Economic Surprise Index measures whether actual macroeconomic data releases are coming in above or below consensus expectations. It is an expectation-relative indicator, so it can improve or weaken even when the underlying economy is still expanding. It does not measure absolute economic growth, and it is not a standalone forecast of market direction.

Definition: Economic Surprise Index is a macro data indicator that compares reported economic releases with the forecasts markets expected before those releases. Positive readings generally mean data is beating expectations. Negative readings generally mean data is missing expectations.

The main idea is simple: markets often react not only to whether economic data is strong or weak, but to whether the data is stronger or weaker than expected. A moderate data release can be treated as supportive if expectations were very low, while a still-healthy release can create disappointment if expectations were too high.

Key Points

- Economic Surprise Index compares actual macro data with consensus expectations.

- Positive readings generally point to upside surprises, while negative readings point to downside surprises.

- The index is expectation-relative, not a direct measure of economic strength.

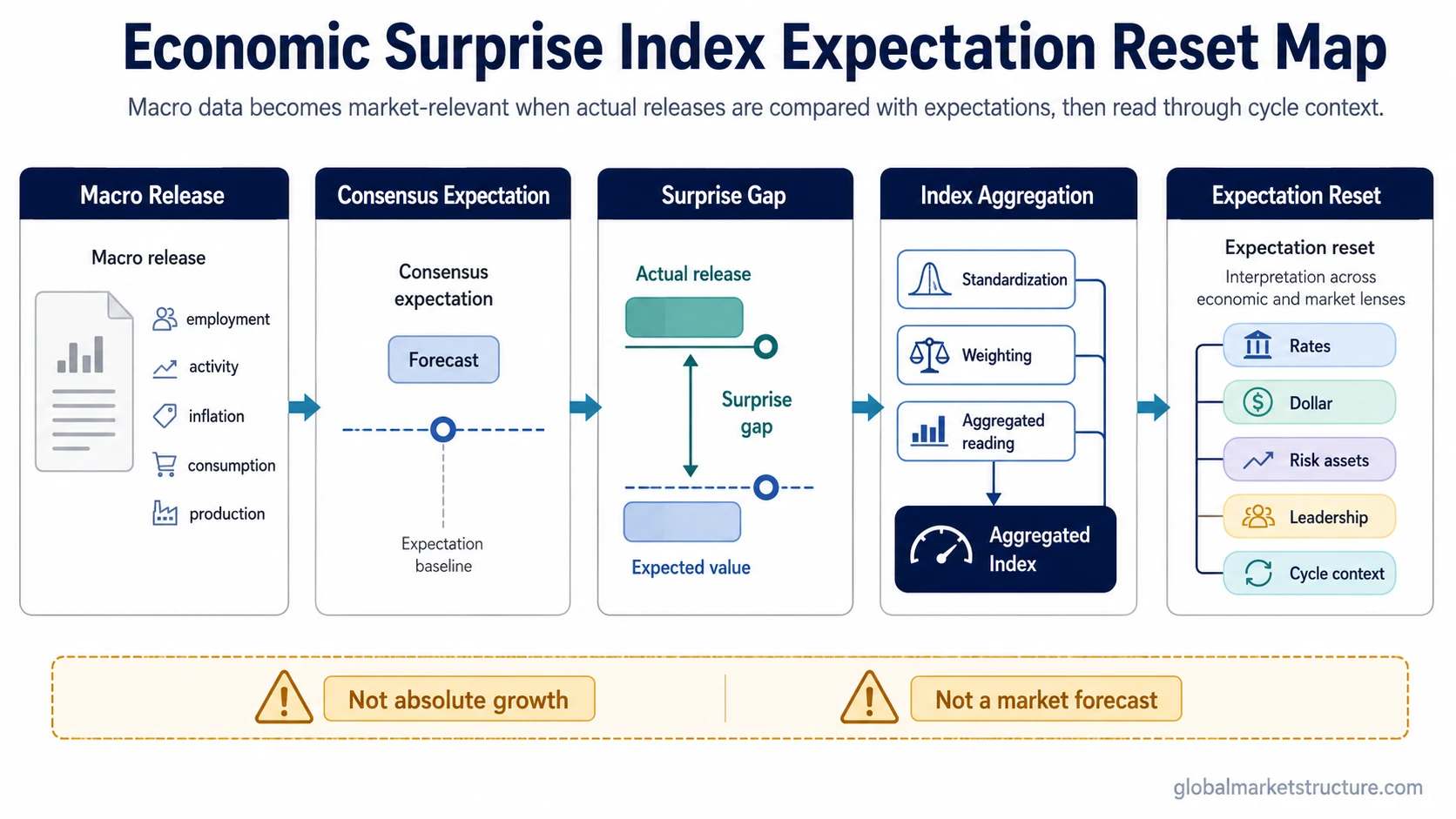

- Market interpretation depends on cycle context, policy expectations, rates, the dollar, risk appetite, and leadership behavior.

- A single surprise reading should not be treated as a recession call, equity forecast, or trading signal.

What the Economic Surprise Index Measures

The Economic Surprise Index measures the gap between reported macroeconomic data and the consensus forecast for that data. The release may involve activity, employment, inflation, consumption, production, or other scheduled macro indicators, depending on the provider methodology and regional index being used.

The index is different from Economic Growth. Growth describes the level or rate of real activity in the economy. Economic surprise describes whether incoming data is better or worse than expected. A growing economy can still generate negative surprises if expectations were set too high.

| Reading direction | What it can mean | What it does not prove | Market-structure boundary |

|---|---|---|---|

| Positive surprise | Actual data is generally beating consensus expectations. | It does not prove the economy is strong in absolute terms. | Interpret alongside growth trend, policy reaction, rates, dollar pressure, and risk appetite. |

| Negative surprise | Actual data is generally missing consensus expectations. | It does not prove recession or immediate market weakness. | Check whether expectations rose too far, whether data is still expanding, and whether markets already priced disappointment. |

| Rising index | Data is increasingly beating forecasts or missing them by less than before. | It does not guarantee risk assets will rise. | Market response depends on inflation pressure, central-bank expectations, positioning, and leadership quality. |

| Falling index | Data is increasingly disappointing relative to forecasts. | It does not automatically mean activity is contracting. | The fall may reflect expectations resetting higher faster than actual data improves. |

How the Economic Surprise Index Is Calculated

Economic surprise indexes usually begin with a scheduled data release and a consensus forecast. The surprise is the difference between the reported value and the expected value. Because different indicators have different units, volatility, and market importance, providers typically standardize and aggregate surprises rather than simply adding raw differences together.

Mechanism sequence: macro release, consensus expectation, surprise magnitude, standardization or weighting, aggregated index reading, expectation reset, and market interpretation.

The exact formula can vary by provider. A provider may weight releases differently, use regional baskets, adjust for historical surprise behavior, or emphasize particular data categories. For concept-level interpretation, the important point is that the index turns many individual actual-versus-expected releases into one broad reading about whether the macro data flow is surprising to the upside or downside.

How Markets Interpret Surprise Readings

Economic surprise readings matter because markets price expectations. When data repeatedly beats forecasts, investors may revise growth expectations, policy expectations, earnings assumptions, or risk appetite. When data repeatedly misses forecasts, the same process can work in reverse, especially if disappointments appear across several important indicators.

The market response is conditional. Stronger surprises can put upward pressure on yields if markets expect firmer growth or a more restrictive central-bank path. The dollar may respond if rate differentials or global liquidity expectations shift. Risk assets may react positively if stronger data supports growth confidence, but the response can weaken if the same data increases inflation concern or policy-tightening risk.

Leadership can also matter. Cyclical sectors, defensive sectors, growth-sensitive assets, value-sensitive assets, and rate-sensitive groups may interpret the same surprise backdrop differently. A surprise index therefore works best as part of a broader macro regime check, not as a single-market rule.

Why Surprise Readings Can Mislead

Common misread: A falling Economic Surprise Index does not automatically mean economic data is deteriorating in absolute terms. It can mean expectations became harder to beat. A rising index does not automatically mean the economy is strong. It can mean weak data is coming in less badly than expected.

The strongest false reading comes from confusing surprise with level. A data release can remain expansionary and still disappoint if the forecast was higher. Another release can remain weak and still surprise positively if the market expected something worse. That is why surprise readings need to be checked against the broader growth path, policy setting, credit conditions, liquidity, and cross-asset confirmation.

The index can also become less informative when one data category dominates the move, when forecasts adjust rapidly, or when markets are focused on a different macro constraint. During an inflation-sensitive regime, upside growth surprises may not carry the same meaning as they would during a growth-scarce regime.

Economic Surprise Index vs Economic Growth and PMI

Economic Surprise Index, economic growth, and the Purchasing Managers Index can all describe the growth-and-activity backdrop, but they answer different questions.

| Concept | Main question | Best interpretation use |

|---|---|---|

| Economic Surprise Index | Is incoming data beating or missing expectations? | Expectation reset and market reaction context. |

| Economic Growth | Is real output expanding or contracting? | Activity level, cycle phase, and growth trend context. |

| Purchasing Managers Index | Are surveyed business conditions improving or weakening? | Forward-looking activity conditions and diffusion-style signals. |

The distinction matters because markets can respond to the expectation gap before the full growth picture changes. Surprise readings can influence expectations quickly, while growth data and business surveys help judge whether the underlying activity trend is actually changing.

Economic Surprise Index Example in Context

Economic data can keep improving while the surprise index weakens. A common scenario is that several activity releases beat forecasts for a period, causing economists and markets to raise expectations for the next data cycle. Later releases may still look healthy in absolute terms, but they begin to fall short of the new, higher forecasts. The surprise index can decline even though the economy has not moved into contraction.

The opposite can also happen. If expectations fall too far, weak data can generate positive surprises simply by being less weak than feared. That can support a short-term expectation reset, but it does not prove that the full growth cycle has turned. The market-structure reading becomes stronger only when surprise direction aligns with broader growth evidence, policy expectations, credit conditions, liquidity, and leadership behavior.

Related Concepts

The most practical use is not prediction. The value comes from identifying expectation reset risk: when optimism has become difficult to beat, when pessimism has become too extreme, or when market leadership starts confirming that the data surprise pattern is changing how capital is being priced.

FAQ

What does the Economic Surprise Index mean?

Economic Surprise Index means actual macroeconomic data is being compared with consensus expectations. Positive readings generally show data beating forecasts, while negative readings show data missing forecasts.

Is the Economic Surprise Index the same as economic growth?

No. Economic growth describes the level or rate of real activity. Economic surprise describes whether incoming data is better or worse than expected.

Does a negative Economic Surprise Index mean recession?

No. A negative reading means data is missing expectations. It may occur while the economy is still expanding if expectations were set too high.

Can the Economic Surprise Index predict markets?

No. The index can help interpret expectation resets, but market direction depends on policy expectations, rates, the dollar, liquidity, credit, positioning, and leadership context.