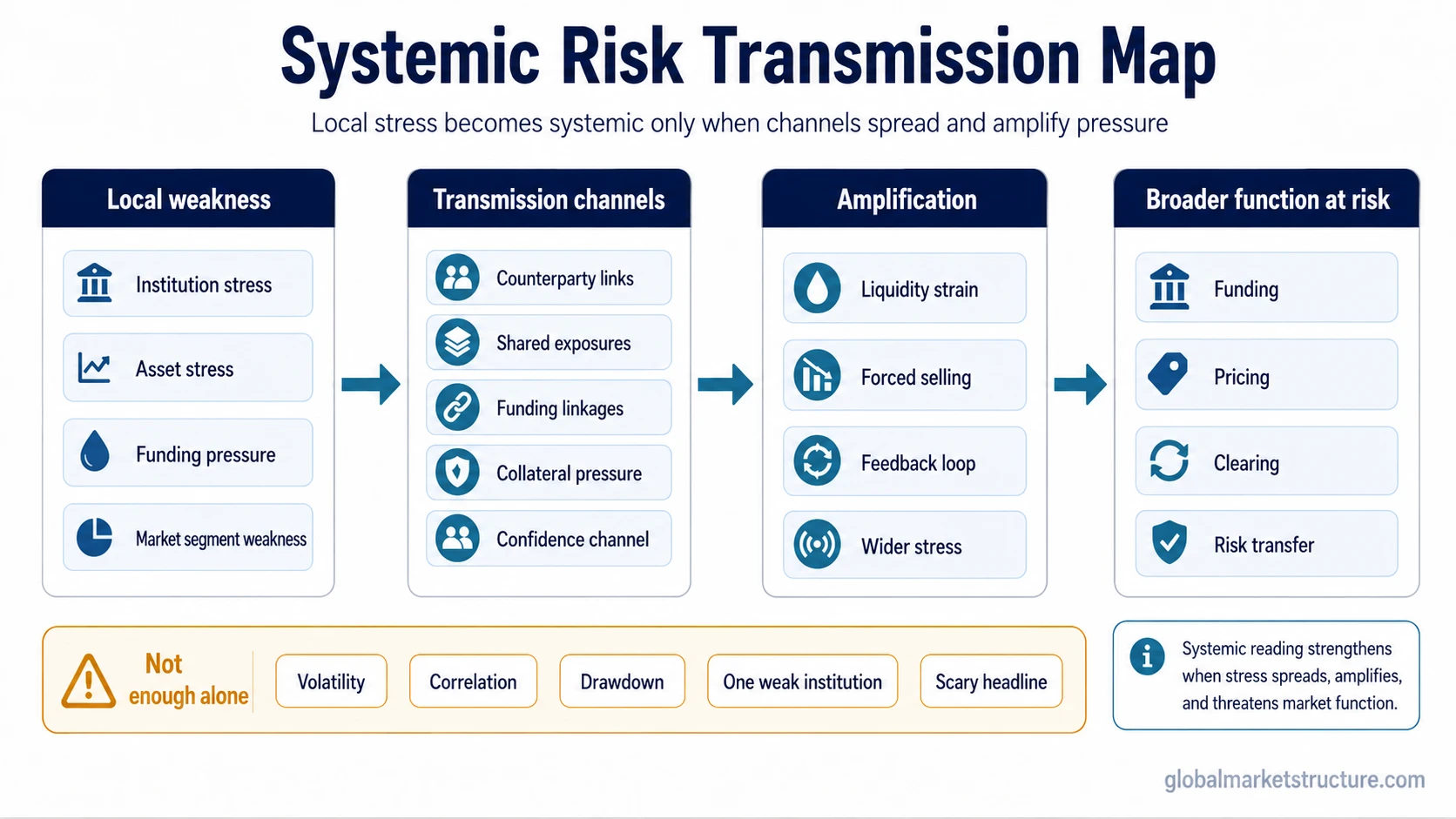

Systemic risk in finance is the risk that stress in one institution, asset, funding channel, or market segment can transmit and amplify across the financial system. It becomes systemic when linkages, liquidity strain, funding pressure, collateral pressure, confidence loss, or forced selling threaten broader market function. Volatility, correlation, a drawdown, one weak institution, or a scary headline is not enough by itself, and the label is not automatically a financial crisis, crash forecast, or portfolio instruction.

Definition: Systemic risk is system-level financial fragility. It describes the risk that localized stress can spread through market, funding, liquidity, confidence, collateral, or balance-sheet channels until broader financial-system function is at risk.

The useful boundary is not whether conditions look uncomfortable. The boundary is whether stress can move beyond its starting point and create amplification across other participants, markets, or funding channels.

What Makes Risk Systemic

A local shock becomes more relevant to systemic risk when it gains a transmission path. The original weakness may start in one balance sheet, asset class, lender group, or market segment, but the concern rises if other participants are exposed through funding, collateral, counterparty, liquidity, or confidence channels.

- Local weakness appears. Stress begins in one institution, market segment, asset type, or funding channel.

- Interlinkages expose others. Counterparties, lenders, investors, or related markets become sensitive to the same weakness.

- Liquidity or funding pressure rises. Participants may find it harder to borrow, roll funding, trade without price impact, or maintain collateral.

- Confidence, collateral pressure, or forced selling develops. The problem can begin feeding on itself instead of staying contained.

- Stress amplifies into broader financial conditions. The label becomes more relevant when the system’s ability to fund, price, clear, or transfer risk is threatened.

That transmission path is related to financial contagion, but the two terms are not identical. Contagion describes how stress spreads; systemic risk describes the broader fragility that can make that spread dangerous for financial-system functioning.

Systemic Risk Is Not Just Market Stress

Systemic risk is often over-applied when markets are volatile or prices are falling. Those conditions can matter, but they do not prove system-level fragility unless there is evidence of transmission and amplification through financial channels.

| Observed stress | When it may become systemic | Why it is not enough alone |

|---|---|---|

| Higher volatility | Volatility spreads through funding, liquidity, collateral, confidence, or forced-selling channels. | Volatility can reflect repricing, uncertainty, or positioning without broader system impairment. |

| Rising correlations | Correlated losses interact with leverage, funding pressure, shared exposures, or collateral stress. | Correlations often rise during ordinary risk-off behavior without becoming systemic. |

| A drawdown | Falling prices impair collateral, force sales, or damage market functioning. | A drawdown can remain a price decline rather than a financial-system fragility event. |

| One institution under stress | Counterparty, funding, payment, confidence, or collateral channels transmit the stress outward. | A single institution can weaken or fail while the broader system remains able to absorb the shock. |

| Defensive market behavior | Multiple channels show stress amplification across financial conditions. | Risk-off behavior alone is not proof of systemic risk. |

A Short Systemic Risk Scenario

A funding-dependent institution loses confidence from lenders. At first, the weakness is local: one balance sheet is under pressure, and nearby asset prices adjust.

The systemic-risk reading becomes more relevant if counterparties reduce exposure, short-term funding tightens, collateral requirements rise, and other participants sell liquid assets to meet obligations. If that forced selling becomes a fire sale, price declines can create feedback that pressures additional balance sheets.

That reading weakens if funding lines remain available, counterparties absorb losses, market depth holds, and the stress does not move into broader financial conditions. The point is not whether prices fell; it is whether the financial system begins transmitting and amplifying the stress.

Systemic Risk, Contagion, Fire Sales, and Systematic Risk

Systemic risk is the system-level fragility condition. Financial contagion is one way stress can travel. A fire sale is one forced-selling feedback mechanism that can intensify stress. A drawdown is a price decline, and volatility is movement around price.

Systematic risk is different again. It refers to broad market-wide exposure that diversification cannot easily remove, not the same thing as system-level failure risk. The difference between systemic and systematic risk matters because the words sound similar but point to different market problems.

Keeping those boundaries clear prevents one weak signal from being upgraded into a system-level conclusion. Systemic risk needs evidence that stress can spread, amplify, and threaten broader financial-system function.

Evidence That Strengthens a Systemic-Risk Reading

A conservative reading looks for evidence across channels rather than one alarming market move. Relevant areas can include interconnections, shared exposures, leverage, short-term funding reliance, market depth, collateral sensitivity, and confidence signals.

None of those inputs is decisive alone. The reading becomes stronger when several channels deteriorate together and stress begins to affect how markets fund, price, clear, or transfer risk.

What to Watch Before Using the Label

The systemic-risk label is strongest when the evidence points beyond isolated weakness. The core test is whether stress can move through transmission channels, amplify under liquidity or funding pressure, and threaten broader market functioning.

If the evidence shows only volatility, correlation, a drawdown, or one contained failure, the systemic-risk label is too strong. Those conditions may still matter, but they do not carry the same meaning as system-level fragility.