Interest rate divergence means interest-rate paths are separating across economies, central-bank regimes, or market-implied yield curves. The separation can change yield gaps, currency pressure, carry incentives, and capital-flow interpretation. It is not the same as a static interest-rate differential, and it is not a standalone forecast, buy/sell signal, or allocation rule.

Definition: Interest rate divergence is the process or condition where policy-rate paths, expected rate paths, or yield paths move differently across economies or markets. It describes rate-path separation, not a guaranteed outcome in currencies, bonds, equities, or capital flows.

Key Points

- Interest rate divergence focuses on rate paths moving apart, not only on the size of a rate spread at one moment.

- The concept often matters through yield gaps, currency behavior, carry incentives, and cross-border capital-flow conditions.

- A higher nominal rate can be misleading if inflation, real yields, growth risk, liquidity, or credibility point in another direction.

- Rate divergence becomes more useful when it is compared with real yields, curve shape, risk appetite, credit conditions, and market positioning.

What Interest Rate Divergence Means

Interest rate divergence appears when two economies, central-bank regimes, or market yield curves stop moving in the same direction. One economy may keep policy rates high while another begins cutting. One bond market may price slower easing while another prices faster easing. One curve may reprice the front end sharply while another moves mainly at the long end.

The concept belongs to rates and intermarket analysis because rate-path separation can change relative yield compensation across markets. That can affect currency behavior, hedging costs, carry incentives, capital allocation, and the way investors compare risk across regions.

The important boundary is that divergence describes a pressure channel. It does not say that a currency must rise, that capital must flow into the higher-rate economy, or that one asset class should be preferred mechanically.

Interest Rate Divergence Compared With Related Concepts

Several nearby concepts sound similar but measure different things. Monetary-policy divergence is broader than interest rate divergence because policy stance can also include balance-sheet policy, forward guidance, reaction functions, and liquidity operations.

| Concept | What it focuses on | Main interpretation use | Main limitation |

|---|---|---|---|

| Interest rate divergence | Policy-rate paths, expected rate paths, or yield paths moving differently across economies or markets. | Interpreting yield gaps, FX pressure, carry incentives, and capital-flow pressure. | It does not automatically forecast currency direction or capital-flow outcomes. |

| Interest-rate differential | The measured spread between two interest rates at a point in time. | Comparing the level of rate compensation between two markets. | A static spread can miss whether the path is widening, narrowing, or repricing quickly. |

| Monetary-policy divergence | Differences in overall policy stance, central-bank reaction functions, guidance, balance sheets, and rates. | Classifying broader policy separation across economies. | It can be broader than the interest-rate channel alone. |

| Real-yield divergence | Differences in inflation-adjusted yield pressure across markets. | Separating nominal rate levels from inflation-adjusted return pressure. | Real yields do not remove the need to check growth, liquidity, credibility, and positioning. |

| Yield-curve divergence | Different behavior between curve segments across markets, such as front-end repricing versus long-end repricing. | Identifying where the market is repricing policy, growth, inflation, or term premium. | Curve shape can send mixed signals when short and long maturities move for different reasons. |

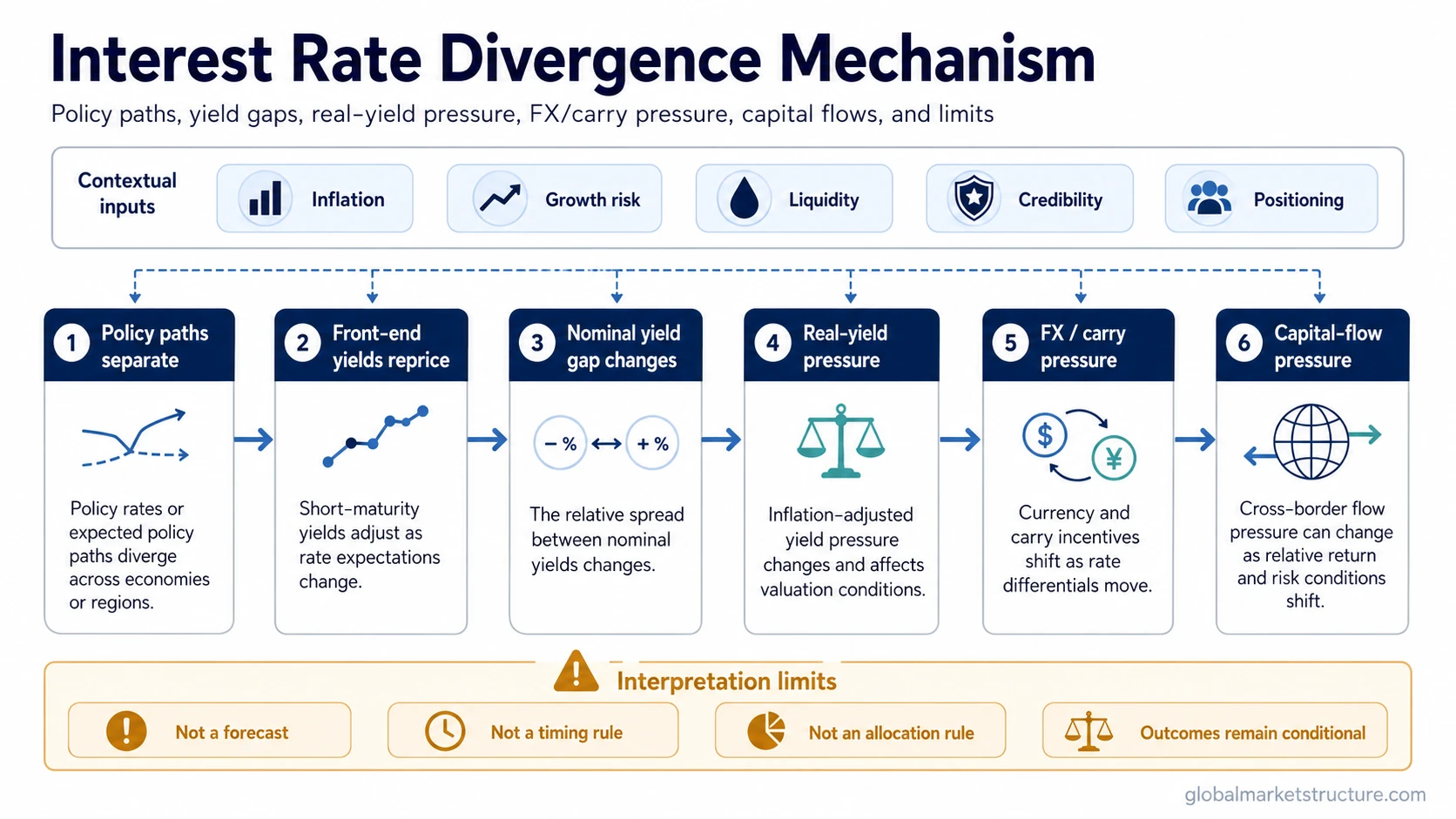

How Interest Rate Divergence Moves Through Markets

The transmission path usually starts with a difference in expected policy rates. If one central bank is expected to keep rates higher for longer while another is expected to cut, front-end yields can reprice in different directions. That changes the nominal yield gap between the two markets.

Mechanism sequence: policy-rate path separation → front-end yield repricing → nominal yield spread change → real-yield pressure → FX and carry pressure → capital-flow pressure → interpretation limit.

The FX channel is often visible because currencies respond to relative return expectations, hedging costs, and the compensation available for holding one currency over another. A wider rate gap can support carry incentives, but carry is only one input. Currency behavior can still be shaped by inflation, growth risk, external balances, policy credibility, liquidity conditions, and crowded positioning.

The capital-flow channel is also conditional. Higher relative yields may attract capital when credibility, liquidity, and risk appetite are supportive. The same yield advantage can be less persuasive when investors fear currency depreciation, credit stress, weak growth, capital controls, or a policy mistake.

Why Interest Rate Divergence Matters for Intermarket Analysis

Interest rate divergence helps connect central-bank expectations with cross-market pressure. It can explain why two bond markets stop moving together, why a currency pair becomes more sensitive to rate expectations, or why international capital allocation starts reacting to relative yield changes.

For market-structure interpretation, the concept is most useful when it is placed beside other evidence. A rate-path separation that also appears in real yields, FX behavior, liquidity conditions, credit spreads, and capital-flow data carries more information than a nominal yield gap alone.

The same rate divergence can have different meanings across regimes. During a growth-led environment, higher rates may reflect stronger nominal activity or delayed easing. During an inflation-pressure environment, higher rates may reflect policy restraint. During a stress environment, a higher yield may reflect risk compensation rather than attractive return.

Interest Rate Divergence vs Interest-Rate Differential

An interest-rate differential is a measurement. Interest rate divergence is a path condition. The differential tells how wide the rate spread is now. Divergence tells whether rate paths are separating, converging, or repricing at different speeds.

That distinction matters because a large spread is not always new information. A market may already price a wide differential, while the more important change is whether expectations are moving wider or narrower. A smaller spread can also matter if it is changing quickly or if real-yield pressure is moving in the opposite direction from nominal rates.

Practical distinction: a 2 percentage point rate gap is a differential. A shift from parallel policy paths to one market pricing higher-for-longer rates while another prices cuts is divergence.

Why Real Yields and Curve Shape Matter

Nominal rates can mislead when inflation conditions differ. A country may have a higher nominal yield, but if inflation expectations are also higher, the real-yield advantage may be smaller than it first appears. Real-yield divergence helps separate rate level from inflation-adjusted pressure.

Curve shape adds another layer. Front-end yields usually respond more directly to expected policy-rate changes. Long-end yields can also reflect growth expectations, inflation risk, term premium, fiscal concerns, or global duration demand. Two economies can have similar policy-rate paths while their long-end yields diverge for different reasons.

A cleaner interpretation comes from asking where the divergence is happening. Front-end divergence points more directly toward policy expectations. Long-end divergence may require more caution because it can mix inflation, growth, term premium, fiscal risk, and global bond-demand forces.

Simple Interest Rate Divergence Scenario

One economy keeps rates high because inflation pressure remains persistent, while another begins cutting because growth is weakening. The nominal yield gap widens. Currency pressure may shift toward the higher-yielding economy, and carry incentives may become more visible.

The interpretation is still incomplete. If the higher-rate economy also has weaker credibility, rising inflation expectations, deteriorating liquidity, or crowded positioning, the yield advantage may not translate into a stronger currency or durable capital inflow. If real yields, FX behavior, credit conditions, and liquidity confirm the same direction, the divergence becomes a more meaningful macro pressure signal.

Common Misreadings of Interest Rate Divergence

Interest rate divergence often becomes misleading when it is read as a mechanical forecast. A higher rate is not automatically a stronger currency. A wider yield gap is not automatically a capital-flow guarantee. A policy-rate difference is not automatically a risk-on or risk-off regime signal.

Limitation: rate divergence can inform macro interpretation, but it should not be converted directly into a market decision without broader evidence.

| False reading | Why it is incomplete | Better check |

|---|---|---|

| Higher rates mean a stronger currency. | Inflation, credibility, growth risk, and positioning can offset nominal yield support. | Compare real yields, FX behavior, external balances, and policy credibility. |

| Wider rate gaps guarantee capital inflows. | Investors may avoid higher yields if currency, liquidity, or credit risk is rising. | Check liquidity, credit spreads, hedging costs, and capital-flow evidence. |

| Rate divergence is a trading signal. | A rate path can describe pressure without defining timing, risk, or outcome. | Keep the concept inside macro interpretation and require broader confirmation. |

| Interest rate divergence equals monetary-policy divergence. | Policy divergence can include guidance, balance sheets, liquidity tools, and reaction functions. | Separate the rate channel from the broader policy stance. |

How to Interpret Interest Rate Divergence Safely

A disciplined reading starts with the rate path, then checks what type of rate is diverging. Policy rates, short-end yields, long-end yields, nominal yields, and real yields can all move for different reasons.

The next step is cross-asset confirmation. FX behavior, inflation expectations, credit conditions, liquidity, capital-flow evidence, and market positioning can either support or weaken the initial rate signal. A rate divergence that appears only in one isolated spread is less reliable than one that aligns across several related markets.

The strongest interpretation remains conditional: rate divergence can describe pressure, transmission, and relative-market stress, but it does not remove uncertainty. It becomes more useful when it explains why markets are repricing, not when it is used as a shortcut for predicting what must happen next.

FAQ

What is interest rate divergence?

Interest rate divergence is the separation of policy-rate paths, expected rate paths, or yield paths across economies or markets. It helps explain relative yield pressure, FX pressure, carry incentives, and capital-flow interpretation.

How is interest rate divergence different from an interest-rate differential?

An interest-rate differential is the measured spread between two rates at one point in time. Interest rate divergence describes the process or condition where rate paths move apart, converge, or reprice at different speeds.

Is interest rate divergence the same as monetary-policy divergence?

No. Interest rate divergence focuses on rate paths and yield paths. Monetary-policy divergence is broader because it can include guidance, balance-sheet policy, liquidity tools, and central-bank reaction functions.

Does a wider interest rate gap predict a stronger currency?

No. A wider rate gap can affect currency pressure, but currency behavior also depends on inflation, real yields, growth risk, external balances, liquidity, policy credibility, and market positioning.