A business-cycle peak is the high point of an economic expansion before activity begins to contract. It is an economic turning-point label, not a stock-market top, recession forecast, allocation rule, or trade signal.

The label is used to describe a broad shift in the business cycle after evidence shows that expansion has stopped rising and contraction has begun. That evidence usually comes from several measures of economic activity rather than from one market chart, one indicator, or one weak data release.

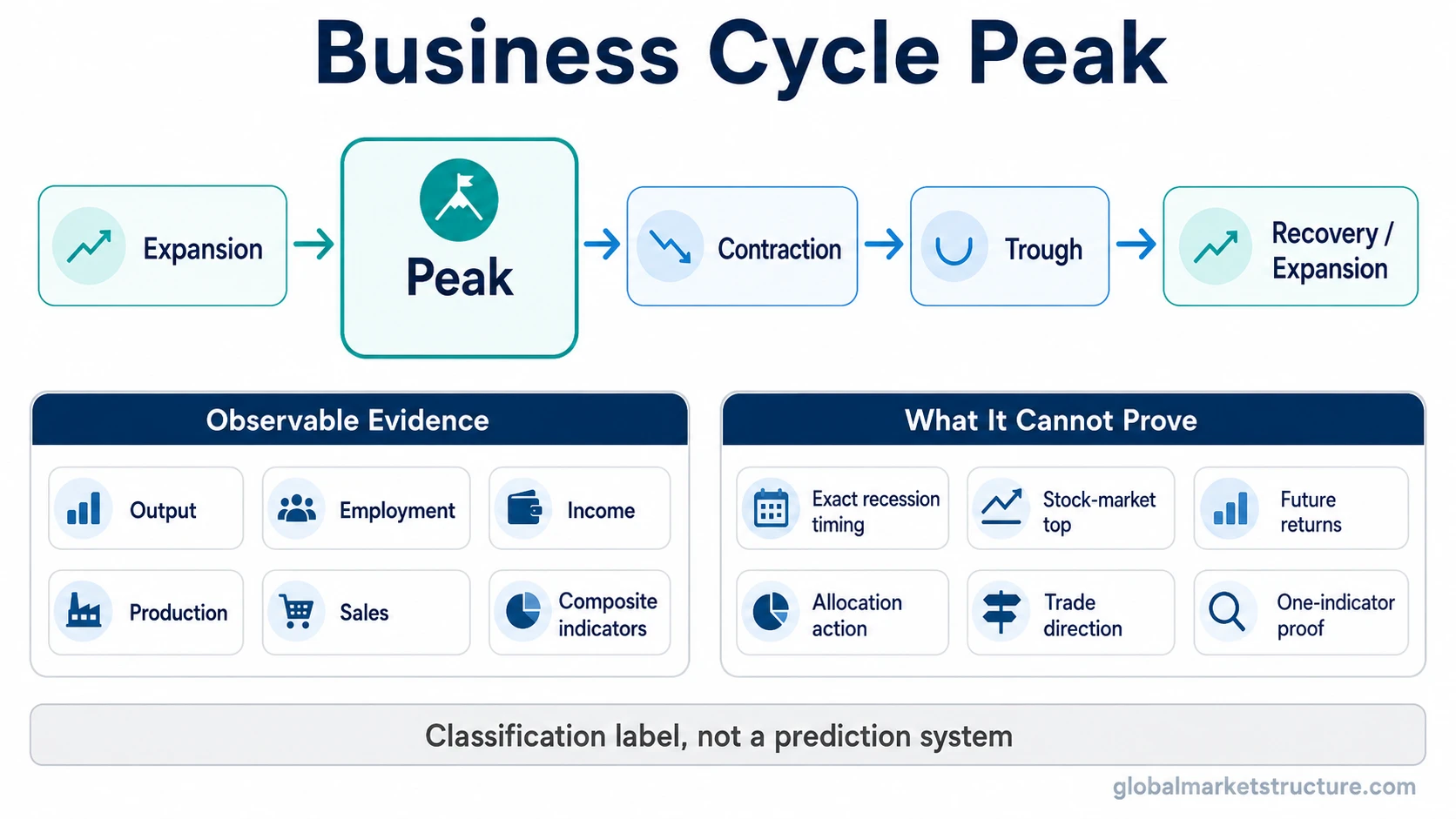

Simple definition: a business-cycle peak marks the transition from expansion to contraction in broad economic activity.

What Is a Business-Cycle Peak?

A business-cycle peak is the point where an economy reaches the top of an expansion phase before moving into contraction. The concept belongs to economic-cycle analysis, so it focuses on broad activity such as output, employment, income, production, and sales.

The peak does not mean that every part of the economy turns down at the same moment. Some areas may weaken earlier, some may lag, and some may remain strong for a period. The label becomes more useful when several economic measures begin to support the same broad turning-point interpretation.

This is why a business-cycle peak is different from a single disappointing data point. One weak release can be noise, revision risk, or sector-specific pressure. A peak classification needs a broader pattern that suggests the expansion phase has ended.

Where a Peak Sits in the Business Cycle

The business cycle is usually described as a sequence of expansion, peak, contraction, trough, and recovery. The peak sits between expansion and contraction. It marks the point where broad economic activity stops rising and the next phase begins to weaken.

The same sequence also explains why a peak should not be read as a complete forecast. A peak describes where the economy is classified within the cycle after enough evidence is reviewed. It does not specify the exact depth, duration, or market effect of the contraction that may follow.

For broader context, the business cycle is the parent concept that explains the full expansion and contraction sequence. A peak is one turning point inside that larger framework.

Evidence That May Support a Peak Classification

A peak classification is stronger when several areas of economic activity begin to align. The exact evidence set can vary, but the useful question is whether weakness is broad enough to suggest a turning point rather than a temporary slowdown.

| Evidence area | What it can show | Why one measure is not enough |

|---|---|---|

| Output | Whether real economic activity is still expanding or has begun to weaken. | Output data can be revised and may not capture every sector at the same time. |

| Employment | Whether labor-market strength is still supporting expansion. | Employment can lag other activity and may remain firm after earlier weakness appears. |

| Income | Whether household and business income conditions still support demand. | Income measures can be uneven across sectors and may not turn at the same pace. |

| Production | Whether industrial or productive activity is slowing beyond one narrow area. | Production weakness can reflect sector pressure rather than a full-cycle turn. |

| Sales | Whether demand is weakening across goods, services, or business activity. | Sales can be affected by prices, inventory cycles, and temporary distortions. |

| Composite indicators | Whether multiple measures point toward the same cycle interpretation. | Composite signals still need context and should not be treated as automatic proof. |

What a Business-Cycle Peak Does Not Prove

A business-cycle peak is often misunderstood because the word “peak” sounds precise. In practice, the label does not prove exact timing, market direction, or the severity of what comes next.

- It does not prove a stock-market top. Financial markets can turn before, during, or after economic-cycle turning points.

- It does not forecast future returns. The label describes a cycle phase, not a return model.

- It does not confirm exact recession timing. A peak may be identified only after enough evidence has accumulated.

- It does not create an allocation rule. Portfolio decisions require separate risk, valuation, liquidity, and mandate analysis.

- It does not provide trade direction. A cycle label is not an entry, exit, stop, target, or signal.

- It does not depend on one indicator alone. A single weak signal can support investigation, but it cannot carry the classification by itself.

Business-Cycle Peak vs Market Top

A business-cycle peak is an economic label. A market top is an asset-price event. The two can be related, but they are not the same thing.

Equity markets, credit markets, rates, commodities, and currencies may all react differently around cycle transitions. Some markets try to discount weakness before the economic data turns. Others respond later as earnings, credit conditions, or liquidity change. That timing difference is why a business-cycle peak should not be converted into a market-timing claim.

| Concept | What it describes | Common mistake |

|---|---|---|

| Business-cycle peak | The high point of broad economic expansion before contraction. | Assuming it automatically identifies the top in asset prices. |

| Market top | A high point in a financial asset, index, sector, or market segment. | Assuming price weakness alone proves the economic cycle has peaked. |

| Recession start | The beginning of a sustained decline in broad economic activity. | Assuming a recession can be precisely known from one early signal. |

Why Peak Identification Can Be Delayed

Business-cycle turning points are usually clearer after the fact than in real time. Data can be revised, indicators can conflict, and different areas of the economy can turn at different speeds.

A real-time observer may see slowing growth, weakening production, softer sales, tighter credit, or lower confidence before the broader classification is clear. Those signals can raise the question of whether the economy is near a peak, but they do not automatically settle the answer.

This delay is not a flaw in the concept. It is part of the reason the concept should be treated as classification rather than prediction. A peak label becomes more reliable when it is supported by a broader evidence set, but that also means it may not arrive at the earliest possible moment.

How a Peak Differs From a Slowdown

A slowdown means growth is weakening. A business-cycle peak means the expansion phase has reached its high point and the economy has moved into contraction. The distinction matters because a slowdown can occur inside an ongoing expansion without becoming a full turning point.

A temporary slowdown may reflect inventory adjustment, policy uncertainty, sector weakness, price effects, or external shocks. A peak classification requires a stronger interpretation: broad economic activity has stopped expanding and the next phase has begun.

| Label | Basic meaning | Interpretation boundary |

|---|---|---|

| Slowdown | Growth continues but at a weaker pace. | Does not necessarily end the expansion. |

| Peak | The expansion reaches its high point before contraction. | Requires broader evidence than one weak indicator. |

| Contraction | Economic activity declines after the peak. | Depth and duration still need separate analysis. |

| Trough | The contraction reaches its low point before recovery. | Does not prove the strength of the next expansion. |

Practical Scenario

A practical scenario is that production growth weakens first, sales soften next, and income or employment data remain firmer for a while. In that situation, the economy may look mixed rather than clearly contracting. The peak question becomes more serious if the weakness spreads across multiple measures instead of staying isolated in one sector.

The useful interpretation is not that one early signal “calls the peak.” The useful interpretation is that the evidence set needs to be watched as a sequence. A broad turning-point label becomes more defensible when several parts of the economy begin to confirm the same direction.

Related Cycle Concepts

A business-cycle peak is easier to understand when it is separated from adjacent cycle labels. These concepts belong to the same cycle family, but each answers a different question.

| Concept | Question it answers | How it relates to a peak |

|---|---|---|

| Expansion | Is broad economic activity rising? | The peak comes at the high point of the expansion phase. |

| Contraction | Is broad economic activity declining? | Contraction follows the peak in the cycle sequence. |

| Business-cycle trough | Where does contraction stop before recovery begins? | A trough is the opposite turning point from a peak. |

| Recession | Has broad economic activity contracted meaningfully? | A peak may precede recession classification, but it does not by itself forecast severity. |

| Business-cycle stages | How do the main phases fit together? | Peak is one stage boundary inside the full cycle sequence. |

Business Cycle Peak FAQ

What does business-cycle peak mean?

A business-cycle peak means the economy has reached the high point of an expansion before broad activity begins to contract. It is a cycle classification label, not a market-timing signal.

Is a business-cycle peak the same as a recession?

No. A peak is the turning point from expansion into contraction. A recession describes a broader decline in economic activity. The peak can mark the transition, but the recession label requires separate evidence.

Does a business-cycle peak mean stocks have topped?

No. A business-cycle peak and a stock-market top are different concepts. Asset prices can move before, during, or after economic-cycle turning points, so the economic label should not be treated as a stock-market top signal.

Can one indicator prove a business-cycle peak?

No. One indicator can raise concern or support further review, but a peak classification is stronger when several measures of economic activity point toward the same broad turning-point interpretation.