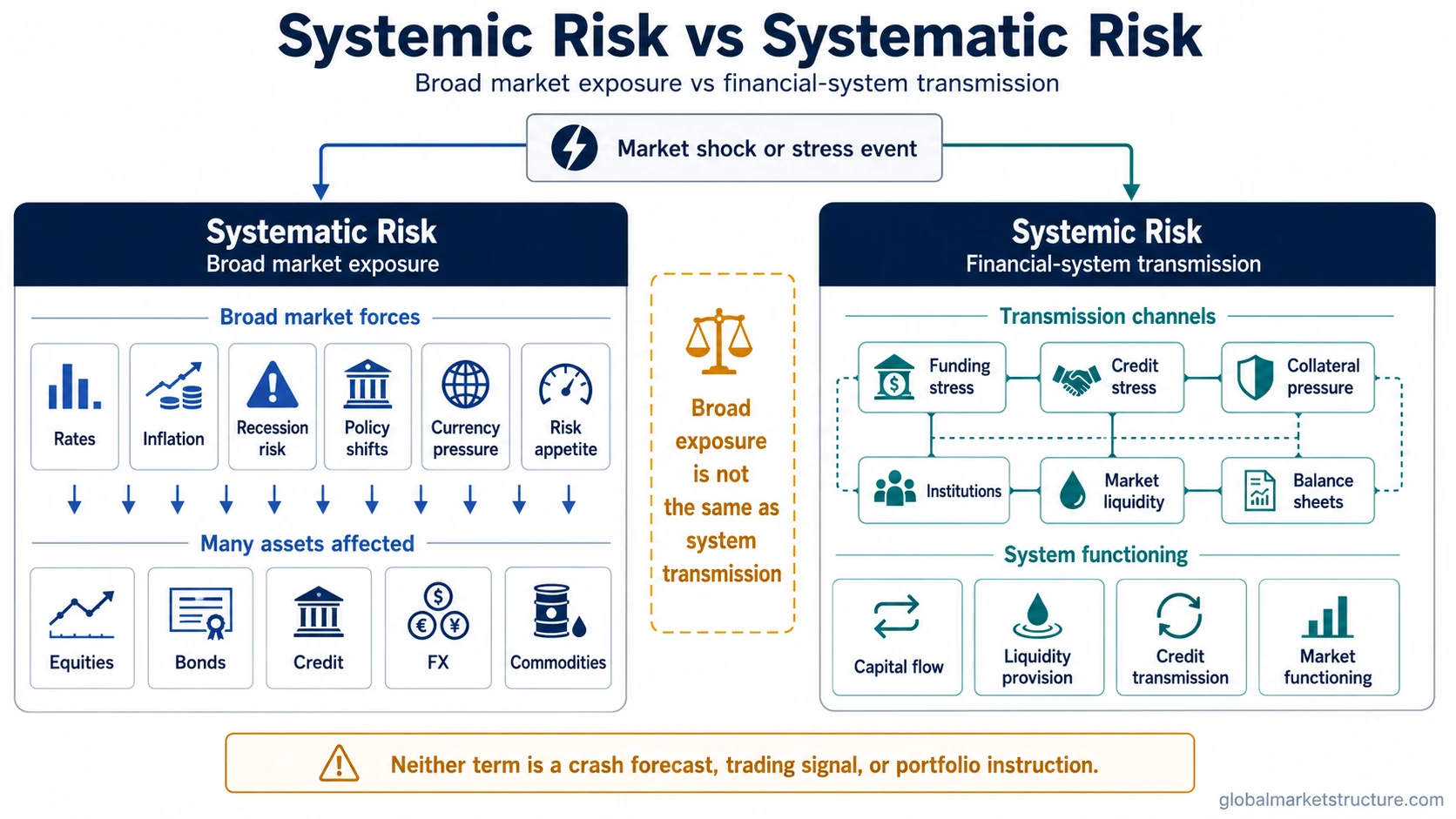

Systemic risk and systematic risk describe different layers of financial risk. Systemic risk is about stress that can spread through the financial system and impair how the system functions. Systematic risk is about broad market exposure that affects many assets and cannot be diversified away within the same market.

The useful test is direct: systemic risk asks whether stress can transmit through institutions, funding markets, credit channels, balance sheets, or market plumbing. Systematic risk asks whether the exposure comes from market-wide forces such as rates, inflation, recession risk, policy shifts, or broad risk appetite.

Key Points

- Systemic risk is about financial-system transmission, contagion paths, institutional links, funding stress, and possible impairment of system functioning.

- Systematic risk is broad market exposure caused by economy-wide or market-wide forces that affect many assets at once.

- A large selloff can be systematic without being systemic if markets continue functioning and stress does not spread through the financial system.

- The distinction is classification, not a crash forecast, trading signal, or portfolio instruction.

Systemic Risk vs Systematic Risk: Core Comparison

| Criterion | Systemic risk | Systematic risk |

|---|---|---|

| Core question | Can stress spread through the financial system and impair system functioning? | Is this broad market exposure affecting many assets? |

| Main concept | System stability and transmission risk | Non-diversifiable market risk |

| Main mechanism | Contagion, institutional failure, funding stress, credit stress, balance-sheet links, and market plumbing stress | Macro shocks, rates, inflation, recession risk, policy shifts, and broad risk appetite |

| Scope | Financial system, networks, institutions, markets, and balance sheets | Broad market or asset-class exposure |

| Diversification relevance | Diversification may not protect if the system itself is impaired | Diversification within the same market cannot fully remove it |

| Common mistake | Calling every large selloff systemic | Treating broad market risk as if it were firm-specific risk |

| Best market-structure lens | Stress transmission and market-functioning lens | Broad exposure and macro-factor sensitivity lens |

The Core Difference

Systemic risk describes the possibility that stress in one part of the financial system can spread widely enough to damage system functioning. The focus is not only the size of the loss. The focus is transmission.

A localized failure, a liquidity squeeze, or a credit event becomes more relevant to systemic risk when it can move through connected institutions, balance sheets, funding markets, collateral chains, or payment and settlement channels. The question is whether the system can still absorb stress, allocate capital, provide liquidity, and process transactions without broader dysfunction.

Systematic risk describes broad exposure to market-wide forces. It is the risk that remains when many securities or assets are affected by the same macro or market factor. A recession shock, inflation repricing, interest-rate move, policy surprise, or general risk-off shift can affect a large share of the market at once.

The important boundary is that systematic risk is broad, but it is not automatically systemic. A market can fall because discount rates rise, earnings expectations weaken, or risk appetite contracts. That can be systematic risk even if the financial system continues functioning normally.

When a Risk Is Systemic

The systemic label fits when damage can propagate through the structure of the financial system. The mechanism matters more than the headline.

Systemic risk becomes a stronger interpretation when stress appears in several connected places at once: funding pressure, credit-market deterioration, collateral strain, forced deleveraging, impaired market liquidity, or pressure on key intermediaries. These are transmission channels, not just price moves.

A bank failure, fund failure, or institutional loss is not automatically systemic. The risk becomes systemic only if the stress threatens wider system functioning or creates a credible path of contagion through other institutions, markets, or funding channels.

Systemic-risk language should be used carefully. A sharp price decline can be severe without being systemic. A single institution can fail without destabilizing the broader system. The systemic label belongs to transmission risk, not to every large loss.

When a Risk Is Systematic

The systematic label fits when risk comes from broad market exposure. The source is usually a factor that affects many assets at the same time rather than a problem isolated to one company, one issuer, or one balance sheet.

Examples include changes in interest rates, inflation expectations, recession risk, broad earnings risk, policy uncertainty, currency pressure, or a general decline in risk appetite. These forces can affect many securities together because they change discount rates, expected growth, liquidity preferences, or required returns.

Systematic risk is often discussed as the risk that cannot be removed simply by diversifying across securities within the same market. A portfolio can reduce company-specific exposure, but it cannot fully remove the shared exposure that comes from broad market conditions.

That does not make systematic risk a prediction tool. It does not say when a market will fall, how far it will fall, or when it will recover. It only describes a type of broad exposure.

Same Scenario, Different Risk Layer

A broad equity market selloff after a recession shock can be systematic risk for equity exposure. Many stocks may decline together because the same macro factor affects earnings expectations, discount rates, credit conditions, and risk appetite.

That same selloff becomes systemic only if stress begins to threaten financial-system functioning. The interpretation changes if the selloff is accompanied by funding stress, collateral pressure, forced deleveraging, credit-market dysfunction, impaired dealer balance sheets, bank stress, or a breakdown in market liquidity.

The same price decline can be systematic before it becomes systemic. A falling index does not prove system failure. The systemic reading requires evidence that stress is transmitting through the financial system in a way that weakens its ability to function.

Common Mistakes When Comparing the Two Terms

A large market decline is not automatically systemic risk. Size alone does not prove transmission.

A single institution failure is not automatically systemic. The systemic question is whether the failure spreads through wider financial connections.

Systematic risk is not the same as unsystematic risk. Systematic risk is broad market exposure. Unsystematic risk is more specific to a company, issuer, sector, or idiosyncratic event.

Systematic risk is not a system-collapse label. It can describe ordinary broad market exposure even when markets continue functioning.

Systemic-risk language is not a standalone crash forecast. It should not be used as a substitute for evidence from credit stress, funding pressure, contagion channels, liquidity withdrawal, or balance-sheet transmission.

Neither term is a market-timing signal. The distinction helps classify risk, not decide what to buy, sell, hedge, or short.

Why the Distinction Matters for Market Structure

The distinction matters because the two terms answer different analytical questions during market stress.

Systematic risk asks whether broad exposure is being repriced across a market. It is useful for understanding why many assets can move together when macro conditions change.

Systemic risk asks whether the financial system itself is becoming a transmission channel. It is useful for interpreting whether stress is spreading through funding, credit, liquidity, collateral, institutions, or market plumbing.

A broad selloff, a drawdown, or a risk-off move can reflect systematic risk without proving systemic stress. The systemic interpretation becomes stronger only when price declines are joined by evidence of transmission, dysfunction, or impaired market functioning.

Clean distinction: systematic risk is exposure to broad market forces; systemic risk is the risk that stress spreads through the financial system itself.

FAQ

Are systemic risk and systematic risk the same thing?

No. Systemic risk concerns financial-system transmission and possible impairment of system functioning. Systematic risk concerns broad market exposure that affects many assets and cannot be diversified away within the same market.

Can the same event create both systemic and systematic risk?

Yes. A macro shock can create systematic risk by affecting broad market exposure. It can also become systemic if the shock spreads through funding markets, credit channels, institutions, balance sheets, or market plumbing.

Is every market crash a systemic-risk event?

No. A crash or large decline can be systematic without being systemic. The systemic label requires evidence of transmission or dysfunction inside the financial system, not just falling prices.

How is systematic risk different from unsystematic risk?

Systematic risk is broad market risk that affects many assets. Unsystematic risk is specific to a company, issuer, sector, or idiosyncratic event and can often be reduced through diversification.