Economic nowcasting estimates the recent past, present, or very near-term state of economic activity before full official data are available. For market-structure interpretation, the estimate matters only after it changes expectations and interacts with cycle context, policy reaction, rates, DXY, credit, breadth, and leadership. A nowcast remains provisional, model-dependent, input-dependent, and not a market signal.

Official macro releases can arrive late, be revised, or describe a period that markets have already started to reprice. A nowcast can help frame the current economic growth backdrop, but it does not replace official data, cross-asset confirmation, or evidence from the broader cycle.

Key Points

- Economic nowcasting estimates current or near-term economic conditions before complete official releases are available.

- Nowcasting differs from forecasting because it focuses on the present or very near term, not a broad future projection.

- Market interpretation depends on expectations, cycle phase, policy/rates, DXY, credit, breadth, and leadership.

- Nowcasts can change as new data arrive, and revisions or model assumptions can weaken the reading.

- A nowcast is not a buy/sell signal, a recession label, or a complete macro regime call.

What Economic Nowcasting Estimates

Definition: Economic nowcasting is the process of estimating the current or very near-term state of an economic variable before the full official data set is available.

In growth analysis, nowcasting usually tries to close the gap between slow official releases and faster incoming evidence. That evidence may include surveys, labor data, spending measures, production indicators, financial conditions, and other high-frequency or mixed-frequency inputs.

The estimate is useful only when its scope is clear. A GDP-related nowcast, an inflation nowcast, and a labor-market nowcast may all update the current macro picture, but they can point to different parts of the economy. The interpretation depends on what is being estimated, which inputs changed, and whether other indicators confirm the same direction.

Official model boundary: Official nowcast tools and institutional models publish their own estimates. Those values should be used only when sourced and dated. The market-structure question is how changing estimates interact with expectations, policy reaction, liquidity, credit, breadth, and leadership context.

Nowcasting vs Forecasting vs Economic Surprise

Nowcasting, forecasting, and economic surprise answer different questions. Confusing them can turn a useful current-state estimate into an unsupported market prediction.

| Concept | Main question | Market-structure use | Common mistake |

|---|---|---|---|

| Economic nowcasting | What does current or very near-term activity likely look like before full official data arrive? | Frames the current growth backdrop and the direction of incoming evidence. | Treating the estimate as a direct market forecast. |

| Forecasting | What may happen over a future horizon? | Builds forward scenarios around growth, inflation, policy, and risk conditions. | Blending long-horizon projections with current-state measurement. |

| Official release data | What was reported by the official source for a defined period? | Creates a formal data point that markets compare against expectations. | Ignoring that official releases may be delayed, revised, or already partly anticipated. |

| Economic surprise | How did actual data compare with expectations? | The Economic Surprise Index helps separate the level of data from the expectations gap. | Assuming strong data matters the same way when it was already expected. |

A nowcast can improve while market reaction remains mixed if the improvement was already expected, if rates rise in response, or if credit and breadth fail to confirm the stronger activity reading.

Economic Nowcasting Framework For Market Interpretation

A macro market-structure reading treats economic nowcasting as one layer inside a broader signal stack. The estimate is the first input, not the conclusion.

| Framework input | What it updates | Market-structure interpretation | What weakens the reading | Related concept |

|---|---|---|---|---|

| Business activity inputs | Current production, services, orders, and sentiment direction. | Improving activity can support a firmer growth reading if it aligns with other evidence. | Survey strength without hard-data follow-through, falling demand, or weak new orders. | Purchasing Managers Index |

| Expectations gap | Whether incoming data are better or worse than what markets had priced. | A small nowcast change can matter if it resets expectations more than the level suggests. | Data improvement that was already anticipated or quickly revised away. | Economic Surprise Index |

| Cycle slack and capacity context | How far activity may be from sustainable capacity. | The same growth nowcast can mean resilience, overheating, or late-cycle pressure depending on slack. | Ignoring the output gap, inflation pressure, or policy sensitivity. | Output Gap |

| Labor confirmation | Whether employment conditions support or challenge the activity estimate. | Labor data can confirm resilience or reveal demand cooling beneath stronger headline activity. | One noisy labor print, seasonal distortion, or claims data that conflict with hiring strength. | initial jobless claims |

| Rates, DXY, credit, breadth, and leadership | Whether cross-asset behavior accepts the growth interpretation. | Confirmation improves when rates, dollar pressure, credit, breadth, and leadership respond coherently. | Higher rates tightening conditions, stronger DXY pressuring liquidity, weak credit, narrow breadth, or defensive leadership. | Cross-asset confirmation layer |

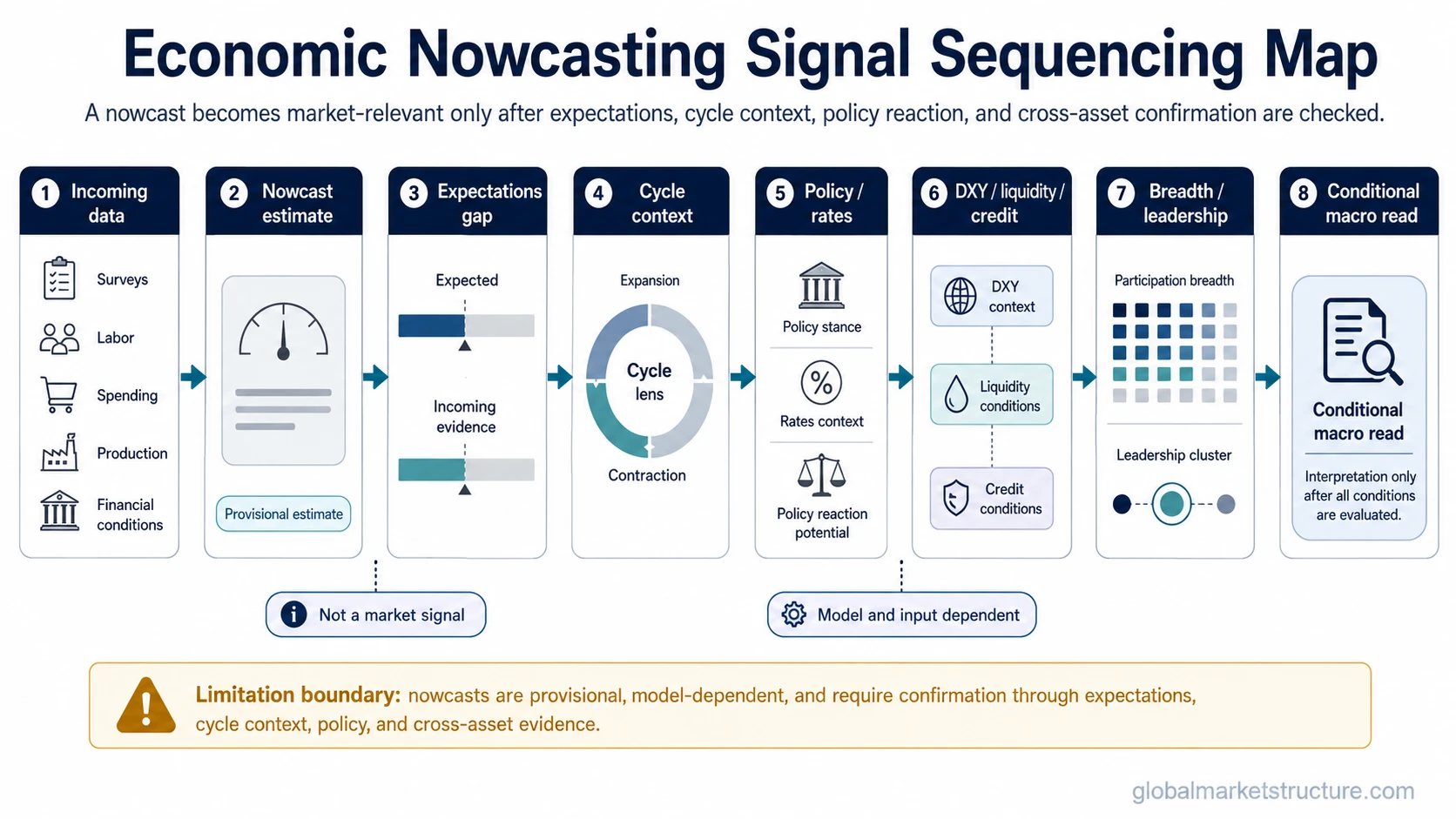

How To Sequence A Nowcast Reading

Economic nowcasting is most useful when the sequence is read in order. Jumping from a stronger estimate to a market conclusion creates the main interpretation risk.

| Sequence step | Question to ask | Interpretation use | Failure point |

|---|---|---|---|

| 1. Incoming data | Which high-frequency or mixed-frequency inputs changed? | Identifies the source of the nowcast movement. | The input is narrow, noisy, seasonal, or contradicted by other data. |

| 2. Nowcast estimate | Did the current-state estimate move enough to matter? | Frames whether the growth backdrop is strengthening, weakening, or staying mixed. | The change is within normal model noise or vulnerable to revision. |

| 3. Expectations gap | Was the change already expected? | Separates level from surprise, which often matters more for repricing. | Markets already priced the improvement or deterioration. |

| 4. Cycle context | Does stronger activity mean resilience, overheating, or policy pressure? | Prevents the same nowcast change from being read the same way in every regime. | Cycle phase, inflation pressure, or slack is ignored. |

| 5. Policy and rates reaction | Does the estimate change expected central-bank reaction or yield pressure? | Connects growth evidence to discount rates, real yields, and financial conditions. | Better growth tightens conditions enough to offset the activity signal. |

| 6. DXY, liquidity, credit, and breadth | Do cross-asset signals confirm the same interpretation? | Tests whether the growth reading is being accepted across market structure. | DXY strength, credit stress, weak breadth, or thin leadership challenges the read. |

| 7. Leadership response | Which areas lead, and does leadership match the growth interpretation? | Helps separate broad growth acceptance from narrow or defensive participation. | Leadership narrows, defensives outperform, or cyclicals fail to confirm. |

What Can Weaken A Nowcast Reading

A nowcast is not automatically stronger because it uses faster data. Faster data can also be noisy, incomplete, or sensitive to model assumptions.

Main limitation: A nowcast is an estimate conditioned by inputs, model design, data quality, and timing. It should be read as provisional evidence, not as a final macro verdict.

| Weakening factor | Why it matters | Safer interpretation |

|---|---|---|

| Data revisions | Early estimates can change when official data are revised or completed. | Treat the reading as current evidence, not final truth. |

| Model assumptions | Different models can weigh inputs differently and target different variables. | Compare the estimate with other macro and market evidence. |

| Noisy high-frequency inputs | Fast data can react to temporary distortions, seasonal effects, or narrow categories. | Look for repeated confirmation rather than one abrupt input change. |

| One-indicator overfit | One strong input can dominate the narrative even when the broader stack is mixed. | Check whether growth, labor, inflation, credit, and breadth agree. |

| Official release surprise | Formal releases can still differ from nowcast expectations. | Separate pre-release estimates from actual-versus-expected data. |

| Policy reaction mismatch | Better activity can raise rate expectations or tighten financial conditions. | Ask whether growth support outweighs the policy/rates response. |

| Cross-asset non-confirmation | Credit, breadth, DXY, or leadership may reject the growth interpretation. | Keep the read conditional until market structure confirms it. |

Economic Nowcasting Example in Context

Business activity data improve and a growth nowcast rises, but labor claims begin to soften and demand-sensitive indicators stop confirming the improvement. The first read is tempting: current activity appears more resilient than expected. The stronger case requires broader confirmation from rates, credit, breadth, DXY, and leadership.

If rates rise sharply because markets expect tighter policy, the improved growth estimate may not support risk appetite in a clean way. If credit remains calm, breadth expands, and leadership broadens beyond a narrow group, the interpretation becomes more coherent. If DXY strengthens, credit weakens, and leadership narrows, the nowcast improvement remains incomplete evidence rather than a regime conclusion.

The practical distinction is sequence. A nowcast can update the growth picture, but market-structure interpretation still depends on whether expectations, policy reaction, liquidity, credit, breadth, and leadership accept or challenge that update.

How Related Growth Inputs Fit

Economic nowcasting works best as a connector between several narrower growth and activity concepts. Each related input answers a different part of the interpretation problem.

| Growth input | What it clarifies | Boundary |

|---|---|---|

| Economic growth | Defines the broader real-activity backdrop that nowcasting tries to estimate earlier. | Growth is the macro concept; nowcasting is the current-estimation process. |

| Purchasing Managers Index | Adds a high-frequency business activity lens through survey-based evidence. | PMI can feed a nowcast, but it should not become the whole growth framework. |

| Economic Surprise Index | Separates actual data from what markets expected before the release. | Surprise logic explains repricing pressure, not the full level of activity. |

| Output gap | Places growth evidence against slack, capacity, inflation pressure, and cycle phase. | A similar growth estimate can carry different meaning depending on cycle position. |

| Initial jobless claims | Adds a labor confirmation lens that can support or challenge activity strength. | Claims data are one labor input, not a complete labor-market framework. |

FAQ

What is economic nowcasting?

Economic nowcasting estimates the current or very near-term state of an economic variable before full official data are available. It is used to interpret the present macro backdrop, not to predict market direction by itself.

How is nowcasting different from forecasting?

Nowcasting focuses on the recent past, present, or very near term, often before official data are complete. Forecasting projects future conditions over a broader horizon and usually depends on a wider scenario set.

Can a nowcast be treated as a market signal?

No. A nowcast is provisional evidence. Market interpretation depends on expectations, cycle context, policy reaction, rates, DXY, credit, breadth, and leadership confirmation.

Why can a nowcast change after new data arrive?

Nowcasts are model-dependent and input-dependent. New releases, revisions, seasonal distortions, or changes in high-frequency data can shift the estimate before official data are complete.