Financial contagion is the transmission and amplification of financial stress across markets, institutions, countries, financial networks, liquidity channels, funding channels, or balance sheets. It can appear when an initial shock spreads through exposures, funding pressure, forced selling, or risk repricing. Volatility, correlation, or a drawdown alone does not prove contagion because the key issue is whether stress is actually propagating across channels.

Financial contagion is about spread, not just movement. Two markets can fall together because they share the same macro driver, the same rate shock, or the same risk-appetite shift. Contagion becomes a stronger interpretation only when stress appears to move through a transmission path and affect areas beyond the original source.

Key Points

- Financial contagion describes stress transmission and amplification across financial channels.

- Correlation, volatility, or a market decline can be evidence to investigate, but none proves contagion by itself.

- A drawdown measures loss depth, while contagion describes how stress spreads.

- Systemic risk is related, but not every contagion episode becomes a system-wide crisis.

- Contagion readings become more credible when several channels point to the same stress pattern.

What Financial Contagion Describes

Financial contagion describes a transmission process. A stress event in one market, institution, region, funding channel, or balance-sheet structure can affect other parts of the financial system through direct and indirect links.

The link can be mechanical, such as counterparty exposure or common holdings. It can be liquidity-driven, such as forced selling after funding conditions tighten. It can also be behavioral, as investors reduce risk across markets after reassessing losses, leverage, or uncertainty.

The important boundary is that contagion requires more than simultaneous price movement. Normal interdependence can make markets move together without a distinct propagation process. A common macro shock can also pressure several assets at once without proving that stress traveled from one part of the system into another.

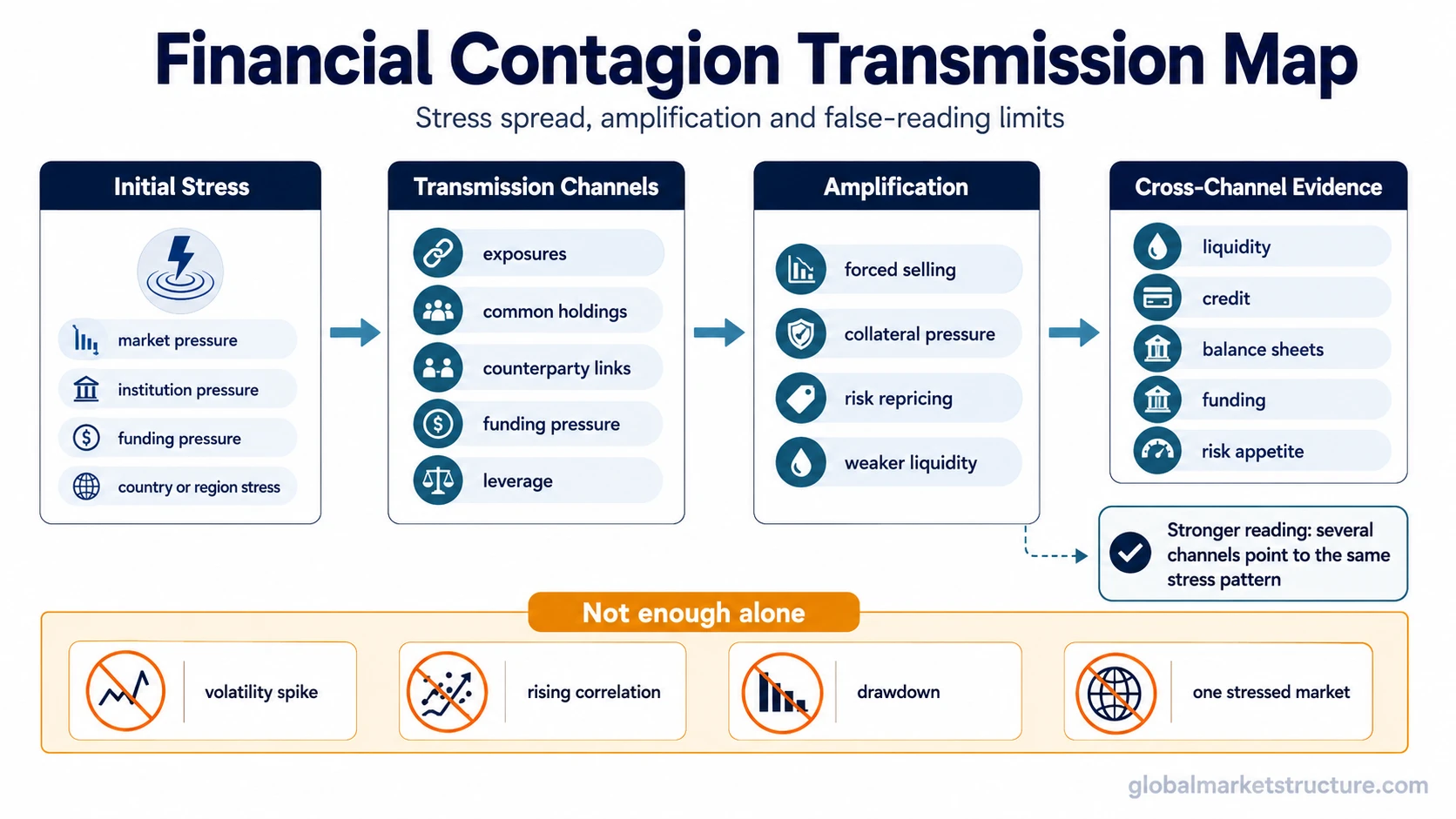

How Financial Contagion Can Spread

Financial contagion can spread when an initial stress point meets a channel that carries pressure into other markets or balance sheets. The channel matters because it separates contagion from a simple selloff or broad risk repricing.

| Stage | What can happen | Why it matters |

|---|---|---|

| Initial stress | A market, institution, country, asset class, or funding channel comes under pressure. | The first shock creates the starting point, but not enough evidence for contagion by itself. |

| Transmission channel | Stress moves through direct exposures, common holdings, funding pressure, counterparty links, leverage, or information gaps. | The channel explains how pressure can leave the original source. |

| Amplification | Forced selling, collateral pressure, risk repricing, or liquidity deterioration can increase the scale of the move. | Amplification makes the stress broader than the initial shock. |

| Cross-channel evidence | Pressure appears across more than one market, institution type, funding condition, or risk measure. | Multiple channels reduce the risk of mistaking ordinary co-movement for contagion. |

| Interpretation limit | The evidence still needs context from liquidity, credit, correlation, volatility, funding, and balance-sheet conditions. | No single indicator can carry the whole conclusion. |

Some contagion channels are direct, such as losses moving through counterparties or shared balance-sheet exposures. Others are indirect, such as investors selling unrelated assets because funding becomes harder, margin pressure rises, or risk appetite deteriorates across markets.

Financial Contagion vs Related Concepts

Financial contagion sits near several crisis-dynamics concepts, but the terms do different jobs. The distinction matters because a market can show losses, volatility, or cross-asset weakness without proving that contagion is spreading.

| Concept | What it describes | What it does not prove |

|---|---|---|

| Financial contagion | Transmission or amplification of stress across financial channels, markets, institutions, countries, networks, or balance sheets. | It does not by itself prove a crash, system-wide failure, or required portfolio action. |

| Drawdown | Loss depth from a prior peak. | It does not prove that stress is spreading across markets, institutions, or balance sheets. |

| Systemic risk | Fragility that can threaten the functioning of the wider financial system. | It is related to contagion, but not every contagion episode becomes a systemic crisis. |

| Common shock or interdependence | Markets moving together because they share macro drivers, normal linkages, policy pressure, or broad risk repricing. | It does not automatically prove stress transmission from one financial channel into another. |

| Funding or liquidity stress | Pressure in financing conditions, trading depth, collateral, or market functioning. | It can be a channel for contagion, but it is not identical to contagion. |

When Contagion Is a False Reading

False reading: A volatility spike can reflect uncertainty, positioning, event risk, or repricing without proving that stress is transmitting across financial channels.

False reading: Rising correlation can come from a common macro shock or normal interdependence rather than contagion.

False reading: A broad market decline can be a drawdown without clear evidence that stress is spreading through funding, liquidity, counterparty, or balance-sheet channels.

False reading: A single market under pressure does not prove contagion unless the stress spreads beyond the original source.

False reading: Contagion and systemic risk are connected concepts, but contagion does not automatically mean the financial system is failing.

A more careful interpretation treats contagion as an evidence-supported reading, not a label for every selloff. Price movement can start the question, but the answer depends on whether the stress is moving through identifiable channels.

Financial Contagion Example in Context

A common situation begins with stress in one funding-sensitive market. Prices fall, risk appetite deteriorates, and leveraged participants start reducing exposure. The first decline alone is not enough to call contagion.

The contagion reading becomes more credible if stress appears in related funding markets, liquidity becomes thinner, credit risk begins repricing, and other assets with shared exposures come under pressure. The reading weakens if the move remains isolated, trading conditions stay orderly, and related markets do not show funding, liquidity, or balance-sheet pressure.

The practical distinction is transmission. A contained loss can be painful without becoming contagion. A smaller initial shock can become more important if it exposes leverage, shared holdings, funding dependence, or counterparty links that spread pressure into other areas.

Why Confirmation Across Channels Matters

Financial contagion is easier to overstate when the evidence comes from one visible market indicator. Volatility can rise quickly, correlations can change during stress, and drawdowns can become severe. Those conditions may be warning signs, but they still need confirmation from transmission channels.

Confirmation becomes stronger when several forms of evidence point in the same direction. Examples include funding pressure, weaker liquidity, forced selling, wider risk spreads, balance-sheet stress, counterparty concerns, and deteriorating risk appetite across more than one market. The combination matters more than any single input.

Risk appetite is part of the interpretation because contagion often involves repricing beyond the original source of stress. When investors reduce exposure across unrelated assets only because one area is under pressure, the pattern may reflect broader fear, funding constraint, or balance-sheet protection. That still requires channel evidence before the label becomes credible.

How Financial Contagion Fits Inside Crisis Dynamics

Financial contagion belongs inside crisis dynamics because it explains how stress can move from one part of the financial system into another. It is not the same as a normal market decline, and it is not automatically the same as system-wide failure.

A drawdown can occur during contagion, but the drawdown itself only measures the loss from a prior peak. Systemic risk can rise when contagion reaches critical institutions, funding markets, or balance-sheet structures, but contagion can also remain limited if the stress stops spreading.

The strongest use of the concept is boundary-aware. Financial contagion describes propagation, amplification, and stress transfer. It should not be used as a shortcut for crash prediction, portfolio action, or any conclusion based on one indicator alone.