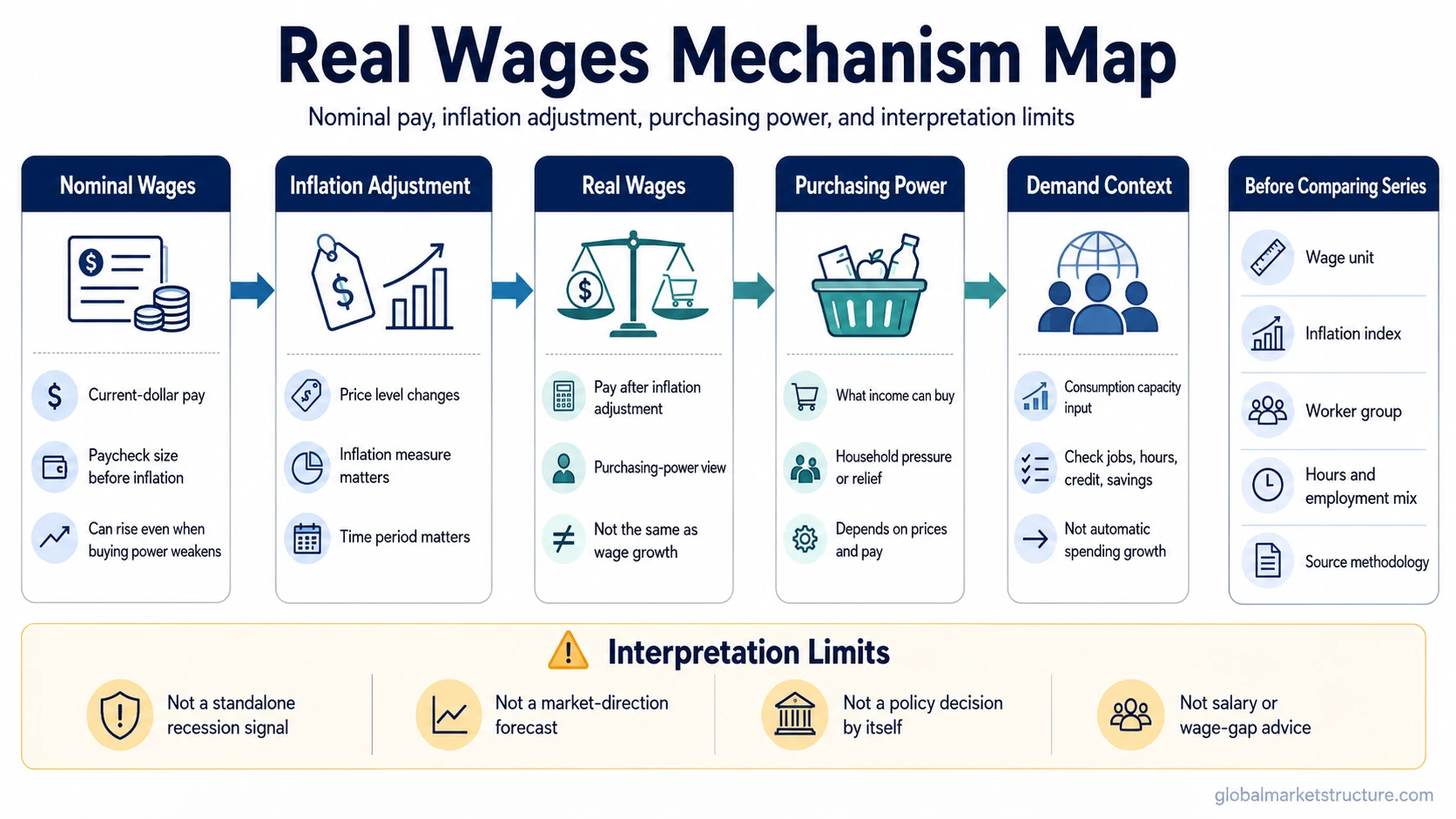

Real wages are wages adjusted for inflation, so they describe purchasing power rather than the dollar amount on a paycheck. They differ from nominal wages, which are measured before inflation adjustment. A real-wage reading depends on the inflation measure, worker group, source methodology, and surrounding labor and consumption conditions, so it should not be treated as a standalone market, recession, or policy signal.

- Real wages measure pay after inflation adjustment, not paycheck size alone.

- Nominal wages can rise while purchasing power falls if prices rise faster.

- Real wage growth tracks the change in inflation-adjusted wages over time.

- Series comparisons need wage unit, inflation measure, worker group, and time-period context.

- Real wages are context inputs, not standalone forecasts for spending, recession, policy, or markets.

What Are Real Wages?

Real wages describe how much labor income is worth after adjusting for changes in prices. The concept matters because a larger paycheck in dollar terms does not always mean a worker can buy more goods and services. If prices rise faster than pay, nominal wages may increase while real wages weaken.

The basic idea is simple: nominal pay shows the current-dollar wage, while real pay adjusts that wage for inflation. The inflation adjustment turns a wage number into a purchasing-power measure. That makes real wages useful for reading household income pressure, consumer capacity, and labor-income conditions, but only with proper measurement context.

Core distinction: nominal wages show the wage before inflation adjustment. Real wages show what that wage is worth after inflation changes purchasing power.

Real Wages vs Nominal Wages

The difference between real wages and nominal wages is the inflation adjustment. Nominal wages can make pay look stronger because they show the dollar amount received. Real wages ask whether that pay has gained or lost buying power after prices change.

| Concept | What it measures | How to read it |

|---|---|---|

| Nominal wages | Pay measured in current dollars before inflation adjustment | Useful for seeing paycheck size, but not purchasing power |

| Real wages | Pay adjusted for inflation | Useful for seeing whether wages buy more or less over time |

| Wage growth | The change in wages before or apart from inflation adjustment | Can look strong even when purchasing power is flat or falling |

| Real wage growth | The change in inflation-adjusted wages | Shows whether wage gains are outpacing price increases |

| Purchasing power | What income can buy after prices are considered | Connects wages to household financial pressure and consumption capacity |

A practical scenario is a worker receiving a higher paycheck while prices rise even faster. The worker earns more dollars, but those dollars buy less than before. In that situation, nominal wages are rising, while real wages are falling.

Real Wage Growth

Real wage growth is the change in inflation-adjusted wages over time. It is not the same as ordinary wage growth, because wage growth may describe pay changes before inflation is considered.

The distinction is important when wage gains and price increases move at different speeds. If nominal wages rise faster than prices, real wage growth is positive. If prices rise faster than nominal wages, real wage growth is negative. If they rise at similar rates, purchasing power may not change much even though paycheck values are higher in dollar terms.

Real wage growth is therefore a purchasing-power measure, not a complete labor-market diagnosis. It does not show whether more people are working, whether hours have changed, whether benefits have shifted, or whether wage gains are concentrated in one worker group.

How Real Wages Connect to Purchasing Power and Demand

Real wages connect labor income to household purchasing power. When real wages improve, workers may have more income capacity after prices are considered. When real wages weaken, households may feel pressure even if nominal wages are still rising.

That purchasing-power channel can matter for consumer spending, but it is not the only input. Spending also depends on employment, hours worked, savings, credit access, debt service, confidence, wealth effects, and the distribution of income gains across households.

Real wages can also affect aggregate demand context because household income is one part of total demand pressure. Still, the relationship is conditional. Stronger real wages can support consumption capacity, but they do not automatically mean broad demand will accelerate. Weaker real wages can create stress, but they do not automatically mean consumption must contract.

Why Real Wages Can Be Misread

Real wages can be misread when the inflation adjustment, wage series, worker group, or time period is unclear. A real-wage measure based on hourly earnings can tell a different story from one based on weekly earnings. A broad average can hide differences across lower-wage, middle-wage, and higher-wage workers.

Labor-force composition also matters. If the mix of workers changes, an average wage measure can move for reasons that do not reflect a clean improvement or deterioration for a typical worker. Participation, employment status, and hours worked should be checked alongside wage data. For that labor-supply context, the labor force participation rate helps separate wage purchasing power from labor-force attachment.

Before comparing real-wage series: check the wage unit, inflation adjustment, worker population, time period, frequency, and whether the measure uses hourly earnings, weekly earnings, or another labor-income series.

Source context matters as well. Different datasets can use different definitions, inflation measures, units, frequencies, and worker populations. A real-wage reading should therefore be treated as a measured statistic with assumptions, not as a self-contained truth about every worker or every household.

What Real Wages Do Not Tell You Alone

Real wages are not a standalone signal. They do not, by themselves, forecast recession, central-bank policy, consumer spending, or asset direction. They are one purchasing-power input that needs labor-market, inflation, credit, savings, confidence, and demand context.

A higher real-wage reading can still coincide with weak demand if employment is soft, hours are falling, credit conditions are tight, or households are rebuilding savings. A lower real-wage reading can still coincide with resilient spending if job growth, savings buffers, or credit access offset part of the pressure.

Real wages should also not be treated as a salary-advice concept. They help interpret inflation-adjusted labor income in macro context. They do not answer whether a job offer is fair, whether a worker should negotiate, or whether wage gaps exist between groups.

Related Labor and Demand Concepts

Real wages sit between wage data and household demand interpretation. Nominal wage growth shows the pay change before inflation adjustment. Real wages show the purchasing-power effect after prices are considered. Consumption data then shows how households actually spend, save, borrow, or absorb pressure.

Soft-data measures can add another layer. The Consumer Sentiment Index does not measure real wages, but it can help show how households feel about economic conditions, inflation pressure, and future expectations. That sentiment layer can differ from wage data because people respond not only to income, but also to prices, job security, debt, and expectations.

Real wages are most useful when they are read as part of a broader labor and demand picture: nominal wages, inflation adjustment, real purchasing power, participation, employment, hours, confidence, and spending behavior. The concept is strongest as a context input, not as a prediction tool.

FAQ

What is the difference between real wages and nominal wages?

Nominal wages are wages measured in current dollars before inflation adjustment. Real wages adjust nominal wages for inflation, so they show purchasing power rather than paycheck size alone.

Can nominal wages rise while real wages fall?

Yes. If nominal wages rise but prices rise faster, the paycheck is larger in dollar terms but buys less than before. In that case, nominal wages are up while real wages are down.

Is real wage growth the same as wage growth?

No. Wage growth can refer to the change in wages before inflation adjustment. Real wage growth refers to the change in wages after inflation is considered.

Do real wages predict consumer spending or markets?

No. Real wages can influence purchasing-power context, but they do not predict consumer spending, recession, policy, or market direction by themselves. Employment, hours, credit, savings, confidence, and inflation context also matter.