Monetary policy divergence means major central banks are moving along different policy paths. One central bank may be tightening, another may be easing, pausing, changing balance-sheet policy, or guiding future rates differently. The market effect can run through rates, yield curves, currency pressure, liquidity expectations, and capital flows, but divergence is not a forecast or trade call by itself.

Definition: Monetary policy divergence is the separation between central-bank policy paths across economies or currency areas. It can involve policy rates, expected future rates, forward guidance, quantitative easing, quantitative tightening, balance-sheet policy, and the credibility of each policy stance.

Key Points

- Monetary policy divergence is broader than a simple interest-rate gap.

- The concept begins with central-bank policy paths, not currency moves or asset-price outcomes.

- Observable inputs include policy rates, expected rate paths, guidance, balance-sheet policy, yield curves, real yields, currencies, and capital-flow pressure.

- Currency and capital-flow reactions are conditional because markets price expectations, credibility, risk appetite, hedging costs, and existing positioning.

- Divergence can shape market structure, but it should not be read as a standalone prediction.

What Monetary Policy Divergence Means

Monetary policy becomes divergent when central banks respond differently to inflation, growth, financial conditions, currency pressure, or domestic stress. The separation can be visible in actual policy rates, but it can also appear through expected future policy, communication, balance-sheet operations, and the market’s belief that a central bank will stay restrictive or accommodative for longer.

A simple example is a global environment where one central bank signals tighter policy to restrain inflation while another signals easier policy to support weak growth. The important point is not that one currency or asset must move in a fixed direction. The important point is that the policy backdrop is no longer synchronized, so rate expectations, liquidity assumptions, currency pricing, and capital allocation can begin to separate.

| What it is | What it is not |

|---|---|

| Separation between central-bank policy paths | A generic disagreement between governments or policymakers |

| A way to compare tightening, easing, pauses, guidance, and balance-sheet policy | A live central-bank forecast table |

| A market-structure input for rates, FX, liquidity, and capital-flow interpretation | A direct forecast for currencies, commodities, bonds, or equities |

| A broader concept than the visible policy-rate gap alone | The same thing as interest-rate divergence |

Observable Inputs

Monetary policy divergence is easier to read when the inputs are separated. A policy-rate gap may be visible, but the market often reacts more to the expected path than to the current rate alone.

| Input | What it can reveal | Why it needs context |

|---|---|---|

| Policy rates | Current stance difference between central banks | The current rate may already be priced into yields and currencies |

| Expected rate path | How markets price future tightening, easing, or pauses | Expectations can change before official policy changes |

| Forward guidance | Whether central banks are guiding markets toward different future paths | Guidance depends on credibility and incoming data |

| Balance-sheet policy | Whether liquidity support or liquidity withdrawal differs across regions | Quantitative easing and tightening affect market conditions through more than policy rates |

| Yield curves and real yields | Whether divergence is appearing in market-implied funding, growth, and inflation expectations | Yield moves can reflect growth stress, inflation risk, or liquidity demand |

| Currencies and capital-flow pressure | Whether investors are reassessing exposure to a currency area | Hedging costs, currency risk, domestic policy response, and broader risk appetite can dominate the rate comparison |

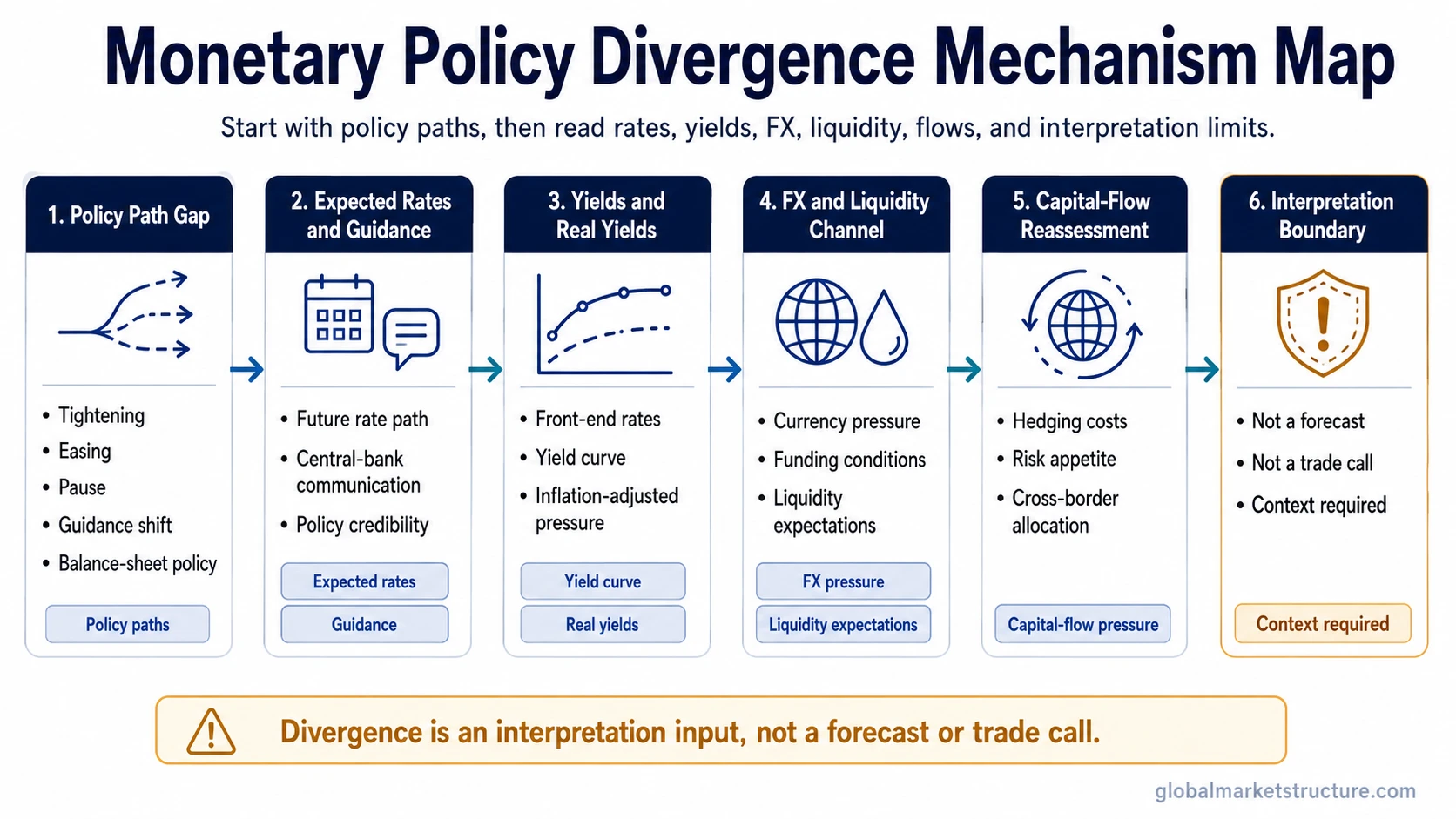

How Monetary Policy Divergence Moves Through Markets

The first step is the central-bank path gap. One central bank may be expected to hold rates higher for longer while another may be expected to ease earlier. That gap can affect short-term rates, yield curves, real yields, and relative currency pressure.

The second step is the expectation channel. Markets do not wait only for official rate decisions. They also price speeches, inflation releases, labor-market data, financial stress, and changes in balance-sheet policy. A divergence reading becomes more fragile when the market has already priced the expected policy gap.

The third step is the liquidity and capital-flow channel. A more restrictive policy path can affect funding conditions, hedging costs, and currency demand, but the direction is not automatic. Investors may reassess exposure to a currency area for yield reasons, risk reasons, balance-sheet reasons, or liquidity reasons, and those forces can conflict.

Monetary Policy Divergence vs Interest-Rate Divergence

Interest-rate divergence is narrower. It focuses on differences between interest rates, bond yields, or expected rate levels. Monetary policy divergence includes those rate differences, but it also includes central-bank communication, expected policy paths, balance-sheet policy, and credibility.

Generic policy divergence can describe many government or institutional differences. Monetary policy divergence is narrower: it compares central-bank stance, guidance, expected rates, and balance-sheet policy across economies.

Policy divergence and currency moves is a related FX-channel question. Monetary policy divergence starts one step earlier, with the policy paths themselves. Currency behavior is one possible transmission channel, not the full concept.

Common False Readings

False reading 1: Divergence predicts currency direction. A higher expected rate path can support a currency in some conditions, but growth risk, hedging costs, external balances, positioning, and risk appetite can change the result.

False reading 2: The current policy-rate gap is the whole story. The expected path, guidance, balance-sheet policy, and credibility of the reaction function can matter more than the current rate.

False reading 3: Divergence creates a direct market call. Divergence is an interpretation input. Asset outcomes still depend on valuation, positioning, credit, liquidity, growth expectations, and prior pricing.

False reading 4: Every central-bank difference is meaningful divergence. Some differences are already priced, temporary, or offset by common global forces and cross-border spillovers.

A Practical Scenario

A common scenario is that one central bank keeps a restrictive tone because inflation is still above target, while another begins signaling future easing because growth is slowing. The initial read may be that the restrictive central bank’s currency should strengthen. That read is incomplete if markets already priced the policy gap or if the restrictive economy is also showing weaker growth and rising credit stress.

A cleaner reading appears when expected rate paths, real yields, guidance, currency behavior, and capital-flow pressure broadly agree. A weaker reading appears when currency behavior contradicts the rate comparison, yield curves price growth stress, or risk appetite overwhelms the relative policy story.

Where Monetary Policy Divergence Fits

Monetary policy divergence sits upstream of several market channels. Monetary policy defines the central-bank stance. The monetary transmission mechanism describes how that stance can move through credit, rates, expectations, asset prices, and the real economy. Divergence compares those policy paths across economies.

Within global divergences, the useful sequence is policy path first, then rates and yields, then currency behavior, then liquidity and capital-flow confirmation. That sequence reduces the risk of treating a single FX move or yield spread as the entire macro story.

FAQ

Is monetary policy divergence the same as interest-rate divergence?

No. Interest-rate divergence focuses on rate and yield gaps. Monetary policy divergence is broader because it includes expected policy paths, guidance, balance-sheet policy, and policy credibility.

Does monetary policy divergence predict currency moves?

No. It can influence currency pressure, but FX markets also price growth risk, inflation credibility, positioning, external balances, hedging costs, and risk appetite.

What makes monetary policy divergence harder to interpret?

It becomes harder to interpret when the policy gap is already priced, when yield curves reflect growth stress, when currency moves contradict rate differentials, or when common global forces reduce the importance of local policy differences.