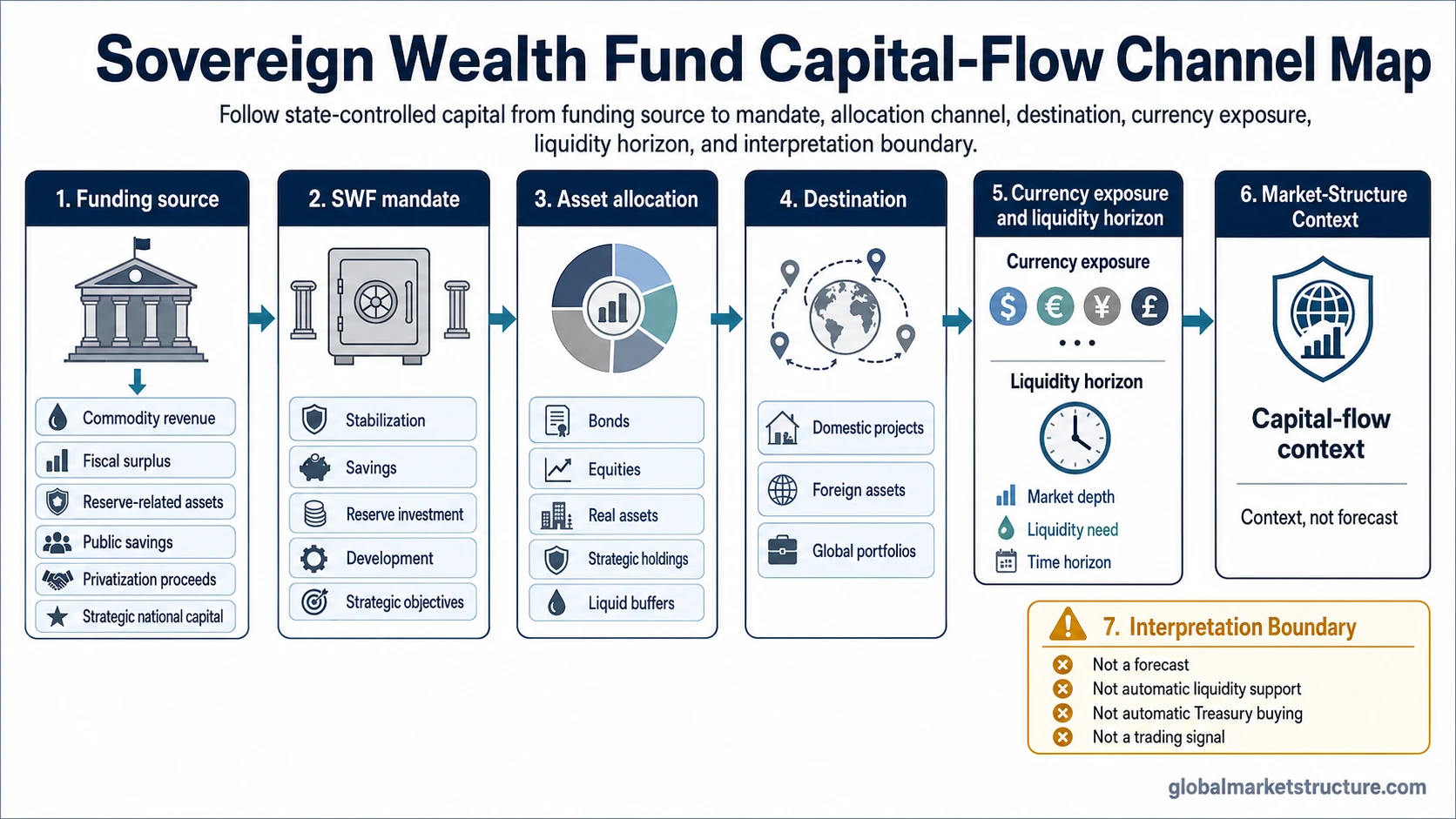

A sovereign wealth fund is a government-owned investment fund that allocates state-controlled capital under a defined mandate. The capital may come from commodity revenue, fiscal surpluses, reserve-related assets, public savings, privatization proceeds, or strategic national capital.

A sovereign wealth fund is not the same thing as central-bank reserves, foreign exchange intervention, or an ordinary public pension fund. Its market-structure relevance comes from how official capital is allocated, where it flows, what currency exposure it creates, and whether the flow is long-term investment, rebalancing, drawdown, or short-term liquidity management.

SWF activity should not be treated as a standalone forecast, automatic liquidity signal, Treasury-buying proof, risk-on signal, or trading signal. The fund label matters only after mandate, funding source, asset channel, currency exposure, liquidity need, and time horizon are separated.

What Is a Sovereign Wealth Fund?

A sovereign wealth fund, often shortened to SWF, is an investment vehicle owned by a government or sovereign authority. It is usually separated from the ordinary budget process and managed according to an investment objective, policy mandate, or national financial purpose.

The defining features are government ownership, state-controlled capital, and an investment mandate. The mandate can focus on stabilizing public finances, saving wealth for future generations, investing surplus reserve-related assets, supporting domestic development, or managing strategic national assets.

The same label can cover very different structures. A commodity exporter may use an SWF to transform resource revenue into diversified foreign assets. Another country may use a fund to invest fiscal surpluses, support long-term public liabilities, or pursue strategic development goals. The market meaning depends on the fund’s mandate, assets, currency exposure, liquidity needs, and time horizon.

How Sovereign Wealth Funds Work

Sovereign wealth funds work by moving state-controlled capital into an investment structure with rules for funding, allocation, risk, liquidity, and governance. The fund may receive capital from export revenue, budget surpluses, privatization proceeds, reserve accumulation, or other official sources.

Once capital enters the fund, the investment mandate determines how the assets are managed. Some funds prioritize liquidity and capital preservation. Others accept longer horizons and broader asset exposure. A stabilization fund may hold more liquid assets because it may need to support the public budget during revenue shocks. A future-generation fund may hold longer-duration global assets because its purpose is intergenerational saving.

Market-Structure Reading

The fund label alone is not enough. The important questions are what capital is being allocated, where it is going, what currency is involved, how liquid the assets are, and whether the fund is accumulating, rebalancing, or drawing down capital.

Main Types of Sovereign Wealth Funds

Sovereign wealth funds are often grouped by purpose. The categories can overlap, but the classification helps separate fiscal stabilization, long-term saving, reserve-linked investment, development objectives, and liability-related structures.

| Type | Role | Market-structure relevance |

|---|---|---|

| Stabilization fund | Buffers fiscal or commodity-revenue volatility. | Can matter during stress if assets are sold, liquidity is preserved, or revenue shocks change official funding needs. |

| Savings or future-generation fund | Converts current national wealth into long-horizon assets. | Can shape long-term demand for foreign assets, real assets, equities, bonds, or diversified portfolios. |

| Reserve-investment fund | Invests assets linked to reserve accumulation, surplus savings, or external buffers. | Can overlap with reserve-management context, but it should not be collapsed into central-bank reserves. |

| Development or strategic fund | Supports domestic, industrial, infrastructure, or strategic objectives. | May be less relevant to liquid global markets if the mandate is domestic, strategic, or project-based. |

| Pension-reserve style fund | Supports future public liabilities where the fund structure fits SWF classification. | Requires careful classification because not every public pension fund is a sovereign wealth fund. |

Sovereign Wealth Fund vs Foreign Exchange Reserves, Pension Funds, and FX Intervention

The most common mistake is treating all official assets as the same thing. A sovereign wealth fund can sit near the reserve and public-finance system, but its purpose differs from foreign exchange reserves, foreign exchange intervention, and ordinary pension funding.

| Concept | What it is | Do not confuse with |

|---|---|---|

| Sovereign wealth fund | A government-owned investment vehicle with a defined mandate. | Not automatically central-bank reserves or a currency-management tool. |

| Foreign exchange reserves | Official reserve assets held for monetary, external-liquidity, or balance-of-payments purposes. | Not automatically an SWF, even when reserve assets are large. |

| Foreign exchange intervention | An active operation in the currency market, usually to influence exchange-rate conditions or manage disorderly pressure. | Not the same as long-term SWF asset allocation. |

| Public pension fund | A fund primarily tied to pension liabilities and future benefit payments. | Not always an SWF unless the fund’s structure and source classification support that label. |

Why Sovereign Wealth Funds Matter for Market Structure

A sovereign wealth fund matters for market structure because it can convert official income, savings, or surplus assets into demand for financial assets. That does not mean every SWF flow moves markets. The effect depends on the size of the flow relative to market depth, the asset class involved, the currency exposure, and the fund’s investment horizon.

The same headline can imply different things under different mandates. A stabilization fund drawing down liquid assets during a fiscal shock has a different market meaning from a future-generation fund allocating slowly into global equities or real assets. A reserve-linked investment fund also has a different interpretation from a domestic strategic fund investing in infrastructure or national development projects.

How to Read SWF Activity

A useful market-structure sequence is to identify the mandate, funding source, asset channel, currency exposure, liquidity preference, portfolio horizon, and flow direction. Only then can SWF activity be interpreted as capital-flow context.

Common Misreadings of Sovereign Wealth Funds

False reading: a sovereign wealth fund automatically means liquidity support, risk-on flows, Treasury buying, dollar strength, equity support, or a trading signal.

Better reading: SWF activity is conditional capital-flow context. Its market relevance depends on mandate, funding source, allocation channel, currency exposure, liquidity conditions, and time horizon.

A large fund can be important without creating an immediate market signal. A fund can also be visible in rankings without producing near-term flow pressure. Size, mandate, asset mix, and liquidity behavior matter more than the label alone.

Example Scenario: From Export Revenue to Foreign Assets

A commodity-exporting country may accumulate revenue during a strong export cycle. Part of that revenue can be transferred into a sovereign wealth fund rather than spent immediately through the public budget.

The fund may allocate across foreign bonds, equities, real assets, strategic holdings, or liquid buffers. The market meaning depends on the destination. Long-term allocation into diversified assets is different from short-term liquidity management, fiscal stabilization, or reserve defense.

The market read should stay at the channel level: official revenue moves into an allocation vehicle, and the destination determines whether the flow matters for liquidity, duration demand, currency exposure, or long-horizon portfolio demand.

Related Concepts

Sovereign wealth funds sit inside the broader official-flow system. These related concepts separate reserve assets, currency-market operations, portfolio allocation, and commodity-revenue recycling.

- Foreign exchange reserves explain the official reserve-asset side of the sovereign-flow system.

- Foreign exchange intervention explains active currency-market operations and intervention context.

- Sovereign wealth fund asset allocation explains the asset-channel layer in more detail.

- Petrodollar recycling explains how oil-export revenue can return to the global economy through spending and investment channels.

FAQ

Is a sovereign wealth fund the same as foreign exchange reserves?

No. Foreign exchange reserves are official reserve assets used for monetary, external-liquidity, or balance-of-payments purposes. A sovereign wealth fund is a government-owned investment vehicle with its own mandate. The two can be related, but they should not be treated as identical.

Are sovereign wealth funds the same as public pension funds?

No. A public pension fund is primarily tied to pension liabilities and benefit payments. Some pension-reserve style structures may be discussed near the SWF universe, but an ordinary pension fund should not be called a sovereign wealth fund without source support.

Do sovereign wealth funds affect markets?

They can affect markets when their flows are large enough relative to market depth or when their allocation choices change demand for assets, currencies, or liquidity. The effect depends on mandate, funding source, asset channel, currency exposure, and time horizon.

Are all sovereign wealth funds funded by oil revenue?

No. Some are funded by commodity revenue, but others may be linked to fiscal surpluses, reserve-related assets, public savings, privatization proceeds, or strategic national capital. Oil revenue is one funding path, not the whole category.

Can sovereign wealth fund activity predict markets?

No. SWF activity should not be treated as a standalone forecast or trading signal. It is better used as capital-flow context that must be interpreted alongside mandate, asset allocation, liquidity conditions, currency exposure, and broader market structure.