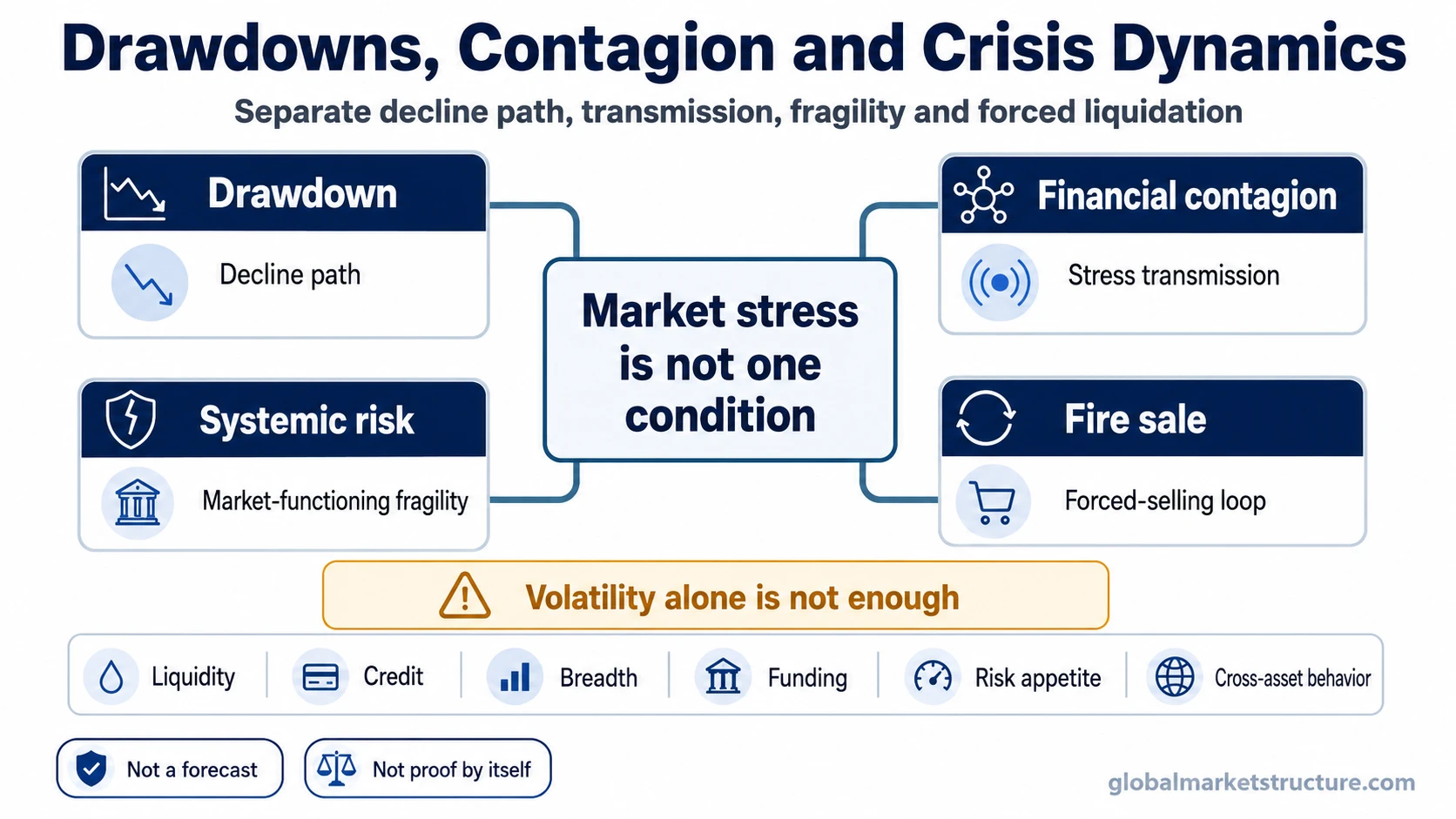

Drawdowns, contagion, and crisis dynamics describe different layers of market stress. A drawdown tracks the decline itself, financial contagion describes how stress spreads, systemic risk asks whether market functioning is threatened, and fire-sale dynamics show how forced selling can intensify pressure. Volatility alone does not confirm a crisis environment.

These concepts belong together because market stress is not one condition. A falling market, a spillover across assets, a liquidity-driven selling loop, and a broader threat to market functioning can overlap, but they do not mean the same thing.

How to choose the right stress concept

The useful question is not only whether markets are under pressure. The useful question is what kind of pressure is being observed: decline path, transmission, system-wide fragility, or forced liquidation.

| Stress question | Correct concept | What it explains | What it does not prove by itself |

|---|---|---|---|

| How large is the decline, how long has it lasted, and what is the recovery path? | Drawdown | The depth, duration, and path of a market decline from a prior high. | It does not automatically explain why stress is spreading or whether the financial system is unstable. |

| Is stress spreading across markets, institutions, regions, or balance sheets? | Financial contagion | The transmission of stress from one market, asset class, or institution to another. | It does not automatically mean the entire system is failing. |

| Could market functioning, funding stability, or balance-sheet confidence be threatened? | Systemic risk | The risk that stress becomes broad enough to threaten normal financial-system functioning. | It does not follow from every selloff or every volatility spike. |

| Is forced selling creating a feedback loop through leverage, collateral, or poor liquidity? | Fire sale | The forced-liquidation process that can push prices lower when participants must sell into weak liquidity. | It does not describe the whole crisis environment unless the selling loop connects to wider stress. |

How the stress question changes the interpretation

Drawdown: Use this concept when the main issue is the size of the decline, the time spent below a prior high, the recovery path, or the experience of loss from peak to trough.

Financial contagion: Use this concept when the main issue is spillover. The stress may begin in one market, institution, funding channel, or region, then move through balance-sheet exposure, correlation, confidence, or liquidity pressure.

Systemic risk: Use this concept when the main issue is whether stress can threaten market functioning or broader financial stability. The question is larger than price decline alone.

Fire sale: Use this concept when forced selling, collateral pressure, leverage, and thin liquidity create a feedback loop. The selling itself can become part of the stress mechanism.

One stress signal is not enough

A volatility spike can occur without confirming systemic stress. A drawdown can be painful without becoming contagion. Contagion can remain local before it becomes systemic. Fire-sale pressure becomes more serious when liquidity, leverage, and forced selling interact.

Stronger market-stress interpretation usually needs confirmation across several areas: risk appetite, credit conditions, liquidity, market breadth, funding pressure, and cross-asset behavior. The point is not to force one label onto every selloff, but to identify which stress mechanism is actually visible.

Where the concepts overlap

A broad equity decline may begin as a drawdown. The question changes if credit conditions deteriorate, liquidity weakens, and stress starts moving across assets or institutions. If selling pressure becomes forced and self-reinforcing, fire-sale mechanics may become part of the interpretation. If the stress begins to threaten market functioning, the discussion moves closer to systemic risk.

The labels are connected, but they should stay separate. Drawdown describes the decline path. Financial contagion describes transmission. Systemic risk describes wider fragility. Fire sale describes forced-selling mechanics.

Neighboring concepts should not be treated as interchangeable

Drawdown is not contagion: a market can fall sharply without stress spreading through other markets or institutions.

Contagion is not automatically systemic risk: stress can spread across connected areas before it threatens the broader financial system.

Systemic risk is broader than a decline: it asks whether the functioning of markets, funding channels, or balance sheets is being threatened.

Fire-sale pressure is a mechanism, not the whole crisis: forced selling can intensify stress, but the wider environment depends on liquidity, leverage, credit, and cross-asset confirmation.

Use these concepts as a stress map

Market stress is easier to interpret when the first step is classification. Start with the question being asked: decline path, stress transmission, systemic fragility, or forced liquidation. Then move into the concept that explains that layer directly.