Market stress is a market-environment condition in which liquidity, credit, volatility, funding pressure, safe-haven demand or risk appetite begin to show strain together. It is broader than a volatility spike and narrower than a full crisis. One indicator alone is not enough to confirm it.

Key Points

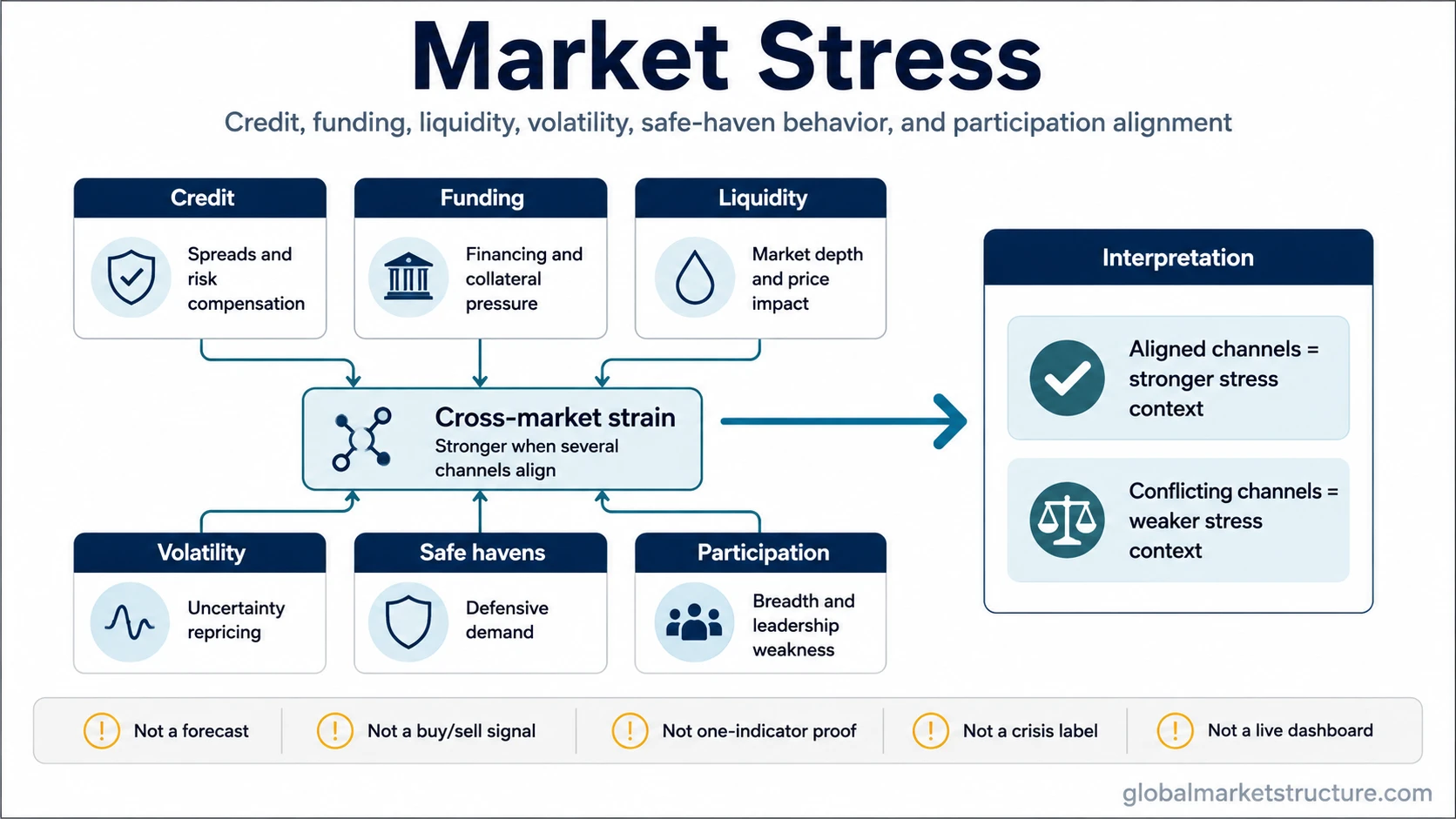

- Market stress describes strain across market functioning, risk pricing and participant behavior.

- It becomes more meaningful when several channels deteriorate at the same time.

- Volatility, VIX, credit spreads, liquidity and safe-haven demand can support the reading, but none of them defines market stress alone.

- Market stress is not a forecast, not a buy/sell signal and not automatically a financial crisis.

What Is Market Stress?

Market stress is a condition where normal risk pricing becomes less stable and market participants begin to demand more protection, liquidity or compensation for uncertainty. It can appear when investors reduce risk exposure, credit markets demand higher spreads, funding becomes harder, liquidity weakens or volatility reprices quickly.

The useful distinction is that market stress is not only a price move. A sharp decline in one asset can be noise, repricing or position adjustment. Stress becomes more credible when the strain appears across several channels at once and changes how participants behave.

Core limitation: market stress is a context condition, not a standalone signal. A VIX move, a volatility spike, a credit-spread move or a stress-index reading can contribute to the interpretation, but none of them proves market stress by itself.

How Market Stress Shows Up Across Markets

Market stress often becomes easier to identify through alignment. A single warning sign may be temporary. Several warning signs moving together can show that the market environment is becoming less resilient.

- Credit channel: spreads may widen as investors demand more compensation for default, downgrade or liquidity risk.

- Funding channel: borrowing, collateral or short-term financing conditions may become less comfortable for leveraged participants.

- Liquidity channel: markets may become harder to trade without larger price impact, especially in thinner or more crowded areas.

- Volatility channel: realized and implied volatility may rise as uncertainty is repriced.

- Safe-haven channel: demand may shift toward assets perceived as more defensive, although that behavior is not always uniform.

- Participation channel: market breadth may weaken if fewer assets or sectors continue to support the index-level move.

This is why market stress should be read as a multi-channel condition. The interpretation becomes stronger when volatility, credit, liquidity, funding and participation tell a similar story. It becomes weaker when one channel looks stressed while the broader system remains orderly.

Market Stress vs Similar Concepts

Market stress overlaps with several related terms, but it should not be collapsed into any one of them. The distinction matters because each concept answers a different question.

| Concept | What It Mainly Describes | Why It Is Not the Same as Market Stress |

|---|---|---|

| Market stress | Strain across market functioning, risk pricing, liquidity and participant behavior. | This is the broader context condition being evaluated. |

| Market volatility | The size or speed of price movement. | Volatility can rise without broader liquidity, credit or funding strain. |

| VIX | Option-implied volatility expectations for the S&P 500. | The VIX can support a stress reading, but it is not a full cross-market stress measure. |

| Financial conditions | The broad ease or tightness of financing, rates, credit and market variables. | Financial conditions can be tight or easy without every market showing acute stress. |

| Risk appetite | The willingness of investors to hold risky assets. | Weak risk appetite can accompany stress, but it can also reflect ordinary caution or valuation adjustment. |

| Systemic risk | The risk that distress spreads through the financial system. | Market stress can exist without becoming systemic. The distinction is closer to systemic risk vs systematic risk. |

| Financial crisis | A severe breakdown in financial stability, confidence or market functioning. | Stress can increase crisis risk, but stress is not the same as a crisis. |

Why One Indicator Is Not Enough

A single indicator can identify pressure in one part of the system, but market stress is a broader interpretation. A volatility spike may reflect a scheduled event. Wider credit spreads may reflect sector-specific concern. A stress index may rise because one component moved sharply while other channels remain calm.

The better question is whether the signal is isolated or confirmed by related evidence. Market stress becomes more credible when credit risk, funding pressure, liquidity deterioration, defensive demand and volatility repricing appear together. It becomes less credible when the evidence conflicts.

Interpretation rule: one indicator can start the question, but cross-market alignment carries more weight than a single reading.

Official or institutional data endpoints can help measure financial stress, but the concept layer still comes first: the channels, boundaries and limitations matter before any data series is treated as complete proof.

A Practical Scenario

One practical scenario: equity volatility rises while credit spreads begin widening, safe-haven demand becomes more visible, liquidity becomes thinner and market breadth weakens. None of those signals alone proves a market-stress regime. Together, they may show that investors are repricing uncertainty across several channels rather than reacting to one isolated headline.

The reading remains conditional. If credit markets stabilize, liquidity stays orderly and participation broadens again, the same volatility move may look more like temporary repricing than durable market stress.

How To Interpret Market Stress Without Treating It as a Signal

Market stress is most useful as a context filter. It can help explain why price moves become larger, why liquidity disappears more quickly, why risk premiums rise or why defensive behavior becomes more visible. It does not tell the reader what to buy, sell or predict.

For example, a widening gap between implied and realized risk can make the volatility risk premium more relevant to the interpretation, but that still does not turn stress into a directional market call. It only shows that the cost of uncertainty and protection may be changing.

The cleanest use of the concept is to separate environment from action. Market stress describes the condition of the market backdrop. Any decision process still requires separate evidence, risk controls and time-horizon context.

Common Interpretation Mistakes

- Equating stress with a crash: stress can exist without an immediate collapse.

- Using VIX alone: implied volatility is useful, but it is not the whole market structure.

- Ignoring liquidity: price movement can look manageable until liquidity disappears.

- Confusing stress with systemic risk: not every stressed market condition threatens the financial system.

- Turning context into a signal: market stress describes conditions, not a direct trade instruction.

FAQ

Is market stress the same as volatility?

No. Volatility describes the size or speed of price movement. Market stress is broader because it can include liquidity, credit, funding pressure, safe-haven demand and changes in participant behavior.

Does a high VIX confirm market stress?

No. A high or rising VIX can support a market-stress interpretation, but it does not confirm stress by itself. The reading becomes more meaningful when other channels also show strain.

Is market stress the same as tight financial conditions?

No. Tight financial conditions can contribute to stress, but market stress focuses on how strain appears in market functioning, risk pricing, liquidity and behavior.

Does market stress predict a crash?

No. Market stress is not a crash forecast. It describes a weaker or more fragile market environment, and the interpretation depends on the surrounding evidence.

Can one indicator measure market stress?

One indicator can highlight pressure, but it should not be treated as complete proof. Market stress is more credible when several independent channels point in the same direction.