and the ability to roll or maintain funding.

Exposure: leverage increases the exposure carried for each unit of own capital.

Sensitivity: gains and losses can move faster relative to the capital base.

Fragility: the position may depend on funding access, collateral value, liquidity, and volatility conditions.

Market effect: if many participants reduce exposure at the same time, leverage can become part of a broader pressure chain.

Leverage vs Margin, Debt, and Leveraged Finance

Leverage is the broad concept. Margin is one way leverage can be created, especially when securities are financed with borrowed funds and collateral. A margin call is a collateral demand inside that structure, not the same thing as leverage itself.

A leverage ratio measures leverage, but it does not define every leverage structure. Debt-to-equity, assets-to-equity, and other ratios can show how much financing supports an entity or position, but the market effect depends on context, liquidity, maturity, collateral, and who holds the exposure.

Leveraged finance usually refers to corporate or institutional borrowing structures, such as loans or debt issued by more indebted companies. That is related to leverage, but it is not the same as all financial leverage in markets.

Operating leverage is different again. It describes how fixed costs can make earnings more sensitive to revenue changes. Financial leverage, in this market-structure sense, focuses on financed exposure and the pressure that can appear when funding or collateral conditions change.

| Term | What it means | How it differs from leverage |

|---|---|---|

| Leverage | Financed exposure larger than capital directly committed. | The broad concept that can appear through several structures. |

| Margin | Borrowing or collateralized financing used to carry exposure. | One structure that can create leverage. |

| Leverage ratio | A measurement of financing relative to capital, equity, or assets. | A metric, not the full mechanism. |

| Leveraged finance | Institutional or corporate borrowing involving more indebted issuers. | A specific finance category, not every form of leverage. |

| Operating leverage | Earnings sensitivity caused by fixed costs. | Business-model sensitivity, not financed market exposure. |

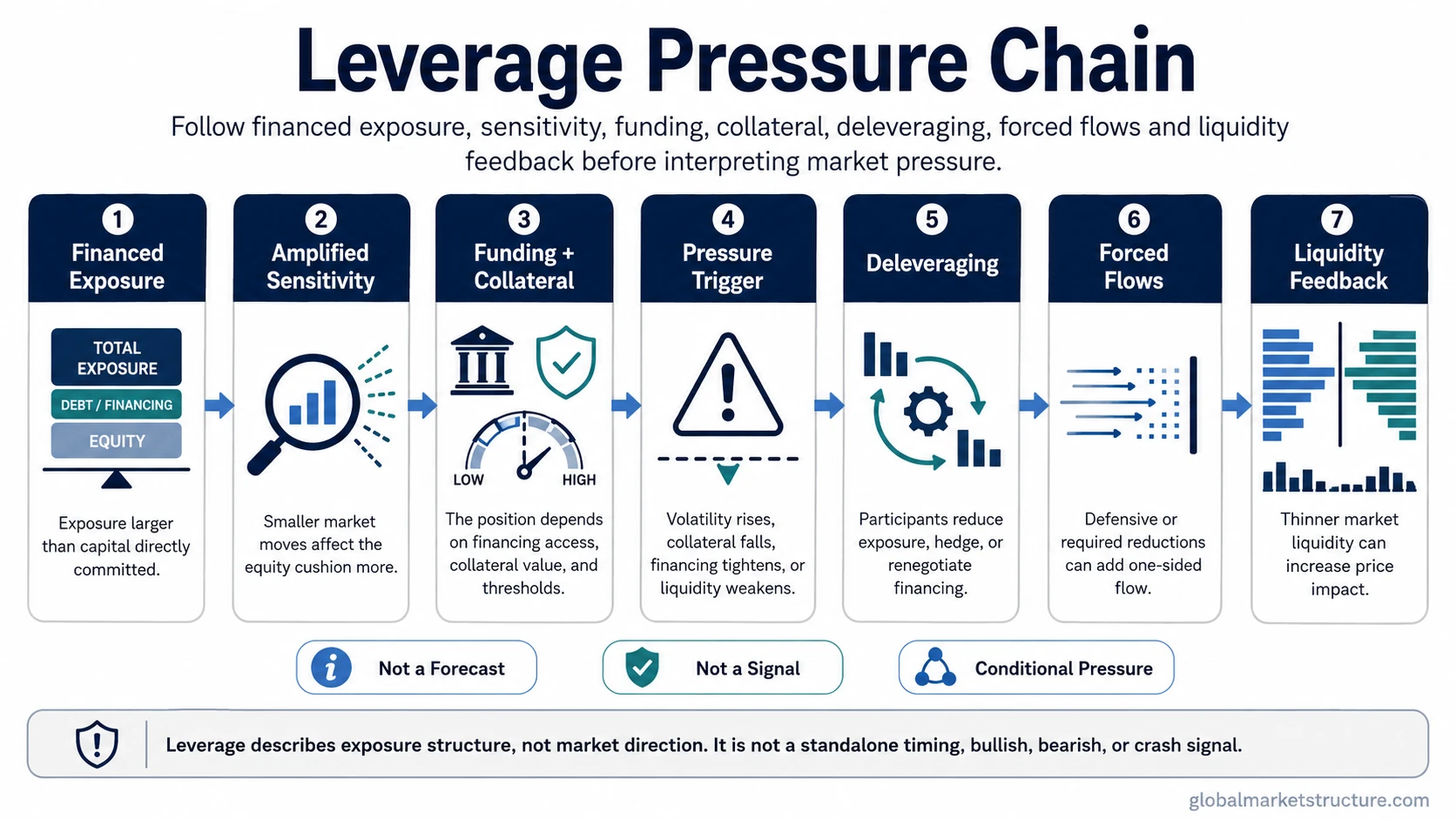

The Leverage Pressure Chain

Leverage becomes most important for market structure when financing turns a normal price move into a balance-sheet, collateral, or liquidity problem. The chain does not require a crash forecast. It describes how financed exposure can transmit pressure when several conditions line up.

| Chain step | What changes | Why it matters | Limitation |

|---|---|---|---|

| Financed exposure | A participant controls more exposure than its own capital alone would allow. | The capital cushion is smaller relative to the exposure carried. | Financing alone does not prove fragility if funding is stable and exposure is well supported. |

| Amplified sensitivity | Price changes have a larger effect on equity, collateral, or risk limits. | Small market moves can matter more to the leveraged participant. | Sensitivity depends on size, structure, hedging, maturity, and liquidity. |

| Funding and collateral dependence | The position depends on financing access, collateral value, and threshold rules. | Pressure can come from funding terms, not only from price direction. | Precise rules vary by structure and require source-specific verification. |

| Pressure trigger | Collateral falls, volatility rises, financing tightens, or liquidity weakens. | The participant may need to post more collateral, hedge, reduce risk, or sell assets. | A trigger does not always force immediate reduction. |

| Participant response | Exposure is reduced, hedges are adjusted, or financing is renegotiated. | This is where deleveraging can begin. | Reduction can be orderly if liquidity is deep and counterparties remain flexible. |

| Market-structure effect | Forced or defensive flows interact with thinner liquidity. | Price impact can increase when many participants respond in the same direction. | The effect is conditional, not automatic. |

| Limitation | Leverage describes exposure structure, not market direction. | It helps explain pressure once stress appears. | It is not a standalone bullish, bearish, timing, or crash signal. |

When Leverage Becomes More Important

Leverage becomes more important when exposure is both large and dependent on conditions that can change quickly. Crowded positioning, rising volatility, falling collateral values, tighter financing, and weaker liquidity can make leveraged exposure harder to maintain.

The pressure is stronger when several conditions appear together. A single leveraged position may not matter to the broader market. Many similar positions, funded in similar ways, reacting to the same collateral or volatility shock, can create a more visible market-structure effect.

A margin requirement can matter in this process because collateral thresholds shape how much exposure a participant can maintain. If collateral support weakens, the same exposure may require more capital or less leverage.

What Leverage Does Not Tell You

Leverage is not automatically bullish or bearish. The same leverage structure can support rising exposure in calm conditions or create pressure when funding and collateral conditions deteriorate.

Leverage is not a timing signal. A market can carry leverage for a long time without immediate stress if liquidity is deep, volatility is contained, and financing remains available.

Leverage is not the same as forced selling. Forced reduction depends on collateral terms, liquidity, risk limits, counterparties, and market conditions. Forced liquidation is a narrower case where exposure is reduced involuntarily.

Leverage is not a complete systemic-risk claim by itself. Broader risk depends on who is leveraged, how the exposure is funded, whether positions are crowded, and how much liquidity is available when risk is reduced.

A Practical Scenario

A fund carries a financed position while market liquidity is calm. The position is not necessarily unstable at the start because collateral is sufficient, financing is available, and price changes remain manageable.

The read becomes incomplete if the analysis stops there. If the asset falls, volatility rises, and financing terms become less flexible at the same time, the fund may need to reduce exposure or post more collateral. The pressure is no longer only about the asset view. It is also about whether the financing structure can survive the new conditions.

The stronger market-structure case appears when many participants face similar constraints while liquidity is thinning. The weaker case appears when financing remains stable, collateral remains sufficient, and buyers can absorb reductions without large price impact.

Related Concepts

Leverage is the starting point for several nearby concepts, but each one explains a different part of the pressure chain.

Exposure reduction: deleveraging explains the process of reducing larger exposure after risk, funding, or collateral pressure rises.

Collateral demand: a margin call describes a demand for more collateral inside a margin structure, while leverage is the broader financed exposure concept.

Aggregate borrowing indicator: margin debt can be used as one related measure of borrowing against securities, but it should not be treated as the same thing as all leverage.

Forced buying distinction: a short squeeze involves pressure on short exposure and can create forced buying, which is different from the broader leverage pressure chain.

FAQ

What is leverage in finance?

Leverage in finance means using borrowed money, debt, margin, derivatives, or another financing structure to control exposure larger than the capital directly committed. It can amplify gains and losses because the exposure is larger than the capital base supporting it.

Is leverage the same as margin?

No. Margin is one structure that can create leverage. Leverage is the broader concept of financed exposure, while margin usually refers to collateralized borrowing or account-based financing used to carry that exposure.

Does leverage always lead to forced selling?

No. Leverage can remain stable when funding is available, collateral is sufficient, volatility is controlled, and liquidity is deep. Forced selling becomes more likely only under specific pressure conditions, such as falling collateral values, tighter financing, weak liquidity, or binding risk limits.