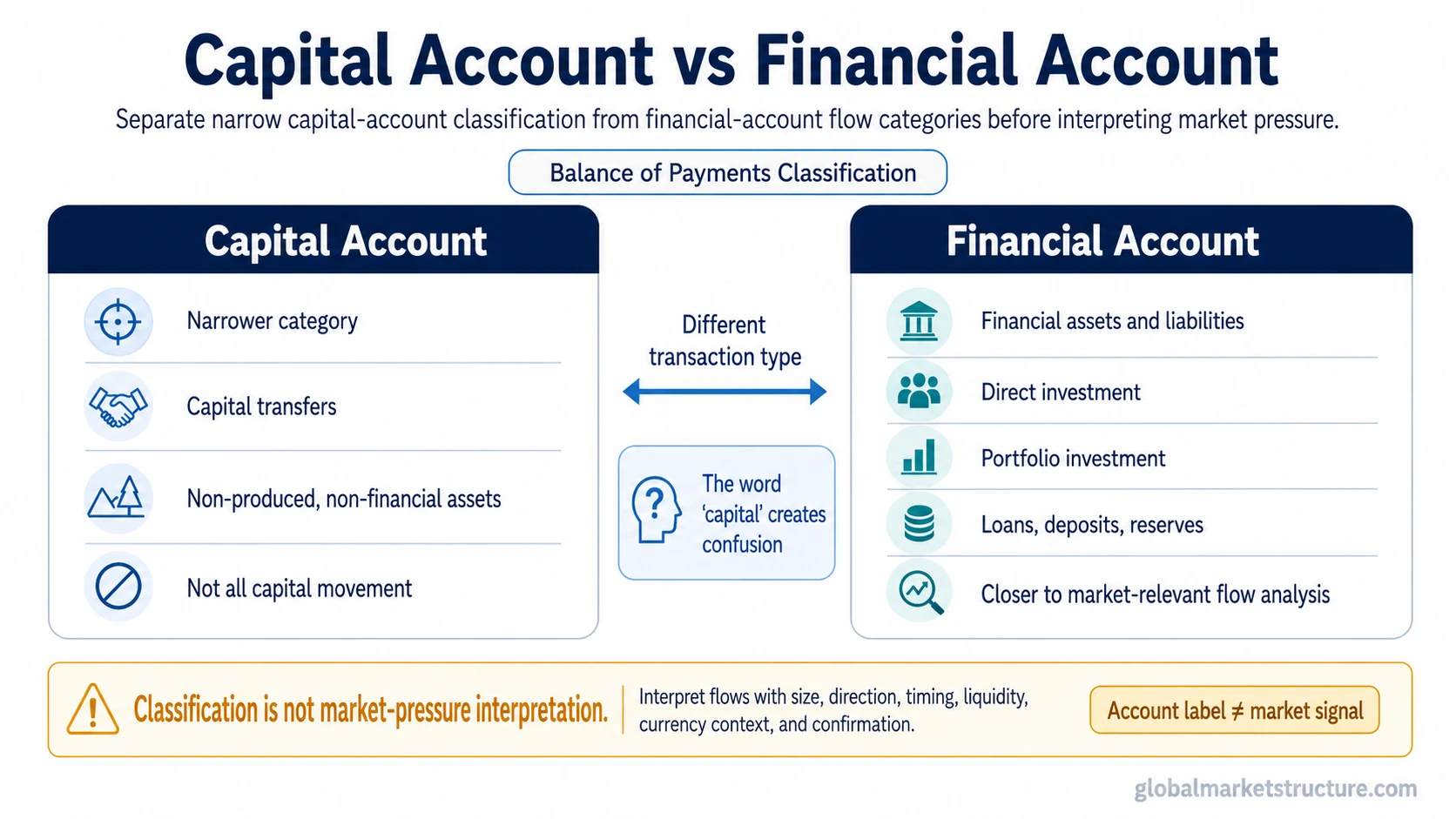

Capital account vs financial account is a balance-of-payments distinction, not just a wording difference. In standard balance-of-payments classification, the capital account is the narrower category for capital transfers and transactions in non-produced, non-financial assets. The financial account records transactions in cross-border financial assets and liabilities, including many investment-style flows.

Direct distinction: the capital account classifies certain transfers and non-produced asset transactions. The financial account classifies transactions in financial assets and liabilities. A market discussion about capital moving across borders usually belongs closer to financial-account and flow analysis than to the narrow capital-account category.

Key Points

- The capital account is narrow in many balance-of-payments classifications.

- The financial account records cross-border transactions in financial assets and liabilities.

- The phrase “capital flows” can sound like it belongs in the capital account, but many market-relevant flows are financial-account items.

- Account labels organize transactions. They do not automatically explain currency pressure, equity flows, bond-market stress, or risk appetite.

Capital Account vs Financial Account: The Core Difference

The capital account records capital transfers and transactions in non-produced, non-financial assets. The financial account records cross-border transactions in financial assets and liabilities. The simplest difference is that the capital account is about certain transfer and ownership-right categories, while the financial account is about financing, investment, and claims across borders.

| Comparison point | Capital account | Financial account |

|---|---|---|

| Main role | Records capital transfers and non-produced, non-financial asset transactions. | Records cross-border transactions in financial assets and liabilities. |

| Typical scope | Narrower in standard balance-of-payments classification. | Broader for market-relevant investment and financing flows. |

| Common examples | Capital transfers, debt forgiveness in some classifications, and rights to non-produced assets. | Direct investment, portfolio investment, loans, deposits, reserve-asset changes, and other financial claims, depending on classification. |

| Market interpretation | Useful for classification, but usually not the main label for investment-flow pressure. | More directly connected to cross-border financing and investment-flow analysis. |

| Main confusion | The name sounds broad because it contains “capital.” | The category often contains the flows market participants mean when they discuss capital moving across borders. |

What the Capital Account Records

The capital account records a limited set of balance-of-payments transactions. In narrower usage, it is not a general bucket for all capital moving into or out of a country. It focuses on capital transfers and transactions involving non-produced, non-financial assets.

Terminology note: the word “capital” can make the capital account sound like the natural home for all cross-border capital movement. In balance-of-payments classification, that is usually too broad. Many financial movements are recorded in the financial account instead.

That distinction matters because market language and accounting classification do not always use the same boundary. A macro comment about foreign capital entering local bonds, equities, deposits, or direct investment is usually closer to financial-account analysis than to narrow capital-account classification.

What the Financial Account Records

The financial account records transactions that change cross-border ownership of financial assets and liabilities. It is the category more closely tied to investment-style flows, financing claims, and ownership of financial instruments across borders.

Financial-account items can include direct investment, portfolio investment, lending, deposits, reserve-asset changes, and other financial claims, depending on the classification system being used. These items are usually more relevant when analyzing cross-border flows and external financing pressure.

Important limitation: a financial-account entry still does not become a market signal by itself. Interpretation depends on size, direction, timing, currency context, financing conditions, and whether other markets confirm or contradict the flow pressure.

Why the Two Accounts Are Confused

The confusion usually comes from the difference between everyday market language and balance-of-payments classification. Market participants often use “capital flows” as a broad phrase for money moving across borders. Balance-of-payments categories are more specific.

That means capital flows can describe a broad market process, while the capital account can describe a narrower accounting category. The two labels overlap in wording, but they should not be treated as identical.

Common mistake: treating “capital account” as shorthand for every cross-border investment flow. In narrower balance-of-payments usage, many of those flows belong in the financial account, not the capital account.

Same Cross-Border Scenario, Different Account Reading

A foreign investor purchases domestic government bonds through a local financial institution. The market discussion may describe this as foreign capital entering the bond market. In balance-of-payments classification, the transaction is more likely to be treated as a financial-account item because it changes cross-border ownership of a financial asset.

A different transaction may involve a transfer of ownership rights to a non-produced, non-financial asset. That belongs closer to the capital-account boundary. Both situations can involve cross-border economic value, but the account classification changes because the transaction type is different.

Same broad idea, different classification: cross-border value movement is not enough to identify the account. The classification depends on whether the transaction is a capital transfer or non-produced asset item, or whether it changes financial assets and liabilities.

Why Account Classification Is Not Market-Pressure Interpretation

Balance-of-payments accounts organize transactions. They do not automatically explain whether a currency should strengthen, whether bond yields should move, or whether risk assets should react. The label tells what kind of transaction was recorded, not the full market effect.

Market-pressure interpretation needs more context. Flow direction matters, but so do scale, persistence, hedging behavior, local liquidity, foreign-exchange intervention, reserve changes, funding conditions, and the surrounding risk environment. A small financial-account flow in a deep market may matter less than a smaller-looking flow in a fragile funding environment.

The useful discipline is to separate classification from interpretation. Account categories help organize flows, but the market reading becomes more meaningful only when the flow is connected to liquidity, currency context, financing stress, and cross-asset confirmation.

Related Concepts

Financial account balance of payments is the cleaner next step for the financial side of the comparison, especially when the question is how investment and financing claims are recorded.

Current account vs capital account helps separate trade, income, and transfer categories from the narrower capital-account label.

Cross-border flow analysis connects the classification question to broader market-structure interpretation without treating the account label as a standalone market signal.