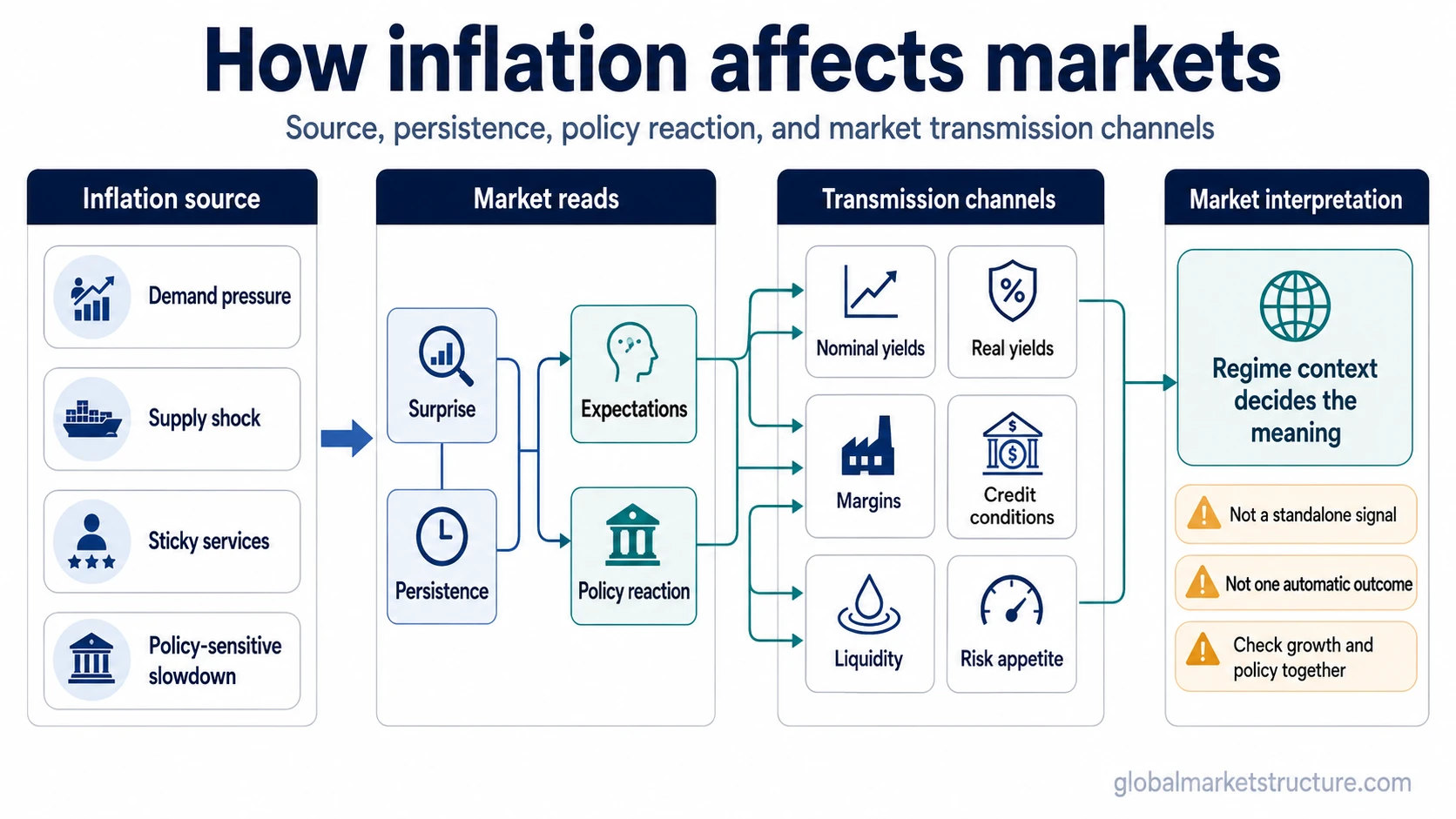

Inflation affects markets through several channels at once: growth expectations, central-bank policy, nominal yields, real yields, company costs, profit margins, inflation expectations, and risk appetite. The same inflation rate can mean different things depending on whether it comes from strong demand, supply pressure, sticky services prices, or a policy-sensitive slowdown. Inflation is a market driver, not a standalone market signal.

Markets react less to the word “inflation” than to what inflation changes. A higher inflation reading can alter expected policy rates, bond yields, discount rates, earnings pressure, currency pressure, and the price investors are willing to pay for future cash flows. The market impact depends on context: where the inflation came from, whether it surprised investors, how persistent it appears, and how central banks are likely to respond.

This is why inflation can create different market outcomes across different regimes. Demand-led inflation can appear alongside firm nominal growth. Supply-driven inflation can squeeze margins. Sticky inflation can keep policy tight for longer. Falling inflation can support risk appetite if growth holds, but it can also signal weaker demand if the slowdown is broad.

The main channels from inflation to markets

The cleanest way to understand inflation’s market impact is to separate the transmission channels. Inflation can affect the economy directly through costs and purchasing power, but it also affects financial markets through expectations, rates, valuation, and risk appetite.

The first channel is growth and demand. When inflation comes from strong demand, markets may initially read it as evidence that nominal activity is still firm. When inflation comes from a supply shock, the same price pressure can feel more negative because costs rise without the same support from real demand.

The second channel is policy. Central banks respond to inflation because persistent inflation can threaten price stability. That policy reaction can influence short-term rates, the yield curve, credit conditions, and liquidity. For market interpretation, monetary policy often matters as much as the inflation number itself.

The third channel is yields. Inflation can push nominal yields higher if investors demand more compensation for future price increases. What matters for valuation, however, is often the inflation-adjusted return available to investors. Rising real yields can pressure long-duration assets because future cash flows are discounted at a higher real rate.

The fourth channel is expectations. Markets often react strongly when inflation changes what investors expect next, not only when current inflation changes. Inflation expectations influence wage behavior, policy expectations, bond pricing, and risk appetite.

The fifth channel is earnings. Inflation can lift nominal revenue in some industries, but it can also raise labor, input, financing, and inventory costs. The market impact depends on whether companies can pass those costs through without damaging demand. That is why profit margins are an important bridge between inflation data and equity-market interpretation.

Inflation channel routing table

Different market questions point to different inflation channels. A broad inflation reading is only the starting point. The more useful question is which part of the market transmission chain is changing.

| Reader question | Inflation channel | Market implication | Deeper concept |

|---|---|---|---|

| Why are yields moving after inflation data? | Nominal yields, policy expectations, and real yields | Bond markets may be repricing future inflation compensation, policy rates, or inflation-adjusted returns. | Real Yields, Monetary Policy |

| Why can stocks fall when inflation is high? | Discount rates, margin pressure, and policy tightening | Equity valuations can compress if real yields rise, costs pressure earnings, or policy becomes more restrictive. | Real Yields, Profit Margins, Monetary Policy |

| Why can markets react to inflation expectations? | Expected inflation and market-implied compensation | Markets may move when future inflation pricing changes, even before current inflation data fully changes. | Inflation Expectations, Breakeven Inflation |

| Why can inflation from supply shocks feel different? | Cost pressure and margin squeeze | Higher costs can hurt real purchasing power and company margins if demand does not rise at the same time. | Inflation, Profit Margins |

| Why does falling inflation not always mean risk-on? | Disinflation, growth weakness, and policy lag | Lower inflation can help if growth holds, but it can be negative if it reflects demand weakness or delayed policy pressure. | Disinflation, Monetary Policy |

Why the same inflation rate can mean different things

The same inflation rate can have different market meaning because markets care about the source, surprise, persistence, expectations, policy reaction, and growth mix behind the number.

Source matters. Inflation driven by firm demand can be read differently from inflation driven by energy, supply bottlenecks, rent, wages, or imported costs. Demand-led inflation may coincide with stronger nominal revenue, while supply-led inflation can pressure real incomes and company margins.

Surprise matters. Markets often price expected inflation before the data arrives. If inflation is already expected, the reaction can be muted. If the data surprises investors, the repricing can move through bonds, currencies, equities, and risk assets quickly.

Persistence matters. A one-off price jump is not the same as inflation that appears sticky across wages, services, housing, or repeated core categories. Persistent inflation can keep policy expectations tighter for longer and raise the hurdle for easier financial conditions.

Expectations matter. Market-implied measures such as breakeven inflation can show how investors price inflation compensation. They are useful market signals, but they can also include liquidity effects and risk premia, so they should not be treated as pure CPI forecasts.

Policy reaction matters. Inflation that changes the expected policy path can affect discount rates, credit conditions, and liquidity. Inflation that does not change the policy path may have a smaller market impact, especially if growth and earnings remain stable.

Growth mix matters. Markets usually prefer inflation that comes with resilient real growth over inflation that erodes purchasing power while growth slows. The difference is not only whether prices are rising, but whether incomes, demand, credit, and earnings can absorb the pressure.

How inflation can affect major market areas

Inflation affects major market areas through different channels. The result is conditional, not automatic.

Equities: Inflation can help nominal revenue in some areas, but it can pressure equities if margins compress, real yields rise, or policy tightens. Long-duration growth stocks can become more sensitive when discount rates rise, while companies with pricing power may be better able to defend margins.

Bonds: Inflation can pressure bond prices when investors demand higher yields to compensate for lost purchasing power or tighter policy. The key distinction is whether yields are rising because growth is strong, inflation compensation is rising, real yields are rising, or policy expectations are tightening.

Yields: Inflation can push nominal yields higher, but the market impact depends on the split between expected inflation and real yields. A move driven by higher real yields can affect valuations differently from a move driven mainly by inflation compensation.

Commodities: Inflation and commodities often interact, but the relationship is not mechanical. Some commodity price increases can contribute to inflation, while some inflation regimes can support commodity demand or hedging behavior. The interpretation changes if the move is supply-driven, demand-driven, or currency-driven.

Currencies: Inflation can affect currencies through real-rate differentials and policy expectations. A currency may strengthen if inflation leads to tighter policy and higher real returns, but it may weaken if inflation damages credibility, purchasing power, or external balances.

Risk assets: Inflation can influence risk appetite through liquidity, discount rates, earnings confidence, and policy uncertainty. Risk appetite usually becomes more fragile when inflation is persistent enough to limit policy flexibility while growth is slowing.

Common mistakes when interpreting inflation and markets

Inflation is easy to overread because it touches many market channels at once. The mistake is treating one channel as if it explains every market reaction.

| Mistake | Why it is incomplete | Better interpretation |

|---|---|---|

| Inflation is always bad for stocks. | Equities can respond differently depending on nominal growth, pricing power, margins, real yields, and policy. | Ask whether inflation is supporting revenue, squeezing margins, raising discount rates, or tightening liquidity. |

| Inflation automatically helps commodities. | Commodities can rise for supply reasons, demand reasons, currency reasons, or positioning reasons. | Separate the commodity driver from the inflation label before interpreting the move. |

| Falling inflation always means easier policy. | Policy may stay restrictive if inflation remains above target or if central banks need confidence that the slowdown is persistent. | Check inflation trend, growth conditions, labor conditions, and policy communication together. |

| Nominal yields explain everything. | Nominal yields combine inflation compensation and real-rate components. | Separate nominal yields from real yields and inflation expectations when interpreting asset prices. |

| Inflation data alone is a trading signal. | Inflation affects markets through many channels, and the same data can be interpreted differently across regimes. | Treat inflation as one macro driver inside a broader market structure, not as a standalone signal. |

| All inflation has the same market meaning. | Demand-led, supply-led, wage-led, imported, and policy-sensitive inflation can affect markets differently. | Identify the source and persistence of inflation before drawing market conclusions. |

A simple scenario framework

Inflation becomes easier to interpret when the scenario is separated from the number itself. These examples are illustrative, not historical market claims.

Demand-led inflation: If inflation is rising because demand is strong, markets may initially focus on resilient nominal growth and earnings. The risk is that policy may tighten if inflation looks persistent, which can later pressure rates, valuations, and credit conditions.

Supply-shock inflation: If inflation is rising because energy, freight, food, or other supply costs jump, the market impact can be more difficult. Companies may face higher input costs while consumers lose purchasing power. That can create margin pressure even if headline revenue looks firm.

Sticky inflation with tight policy: If inflation remains persistent while central banks are already restrictive, markets may worry that policy cannot ease quickly. In that environment, real yields, credit conditions, and liquidity can matter more than the inflation number alone.

Falling inflation with weak growth: Lower inflation can support markets if it allows easier policy while growth stays resilient. But falling inflation can be less positive if it reflects weak demand, falling pricing power, tighter credit, or earnings pressure.

Inflation is not a standalone market signal

Inflation matters because it changes growth expectations, policy reaction, yields, real yields, margins, liquidity, and risk appetite. It should not be treated as a standalone forecast, buy/sell signal, or portfolio instruction. The useful question is not simply whether inflation is high or low. The useful question is which transmission channel is changing and whether growth, policy, expectations, and earnings confirm the interpretation.

Where to go deeper

For the inflation channel itself, start with inflation. The core concept needs to be separated from market interpretation before the transmission channels become useful.

For why markets can react before inflation is fully visible in current data, focus on inflation expectations and breakeven inflation. Those concepts separate current price changes from expected future inflation and market-implied inflation compensation.

For why inflation can affect valuation, bond yields, and risk appetite, focus on real yields. The real-yield channel is often where inflation, policy, and asset pricing connect most directly.

For the policy reaction path, focus on monetary policy. Inflation affects markets partly because it changes how investors think central banks may respond.

For the corporate earnings channel, focus on profit margins. Inflation can raise nominal revenue in some cases, but the market impact depends on whether companies can protect margins after labor, input, financing, and operating costs rise.

FAQ

How does inflation affect markets?

Inflation affects markets through growth expectations, policy reaction, nominal yields, real yields, company costs, profit margins, inflation expectations, and risk appetite. The impact depends on the source, surprise, persistence, and policy response.

Is inflation always bad for stocks?

No. Inflation can pressure stocks when it raises discount rates, squeezes margins, or leads to tighter policy. But the effect can differ when nominal growth is strong, companies have pricing power, or markets already expected the inflation.

Why do bonds react to inflation?

Bonds react to inflation because inflation changes expected purchasing power, policy rates, and the compensation investors may require to hold fixed-income securities. Bond prices can fall when yields rise in response to inflation pressure.

Why can markets rise when inflation is high?

Markets can rise during high inflation if investors focus on strong nominal growth, resilient earnings, or inflation that is already priced in. The reaction depends on policy expectations, real yields, margins, and whether growth remains firm.

What matters more, inflation level or inflation expectations?

Both matter. The inflation level describes current price pressure, while inflation expectations influence policy pricing, bond yields, wage behavior, and risk appetite. Markets often react most when expectations change unexpectedly.