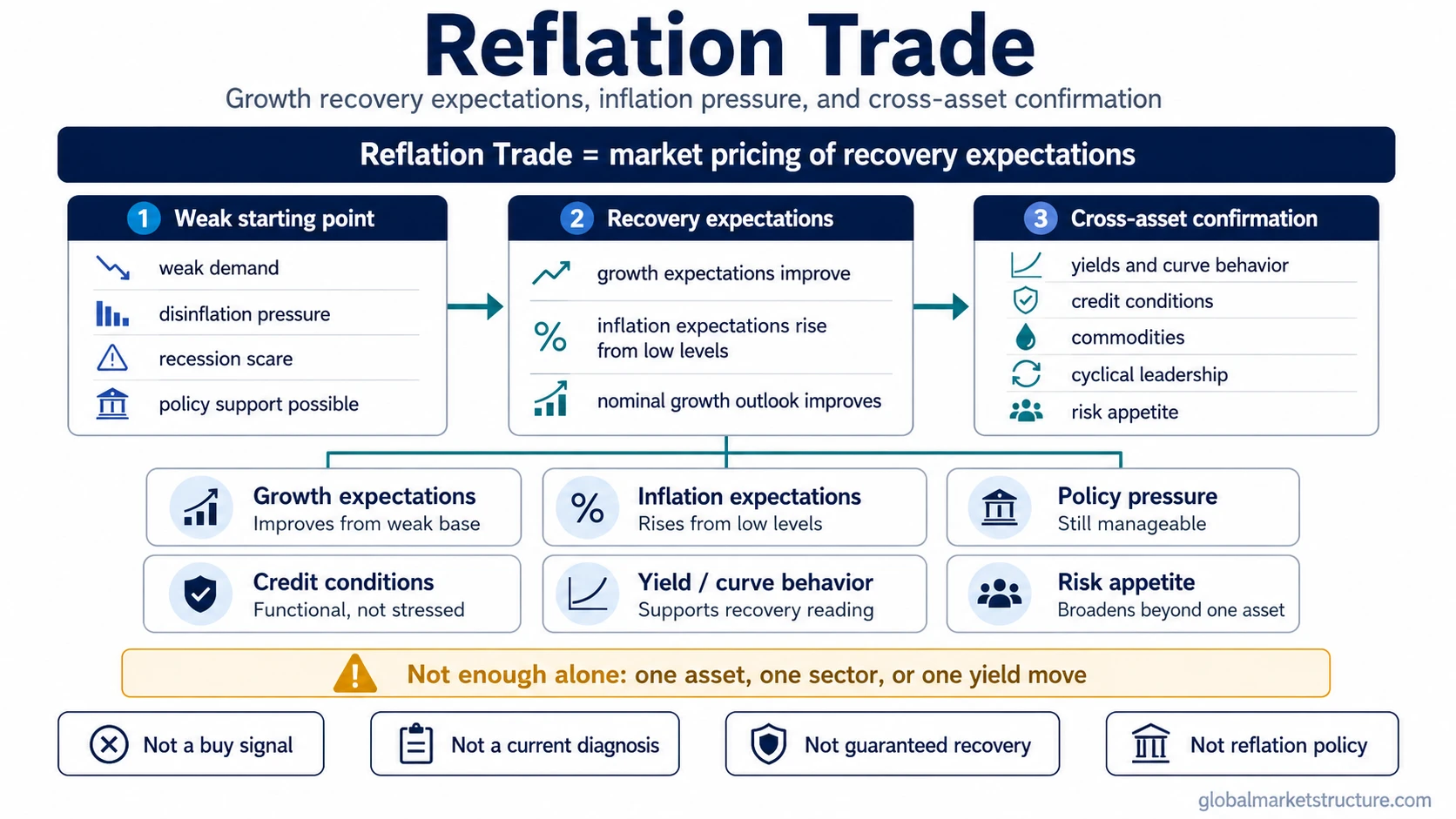

A reflation trade refers to market positioning or cross-asset behavior that reflects expectations of improving growth and rising inflation from a weak, recessionary, or disinflationary starting point. The phrase describes how markets may begin to price a recovery in nominal growth before that recovery is fully visible in realized economic data.

A reflation trade is not the same as reflation policy. It is also not automatically an inflation trade, a stagflation regime, or a standalone trading signal. The label becomes more useful when several market channels point toward the same recovery theme, rather than when one asset or one sector moves in isolation.

Definition

| Item | Meaning |

|---|---|

| Core idea | Market behavior linked to expectations that growth and inflation are recovering from a weak starting point. |

| Starting condition | Usually a downturn, recession scare, deflationary pressure, disinflation, or weak nominal-growth backdrop. |

| Common expression channels | Cyclical assets, value-sensitive areas, financials, commodities, inflation expectations, yields, curve behavior, and broader risk appetite may respond. |

| What it is not | It is not a policy program, a guaranteed recovery, a buy signal, a sector list, or proof that reflation has already arrived. |

Key Points

- A reflation trade is mainly an expectations concept. Markets can price the possibility of stronger nominal growth before the data confirms a durable recovery.

- The phrase is broader than a single asset class. Commodities, yields, cyclical leadership, financials, small caps, value stocks, credit conditions, and risk appetite may all matter, but none of them confirms the theme alone.

- A reflation trade can fail if growth expectations fade, inflation overshoots into policy pressure, credit conditions weaken, or the theme becomes fully priced before the macro recovery is durable.

What a Reflation Trade Means

A reflation trade describes the market expression of a recovery narrative. The underlying idea is that the economy is moving away from weak demand, falling inflation pressure, or recession-like conditions and toward a stronger nominal-growth environment.

That does not mean every asset responds in the same way. Different markets may express the theme through different channels. Cyclical equities may reflect improving earnings expectations. Financials may react to yield-curve changes. Commodities may reflect stronger demand or inflation expectations. Bond yields may rise if investors expect stronger growth, higher inflation, or less need for policy easing.

The concept becomes weaker when it is reduced to a simple asset list. “Reflation trade” does not mean that commodities, banks, value stocks, or small caps must rise. Those markets can move for other reasons, and their meaning changes depending on credit conditions, policy expectations, real yields, earnings expectations, and the broader risk environment.

A cleaner interpretation separates the macro label from the action. A macro label can describe the market environment without automatically becoming an instruction to position in a specific asset. It also keeps reflation separate from adjacent regime labels such as stagflation, where inflation pressure persists while growth weakens.

How the Reflation Trade Mechanism Works

A reflation trade usually begins with a weak or disinflationary backdrop. Growth may be slowing, inflation pressure may be fading, demand may be soft, or markets may be concerned about recession risk.

Policy support or recovery expectations can then change market pricing. Fiscal stimulus, monetary easing, lower real-rate pressure, improving credit conditions, or a turn in growth expectations may lead investors to price a stronger nominal-growth path.

As that expectation develops, inflation expectations may rise from low levels. Nominal yields can move higher, curves may steepen, cyclical leadership may improve, and inflation-sensitive areas may attract attention. This differs from disinflationary growth, where growth may remain stable while inflation pressure cools rather than rises from a weak starting point.

The final interpretation depends on confirmation. A reflation trade becomes more credible when growth expectations, inflation expectations, credit conditions, sector leadership, yields, commodities, and broad risk appetite align. It becomes less credible when the move is isolated, credit stress appears, inflation pressure becomes policy-threatening, or growth data fails to follow market pricing.

Reflation Trade Condition Stack

| Condition | What it suggests | Why it is not enough alone | What weakens the reading |

|---|---|---|---|

| Improving growth expectations | Markets may be pricing recovery from a weak starting point. | Expectations can change before actual data improves. | Growth data fails to recover or forward indicators deteriorate. |

| Rising inflation expectations from low levels | Investors may expect stronger nominal demand. | Inflation expectations can rise because of supply pressure, not healthy demand. | Inflation becomes cost pressure while real growth remains weak. |

| Yield or curve behavior | Higher nominal yields or a steeper curve may reflect recovery expectations. | Yields can rise for many reasons, including risk premium, supply concerns, or policy repricing. | Higher yields begin pressuring risk assets or tightening financial conditions. |

| Cyclical or value leadership | Markets may be rotating toward areas that reflect recovery expectations. | Sector leadership can reflect positioning, valuation, or temporary flows. | Leadership narrows, reverses, or fails to broaden across risk assets. |

| Commodities or inflation-sensitive assets | Demand-sensitive assets may respond to expected nominal recovery. | Commodities can rise because of supply shocks or geopolitical pressure. | Commodity strength raises input costs without improving real demand. |

| Credit conditions | Functional credit can support the recovery interpretation. | Calm credit does not prove recovery by itself. | Credit spreads widen, funding stress rises, or lenders become more cautious. |

| Policy pressure | Supportive or manageable policy expectations can help reflation pricing. | Stimulus does not automatically create durable reflation. | Inflation overshoot forces tighter policy or reduces the policy support impulse. |

| Risk appetite breadth | Broad participation can support the reflation interpretation. | Risk appetite can be driven by liquidity, positioning, or sentiment alone. | Participation becomes narrow, speculative, or unsupported by macro improvement. |

Reflation Trade vs Reflation Policy vs Inflation Trade vs Stagflation

| Concept | Core meaning | Starting condition | What confirms it | Common mistake |

|---|---|---|---|---|

| Reflation trade | Market behavior tied to expectations of recovering growth and inflation from weak conditions. | Weak growth, disinflation, downturn risk, or depressed nominal expectations. | Multiple channels align: growth expectations, inflation expectations, credit, yields, cyclicals, and risk appetite. | Treating one asset move as proof that reflation is real. |

| Reflation policy | Policy action intended to lift demand, prices, or nominal growth. | Weak demand, deflation risk, recession pressure, or below-target inflation. | Policy works through demand, credit, spending, incomes, and inflation expectations. | Assuming policy intent automatically produces market reflation. |

| Inflation trade | Market behavior linked mainly to rising inflation or inflation protection demand. | Inflation pressure, inflation fear, or repricing of purchasing-power risk. | Inflation-sensitive assets or inflation expectations respond, often with attention to real yields. | Treating all inflation-sensitive moves as healthy reflation. |

| Stagflation | A regime where inflation pressure persists while growth weakens. | Weak or slowing growth with stubborn inflation pressure. | Growth deteriorates while inflation remains elevated or sticky. | Confusing inflation pressure with recovery. |

How Markets Often Express Reflation Expectations

Markets often express reflation expectations through relative behavior rather than one isolated signal. Cyclical sectors may outperform defensive areas if investors expect stronger demand. Financials may respond if yield curves steepen and loan-growth expectations improve. Commodities may rise if stronger activity is expected to lift demand. Small caps and value-sensitive areas may improve if investors expect a broader recovery rather than narrow defensive leadership.

Bond markets can also participate. Nominal yields may rise if investors expect stronger growth and inflation. Breakeven inflation measures may move if markets price higher inflation expectations. Curve behavior can become relevant when investors expect short-term policy to remain supportive while longer-term growth and inflation expectations improve.

These signals need context. Higher yields can support a reflation interpretation when they reflect improving nominal growth, but they can become a headwind if they tighten financial conditions too quickly. Commodity strength can support the theme when demand is improving, but it can contradict the theme when supply pressure raises costs without improving real activity. Cyclical leadership can be useful, but it becomes less reliable if credit conditions are deteriorating.

The interpretation becomes stronger when several channels point in the same direction instead of relying on one asset move.

Why a Reflation Trade Can Be Misleading

A reflation trade can be misleading when the market prices recovery faster than the economy confirms it. Markets often move ahead of data, which means the label can appear before the macro regime is durable.

One asset move is not enough. Rising commodities, higher yields, or stronger cyclicals can each appear for reasons that are not reflation. Supply shocks, positioning, fiscal expectations, risk-premium changes, and temporary sentiment shifts can all create similar surface behavior.

Inflation overshoot can also damage the reflation interpretation. A moderate rise in inflation expectations from depressed levels may support the idea of recovering nominal demand. Persistent or excessive inflation pressure can create a different problem by increasing policy-tightening risk, pressuring margins, and weakening real income.

Credit conditions are another boundary. A reflation label is less convincing if credit spreads widen, funding stress rises, or lenders become more cautious. Healthy reflation usually requires a functional credit backdrop. Credit stress can turn the same market environment into a more fragile risk regime.

The theme can also become priced in. If markets already reflect optimistic recovery expectations, later data may need to exceed that pricing to keep the trade alive. A correct macro direction can still produce poor market behavior if the expectation was already crowded or fully discounted.

Illustrative Scenario

A weak economic backdrop develops after a period of slowing demand and falling inflation pressure. Policy expectations shift toward support, and markets begin to price the possibility that nominal growth will recover over the next several quarters.

Cyclical areas start outperforming defensive areas, long-term yields rise, inflation expectations move up from low levels, and commodities strengthen. At first, those moves may look like a reflation trade.

The interpretation remains incomplete, though. If credit spreads stay calm, breadth improves, and forward growth indicators begin to recover, the reflation reading becomes more coherent. If credit stress rises, inflation pressure comes mainly from supply constraints, or higher yields begin tightening financial conditions, the same surface pattern becomes less reliable.

The useful distinction is expectation versus realization. Markets can price reflation before the economy confirms it, but the label remains provisional until the condition stack improves beyond one or two visible signals.

How to Interpret the Label Safely

A reflation trade is best treated as a macro-regime label, not as a mechanical signal. It can help describe the environment markets are trying to price, but it does not decide positioning on its own.

The strongest use of the concept is diagnostic. The label asks whether growth expectations, inflation expectations, policy conditions, credit, yields, commodities, sector leadership, and risk appetite are telling a consistent story. If they are, reflation pricing may be more defensible. If they are not, the label may be hiding a weaker or more conflicted environment.

The main boundary is that reflation is a recovery concept. Inflation without growth is not reflation in the same sense. Persistent inflation with weak growth moves the discussion closer to stagflation. Falling inflation pressure with stable growth points toward a different macro environment. The distinction is clearer when viewed through reflation versus stagflation, because the key question is whether inflation pressure comes with improving growth or weakening growth.

FAQ

What is a reflation trade?

A reflation trade is market behavior linked to expectations that growth and inflation are recovering from a weak or disinflationary starting point.

Is a reflation trade the same as reflation policy?

No. Reflation policy is an action intended to support demand, prices, or nominal growth. A reflation trade is how markets price the expectation that those conditions may improve.

Is a reflation trade the same as an inflation trade?

No. An inflation trade is mainly linked to inflation pressure or inflation protection. A reflation trade usually requires improving growth expectations as well.

What can make a reflation trade misleading?

It can be misleading when one asset move is treated as confirmation, when credit weakens, when inflation overshoots, or when markets price recovery faster than the economy confirms it.

Does a reflation trade mean markets will rise?

No. A reflation trade does not guarantee broad market gains. Some assets may respond positively to recovery expectations while others may be pressured by higher yields, policy repricing, or weaker margins.