Drawdown means a decline from a prior peak to a later trough in a price, index, portfolio, strategy, or other financial variable. In market-risk analysis, drawdown describes loss depth, time under water, and the recovery path after stress appears. It does not, by itself, forecast a crash or prove systemic stress. The interpretation becomes stronger when credit, liquidity, breadth, volatility, funding pressure, and contagion conditions confirm the decline.

What drawdown means

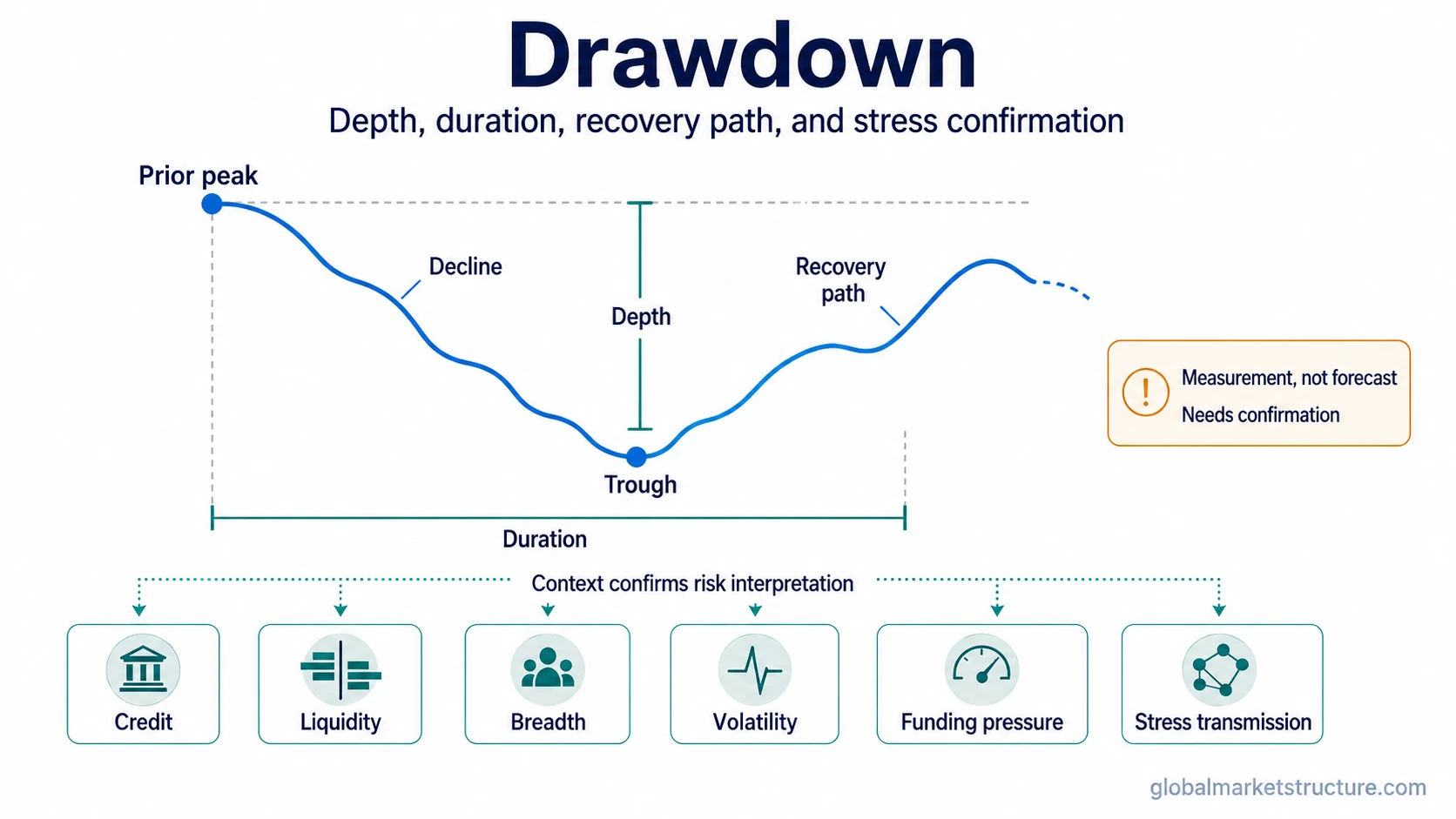

A drawdown measures how far a market variable falls from a previous high before a later low is reached. The prior high is the peak. The later low is the trough. The distance between them is the drawdown depth.

Drawdown is usually expressed as a percentage. If an index falls from 100 to 80 before recovering, the drawdown is 20%. The same logic can apply to a market index, an asset price, a portfolio value, a trading strategy, or a broader risk variable.

Maximum drawdown is the largest peak-to-trough decline measured over a defined period. It identifies the deepest observed decline inside that period, not the reason for the decline or what happens next.

Peak, trough, depth, duration, and recovery path

Drawdown has several parts. The peak is the prior high. The trough is the later low. Depth measures the size of the decline. Duration measures how long the variable remains below the prior peak. The recovery path describes how the market behaves after the trough has formed.

Depth and duration are different. A sharp 10% decline that recovers quickly carries different information from a 10% decline that remains unresolved for months. The percentage loss is the same, but the time under water and the market’s ability to absorb stress are not the same.

The recovery path matters because a drawdown can stabilize, grind sideways, recover quickly, or keep making lower recovery attempts. Those paths can suggest different levels of stress absorption, risk appetite, and liquidity support, but they still require confirmation from other market conditions.

How a drawdown develops

A drawdown starts after a prior high has formed. The market variable then declines until a trough is established. The trough is only known after the low has already appeared. Until then, the active decline is still unresolved.

After the trough, the recovery path determines whether the earlier peak is regained, partially regained, or remains distant. Duration continues until the variable returns to the prior peak. A drawdown can therefore be shallow but long, deep but brief, or deep and long at the same time.

Market-risk interpretation begins after the basic measurement is separated from the cause. A drawdown measures the decline. It does not automatically explain whether the decline came from valuation repricing, liquidity withdrawal, credit stress, forced selling, weakening breadth, or broader stress transmission.

Drawdown dimensions

| Drawdown dimension | What it measures | What it does not prove |

|---|---|---|

| Depth | The percentage decline from the prior peak to the later trough. | It does not prove why the decline happened. |

| Duration | The time spent below the prior peak. | It does not prove that stress is systemic. |

| Recovery path | The way the market behaves after the trough. | It does not guarantee a full recovery or a renewed decline. |

| Maximum drawdown | The largest peak-to-trough decline over a defined period. | It does not forecast future returns. |

| Confirmation context | The surrounding credit, liquidity, breadth, volatility, funding, and contagion conditions. | It does not turn drawdown into a standalone signal. |

Drawdown versus loss, volatility, contagion, and other meanings

Drawdown versus realized loss: A drawdown can exist before a position or portfolio loss is realized. A market value may be below its prior peak even if nothing has been sold. A realized loss requires an actual exit or accounting recognition, depending on the context.

Drawdown versus volatility: Volatility measures variability or fluctuation. Drawdown measures decline from peak to trough. A market can be volatile without being in a large drawdown, and it can remain in a drawdown even after volatility has cooled.

Drawdown versus financial contagion: Drawdown describes the observed decline. financial-contagion describes stress transmission across assets, institutions, regions, or funding channels. The decline may be visible before the transmission mechanism is clear.

Drawdown versus forced selling: A drawdown does not automatically prove forced liquidation. A fire-sale requires selling pressure under liquidity stress, often with price impact that reflects urgency rather than normal repricing.

Drawdown versus systemic risk: Systemic risk involves broader fragility across the financial system. Drawdown can be one symptom of stress, but it does not prove system-level instability without additional evidence.

Drawdown versus retirement drawdown: In retirement planning, drawdown can refer to withdrawing savings or portfolio assets over time. Market-risk drawdown is different: it measures the decline from a prior high to a later low.

Drawdown versus credit-line drawdown: In lending, drawdown can mean using part of an approved credit facility. Market drawdown does not describe borrowing activity; it describes the path from peak value to trough value.

Drawdown versus climate drawdown: Climate drawdown refers to reducing atmospheric greenhouse gas levels. Financial drawdown is a market-risk measurement, not a climate or environmental term.

Why the same drawdown can mean different things

A 12% equity-index drawdown can carry different risk information under different conditions. If credit spreads remain contained, liquidity is still functioning, breadth is not collapsing, and volatility is controlled, the decline may reflect normal repricing or a contained risk reset.

The same 12% drawdown becomes more serious when credit conditions deteriorate, liquidity weakens, market breadth narrows, volatility expands, funding pressure rises, and stress begins moving across connected markets. Under those conditions, drawdown becomes part of a broader stress picture rather than a simple percentage decline.

The useful distinction is conditional. Drawdown provides the observed loss path. Credit, liquidity, breadth, funding, volatility, and contagion conditions help judge whether the decline is isolated, absorbed, or spreading through the market structure.

Practical scenario

Consider two broad equity indices that each fall 15% from prior highs. In the first scenario, credit spreads remain stable, liquidity conditions are orderly, market breadth weakens only modestly, and the index recovers steadily. The drawdown still matters, but the surrounding evidence points toward contained repricing rather than broad stress.

In the second scenario, the same 15% decline appears alongside widening credit spreads, weaker liquidity, thin breadth, rising volatility, funding pressure, and signs of stress transmission across markets. The drawdown percentage is identical, but the risk environment is different because the decline is now confirmed by adjacent stress indicators.

What drawdown cannot prove by itself

Drawdown is an important risk measure, but it is not a forecast. It does not automatically predict a crash, recession, recovery failure, systemic event, or future return path.

Drawdown is also not a trading instruction. A deeper decline does not automatically mean buy, sell, hedge, reduce exposure, or hold cash. Those actions depend on strategy, mandate, time horizon, risk controls, liquidity needs, and evidence beyond the drawdown itself.

The strongest use of drawdown is diagnostic. It helps describe how much stress has appeared, how long the market has remained below its prior high, and whether recovery behavior is being confirmed or contradicted by the surrounding risk environment.

Key Points

- Drawdown measures a peak-to-trough decline from a prior high to a later low.

- Maximum drawdown is the largest drawdown observed over a defined period.

- Depth, duration, and recovery path provide different information.

- Drawdown is not the same as volatility or a realized loss.

- Drawdown alone does not prove contagion, forced selling, systemic risk, or a crash forecast.

- Market-risk interpretation becomes stronger when drawdown is confirmed by credit, liquidity, breadth, volatility, funding pressure, and stress-transmission conditions.

FAQ

What is drawdown in finance?

Drawdown is the decline from a prior peak to a later trough in a price, index, portfolio, strategy, or other financial variable. It measures how far the value falls before a low is established.

What is maximum drawdown?

Maximum drawdown is the largest peak-to-trough decline measured over a defined period. It identifies the deepest observed decline in that period, not the cause of the decline or the future path.

Is drawdown the same as volatility?

No. Volatility measures fluctuation or variability. Drawdown measures decline from peak to trough. A market can be volatile without a large drawdown, and a market can remain below a prior peak even after volatility falls.

Does drawdown predict a market crash?

No. Drawdown does not predict a crash by itself. It becomes more informative when the decline is confirmed by weaker credit, liquidity, breadth, funding, volatility, or stress-transmission conditions.