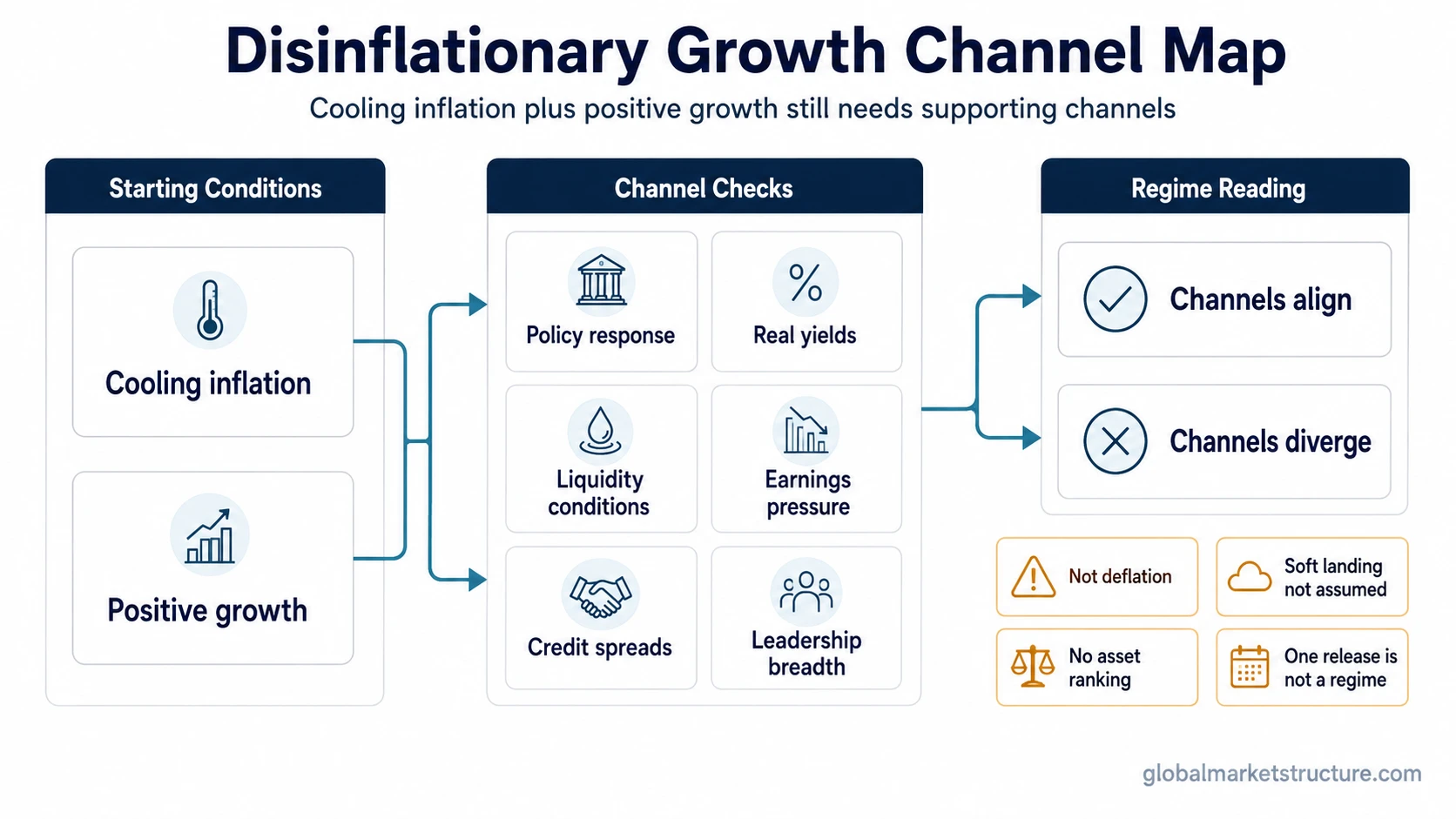

Disinflationary growth is a macro-regime condition where inflation is cooling while economic growth remains positive. It is not the same as deflation, does not guarantee a soft landing, and does not automatically predict asset returns.

The label is useful only when the inflation trend, growth backdrop, policy reaction, real yields, liquidity conditions, earnings pressure, and market leadership are read together. A single inflation release or a short-term market move is not enough to define the regime.

Definition: Disinflationary growth describes an environment where the rate of inflation is slowing, but the economy is still expanding rather than contracting. The growth condition is what separates it from generic disinflation.

Key Points

- Disinflationary growth means inflation is cooling while growth remains positive.

- It is not deflation because the general price level does not need to fall.

- It is not automatically a soft landing or an asset-return signal.

- The interpretation depends on policy, real yields, earnings, liquidity, credit, and market leadership.

What Disinflationary Growth Means

Disinflationary growth combines two conditions. The first is disinflation, meaning inflation pressure is easing or the inflation rate is slowing. The second is positive growth, meaning economic activity is still expanding enough to avoid a contractionary regime label.

That combination can look benign at the headline level because inflation pressure is cooling without an immediate collapse in activity. The interpretation remains conditional because growth can be uneven, policy can remain restrictive, real yields can stay high, and earnings can weaken even while headline growth is still positive.

The concept works best as a regime description, not as a forecast. It describes the relationship between inflation and growth, then requires confirmation from the surrounding macro and market channels.

Disinflationary Growth vs Disinflation and Deflation

The main confusion is that disinflationary growth sounds similar to disinflation, but the two are not identical. Disinflation only describes the direction of inflation. Disinflationary growth adds a growth condition.

| Concept | Core meaning | What it does not prove |

|---|---|---|

| Disinflation | The inflation rate slows, even if prices are still rising. | It does not prove that growth is strong or that policy will ease. |

| Deflation | The general price level falls. | It is not required for disinflationary growth. |

| Disinflationary growth | Inflation cools while growth remains positive. | It does not guarantee a soft landing or positive asset returns. |

| Deflationary bust | Growth weakens or contracts while stress and price pressure deteriorate. | It is not the same as a positive-growth disinflation regime. |

| Reflation | Growth and inflation impulse improve after slowdown, policy support, or easier conditions. | It is not simply lower inflation with stable growth. |

Why the Growth Condition Matters

Disinflation alone can come from several different forces. Inflation may slow because supply pressure eases, demand normalizes, policy is restrictive, credit tightens, or growth begins to weaken. The growth condition matters because it helps separate a healthier cooling-inflation environment from a more fragile slowdown.

When growth remains positive, income, employment, demand, and earnings may have more room to absorb slower inflation. That does not remove risk. It only changes the starting interpretation. If policy remains tight, real yields rise, credit spreads widen, or earnings revisions weaken, the same disinflation signal can become less supportive.

The regime is more coherent when inflation, growth, policy, real-yield, liquidity, earnings, credit, and leadership signals point in the same direction. It becomes less stable when the headline inflation trend improves but the supporting channels deteriorate.

Observable Channels in a Disinflationary Growth Regime

Disinflationary growth is not confirmed by one number. The label becomes more useful when several channels support the same interpretation.

| Channel | What supports the regime reading | What weakens or changes the reading | Why it matters |

|---|---|---|---|

| Inflation trend | Inflation pressure cools over more than one reading. | Inflation reaccelerates or stays sticky in core categories. | The regime begins with disinflation, but the trend needs persistence. |

| Growth data | Output, demand, income, or employment remain positive. | Growth rolls over, demand contracts, or labor weakness broadens. | Positive growth is the difference between disinflationary growth and a stress-led slowdown. |

| Policy reaction | Policy pressure becomes less restrictive without signaling growth stress. | Policy remains tight because inflation is still too high, or easing begins because growth is breaking. | The reason for policy change matters as much as the direction of policy change. |

| Real yields | Real yields do not tighten enough to offset the inflation improvement. | Real yields rise as inflation falls, keeping financial conditions restrictive. | Cooling inflation can still be restrictive if real borrowing costs rise. |

| Earnings and margins | Revenue and margin pressure remain manageable as inflation cools. | Earnings revisions weaken or margins compress despite positive growth. | Growth at the macro level does not automatically protect profits. |

| Liquidity and financial conditions | Credit availability, funding conditions, and market liquidity remain stable. | Credit tightens, funding pressure rises, or liquidity becomes fragile. | A benign inflation trend can be undermined by tightening financial channels. |

| Credit spreads | Spreads remain contained while inflation cools. | Spreads widen as markets price higher default or slowdown risk. | Credit can reveal stress that headline growth has not yet shown clearly. |

| Market breadth and leadership | Participation broadens and leadership is not concentrated in only a few defensive or rate-sensitive areas. | Leadership narrows, defensive behavior dominates, or participation weakens. | Leadership helps show whether the regime is being confirmed broadly or only by a narrow market segment. |

Common False Readings

Cooling inflation is only one part of the regime. The most common mistake is treating disinflation as a complete market conclusion rather than a condition that needs confirmation.

- Cooling inflation does not automatically mean risk assets will rise.

- Cooling inflation does not guarantee lower rates.

- Positive growth does not guarantee a soft landing.

- Leadership rotation is not an asset-ranking framework.

- One data release is not a regime.

- Lower inflation does not always mean easier financial conditions if real yields, credit, or liquidity are tightening.

A stronger interpretation requires alignment between the inflation trend and the surrounding channels. A weaker one appears when inflation cools for reasons that also damage growth, earnings, liquidity, or credit conditions.

How It Differs From Nearby Macro Regimes

Disinflationary growth sits near several macro-regime labels, but the distinctions matter. The same inflation trend can point to different environments depending on whether growth is improving, weakening, or staying resilient.

| Nearby regime | How it differs from disinflationary growth |

|---|---|

| Reflation trade | Reflation focuses on an improving growth and inflation impulse after slowdown, policy support, or easier conditions. Disinflationary growth focuses on cooling inflation while growth stays positive. |

| Deflationary bust | A deflationary bust involves weak or contracting growth and stress conditions. Disinflationary growth still requires positive growth. |

| Stagflation | Stagflation combines persistent inflation pressure with weak growth. Disinflationary growth has cooling inflation and positive growth. |

| Goldilocks | Goldilocks is often used for a more broadly benign mix of growth, inflation, policy, and risk conditions. Disinflationary growth can overlap with that idea, but it is not identical unless the supporting channels also align. |

Practical Scenario: When the Label Can Be Misleading

Inflation may cool across several readings while output and employment remain positive. That can still fit the headline definition of disinflationary growth. The interpretation becomes less stable if real yields stay elevated, credit availability tightens, earnings revisions weaken, and market leadership narrows.

In that setting, the label describes the inflation-growth mix, but it does not confirm a broad low-stress regime. The supporting channels still have to show that growth, liquidity, credit, and earnings are not deteriorating beneath the headline data.

FAQ

What is disinflationary growth?

Disinflationary growth is a macro-regime condition where inflation is cooling while economic growth remains positive.

Is disinflationary growth the same as deflation?

No. Deflation means the general price level is falling. Disinflationary growth means inflation is slowing while growth remains positive, so prices may still be rising.

Is disinflationary growth the same as a soft landing?

No. It can resemble a soft-landing environment, but it does not guarantee one. Policy, real yields, liquidity, credit, earnings, and leadership still need to support the interpretation.

Does disinflationary growth mean risk assets will rise?

No. It is a regime description, not an asset-return signal. Market interpretation depends on the surrounding channels, including policy, real yields, liquidity, earnings, credit, and breadth.

How is disinflationary growth different from reflation?

Disinflationary growth focuses on cooling inflation with positive growth. Reflation focuses on an improving growth and inflation impulse after slowdown, policy support, or easier conditions.