Current account and capital account are different parts of the balance of payments. The current account records cross-border flows tied to goods, services, income, and transfers. The capital account records capital transfers and certain asset-related transactions, while many market discussions also need to separate it from the financial account. The useful question is not simply “trade or money,” but what kind of transaction is being recorded.

Key Points

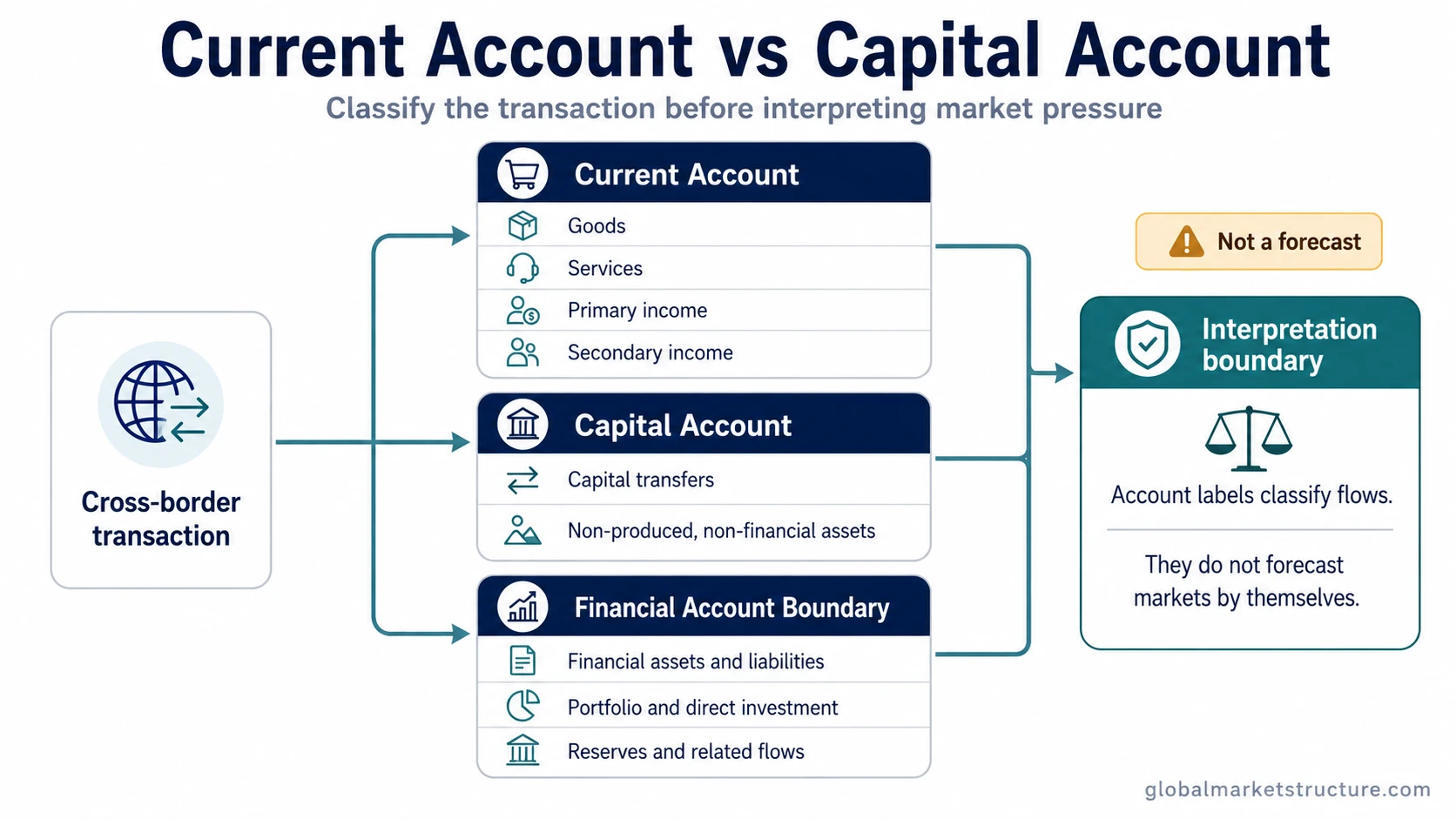

- The current account records goods, services, primary income, and secondary income flows between residents and non-residents.

- The capital account is narrower. It records capital transfers and acquisition or disposal of non-produced, non-financial assets.

- Many financial-asset and liability flows belong to the financial account, not the narrow capital account.

- Account labels classify transactions. They do not forecast exchange rates, equity markets, bond markets, or risk appetite by themselves.

Current Account vs Capital Account: The Core Difference

The current account and capital account both sit inside the balance-of-payments framework, but they answer different classification questions.

The current account asks whether a cross-border transaction is tied to goods, services, income, or current transfers. The capital account asks whether the transaction is a capital transfer or involves certain non-produced, non-financial assets. That makes the capital account much narrower than the casual phrase “capital flows” often suggests.

Core distinction: The current account records recurring trade, service, income, and transfer flows. The capital account records a narrower set of capital-transfer and non-produced-asset transactions. Broader investment flows usually require the financial-account boundary.

Current Account vs Capital Account Comparison Table

| Criterion | Current Account | Capital Account | Common Mistake |

|---|---|---|---|

| Main classification question | Does the transaction involve goods, services, income, or current transfers? | Does the transaction involve capital transfers or certain non-produced, non-financial assets? | Treating the split as simply “trade vs money.” |

| Typical components | Goods, services, primary income, and secondary income. | Capital transfers and acquisition or disposal of non-produced, non-financial assets. | Treating all cross-border investment flows as capital-account items. |

| Economic meaning | Shows trade-related, service-related, income, and transfer flows with the rest of the world. | Captures a narrower set of capital-transfer and asset-category changes. | Confusing the capital account with the broader financial account. |

| Market interpretation use | Can help frame external balance pressure, but only with context. | Helps classify a narrower set of cross-border changes. | Assuming either account directly predicts asset prices. |

| Main limitation | A surplus or deficit is not automatically bullish or bearish. | The capital account alone is usually too narrow for broad market-flow conclusions. | Ignoring financial-account offsets, reserves, hedging, liquidity, and risk appetite. |

What the Current Account Records

The current account records cross-border flows in goods, services, primary income, and secondary income. Goods and services cover trade activity. Primary income usually includes income from labor, direct investment, portfolio investment, and other income relationships. Secondary income covers current transfers where value moves across borders without a direct exchange of goods or services.

A current-account surplus means receipts in these categories exceed payments. A current-account deficit means payments exceed receipts. That classification can matter for macro interpretation, but it does not settle the market question on its own. The surrounding financing conditions, reserve behavior, currency regime, hedging demand, and investor positioning can change how the same current-account balance is absorbed by markets.

What the Capital Account Records

The capital account records capital transfers and transactions involving non-produced, non-financial assets. This makes it a narrower account than many casual explanations imply.

A capital transfer can change an ownership or obligation position without being an ordinary goods, services, or income exchange. Transactions involving certain non-produced, non-financial assets may also fall into this account. The exact classification should follow official balance-of-payments methodology rather than broad market shorthand.

Limitation: The capital account is not a complete map of international investment pressure. Portfolio investment, direct investment, derivatives, reserve assets, and other financial-asset changes are normally handled through the financial account rather than the narrow capital account.

Why the Financial Account Creates Confusion

A common confusion is that “capital account” is sometimes used loosely to describe cross-border investment flows. In stricter balance-of-payments usage, many ownership changes in financial assets and liabilities belong to the financial account rather than the narrow capital account.

Boundary note: Capital account and financial account should remain separate in strict balance-of-payments usage, even when market commentary uses “capital” more broadly. The transaction should be classified first; possible market pressure should be interpreted only after the accounting boundary is clear.

This boundary matters because many financial-asset flows are described casually as capital flows even when strict balance-of-payments classification points to the financial account. If a transaction changes ownership of financial assets or liabilities, it may be a financial-account item. If the transaction records goods, services, income, or current transfers, it belongs in the current account. If it records capital transfers or certain non-produced, non-financial assets, it belongs in the capital account.

Same Scenario, Different Account Classification

The same cross-border environment can produce several different balance-of-payments entries. The account depends on what changed, not on whether money crossed a border.

| Scenario | Likely classification | Reason |

|---|---|---|

| A foreign buyer purchases exported goods from a domestic producer. | Current account | The transaction is tied to goods trade. |

| A domestic company receives income from an investment abroad. | Current account | The transaction is tied to primary income. |

| A cross-border capital transfer changes an ownership or obligation position without an ordinary goods, services, or income exchange. | Capital account, subject to official classification | The transaction may fall under capital-transfer treatment, but final classification should follow official balance-of-payments methodology. |

| A foreign investor buys a domestic bond or equity claim. | Financial account | The transaction changes ownership of a financial asset or liability, so it is not the same as the narrow capital account. |

Why Account Classification Is Not a Market Forecast

Account labels classify transactions. They do not predict market direction. A current-account surplus does not automatically mean a currency should rise. A current-account deficit does not automatically mean a market is weak. A capital-account entry does not automatically prove durable capital pressure.

Account classification connects to capital flows when the question shifts from what was recorded to whether the flow can create pressure. The remaining issue is whether the flow is persistent, expected, hedged, financed smoothly, or occurring during a fragile risk environment.

For example, an external deficit may be financed smoothly during a period of strong investor demand. A surplus may have limited market effect if it is already expected or offset by financial-account flows. The accounting label helps organize the evidence, but the market effect depends on the broader regime.

How This Fits Into Capital Flow Interpretation

Balance-of-payments categories are useful because they stop different flow types from being mixed into one vague story. Goods flows, service flows, income flows, capital transfers, and financial-asset flows can all matter, but they do not carry the same interpretation.

Interpretation sequence: classify the transaction, identify the related flow, check whether the flow is persistent, then examine offsets such as hedging, reserve use, liquidity, financial-account behavior, positioning, and global risk appetite.

This is especially important when reading cross-border flows. A recorded flow may show an external transaction, but market pressure depends on whether that flow changes actual currency demand, financing stress, reserve behavior, or portfolio positioning.

Related Concepts

Current account and capital account labels identify what a cross-border transaction records. Broader flow analysis then asks whether those flows create pressure, how persistent the pressure is, whether the pressure is offset elsewhere, and whether the surrounding market regime makes it more important.

The next useful distinction is between the accounting record and the market-pressure channel. The accounting record tells you where the transaction belongs. The market-pressure channel asks how that transaction interacts with liquidity, financing, hedging, reserves, and risk appetite.

FAQ

Is the capital account the same as the financial account?

No. In strict balance-of-payments usage, the capital account is narrower and covers capital transfers plus certain non-produced, non-financial assets. The financial account records many changes in financial assets and liabilities, such as portfolio investment, direct investment, derivatives, reserves, and other financial flows.

Does a current account surplus mean a currency should rise?

No. A current account surplus can matter for external-balance interpretation, but it does not forecast currency direction by itself. The market effect can depend on expectations, hedging, reserve behavior, financial-account offsets, liquidity, positioning, and broader risk appetite.