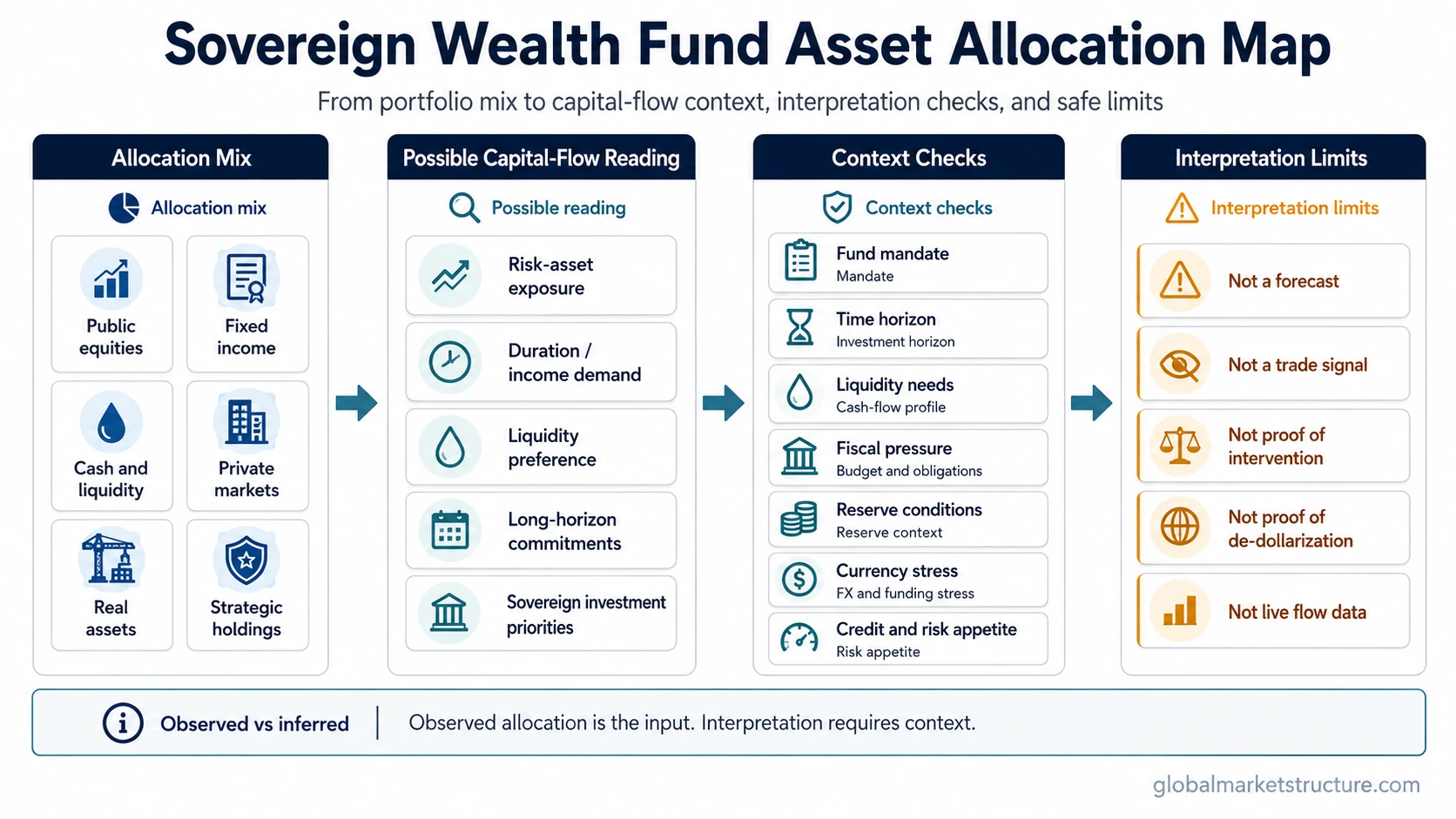

Sovereign wealth fund asset allocation is the way a state-owned investment fund divides capital across public equities, fixed income, cash, private markets, real assets, alternatives, and strategic holdings. The mix can help interpret capital-flow pressure, but only when mandate, time horizon, liquidity needs, liabilities, fiscal context, reserve conditions, and broader risk appetite are considered together.

Definition: Sovereign wealth fund asset allocation is the fund-level portfolio mix used by a sovereign wealth fund to distribute capital across asset classes according to its objective, constraints, and investment horizon.

The useful reading is not the allocation mix by itself, but what that mix suggests when it is tested against liquidity, fiscal pressure, reserve conditions, currency stress, and global risk appetite.

Key Points

- Sovereign wealth fund asset allocation is a portfolio mix, not a market forecast.

- Allocation choices depend on fund mandate, horizon, liabilities, liquidity needs, governance, and sovereign balance-sheet context.

- Allocation shifts can support capital-flow analysis only when they align with wider liquidity and risk conditions.

- SWF assets and reserve assets can be related in sovereign balance-sheet analysis, but they are not the same category.

What Drives Sovereign Wealth Fund Asset Allocation

SWF allocation starts with the fund’s purpose. A stabilization fund may need more liquidity because it can be used to cushion budget pressure or commodity-revenue volatility. A savings fund can usually accept a longer horizon. A pension reserve fund may focus more on future liabilities. A strategic development fund may hold assets connected to national investment goals.

That mandate changes how the same allocation should be read. A higher share of private assets may reflect long-term illiquidity tolerance. A higher share of liquid fixed income may reflect liability matching, reserve-adjacent liquidity needs, or a more cautious funding environment. The allocation mix becomes more informative when it fits the fund’s role rather than when it is read as a generic risk-on or risk-off signal.

Major Allocation Buckets

| Allocation bucket | Common role | Interpretation limit |

|---|---|---|

| Public equities | Exposure to global earnings, equity beta, and long-term capital appreciation. | Higher equity exposure may increase sensitivity to risk assets, but it is not enough to prove near-term risk appetite. |

| Fixed income | Income, duration exposure, liquidity, collateral quality, or liability matching. | A larger fixed-income allocation may reflect yield, liquidity, or liability needs rather than a simple defensive view. |

| Cash and liquidity assets | Redemption flexibility, fiscal transfer capacity, and short-term liquidity management. | Higher liquidity can signal caution, but it can also reflect operational needs or upcoming commitments. |

| Private markets | Long-horizon exposure to private equity, private credit, infrastructure, and illiquidity premia. | Private-market exposure should not be read as immediate public-market support because commitments and cash calls can be delayed. |

| Real estate and infrastructure | Real-asset exposure, income, inflation sensitivity, and strategic ownership. | These assets can reflect long-term mandate design more than current market timing. |

| Alternatives | Diversification, hedge-fund exposure, commodities, or non-traditional risk premia. | Alternative exposure needs context from strategy, liquidity terms, and governance constraints. |

| Strategic direct investments | Domestic development, sector strategy, or national capital allocation goals. | Strategic holdings can reflect policy objectives rather than ordinary portfolio optimization. |

How Allocation Mix Can Affect Capital-Flow Interpretation

SWF allocation can matter for market-structure analysis because large sovereign funds sit at the intersection of fiscal policy, reserves, global portfolios, and cross-border capital flows. A change in allocation may influence demand for public equities, government bonds, credit, private assets, currencies, or real assets, depending on the fund’s scale and implementation path.

The observed allocation is only the starting point. The useful inference depends on whether the change is consistent with liquidity conditions, reserve pressure, fiscal needs, currency stress, funding conditions, and broader risk appetite.

Observed versus inferred: The observed fact is the allocation mix. The inference is what that mix may suggest about sovereign constraints, risk appetite, liquidity preference, or cross-border capital behavior. Those two layers should stay separate.

Misread vs Safer Interpretation

| Misread | Safer interpretation |

|---|---|

| A higher private-market allocation proves that sovereign capital is turning aggressively risk-on. | Higher private-market exposure may reflect long horizon, illiquidity tolerance, mandate design, lower expected public-market returns, or strategic allocation. It says more when it aligns with easier funding conditions, stable reserves, lower currency pressure, and broad risk appetite. |

| A larger fixed-income allocation always means defensive positioning. | Fixed-income exposure can be driven by yield levels, liability matching, collateral quality, liquidity preference, reserve-adjacent needs, or duration management. Credit spreads, real yields, fiscal pressure, and currency conditions help refine the reading. |

| An allocation change proves reserve selling, intervention, or de-dollarization. | Fund allocation data is not the same as official reserve data, balance-of-payments evidence, or currency intervention evidence. It can support a broader sovereign-flow view, but it cannot prove those claims alone. |

Conditions That Change the Interpretation

A safer reading separates the observed allocation change from the possible inference, the context needed, and the limit that should remain attached to the claim.

| Observed condition | Possible interpretation | Context needed | Limit on the claim |

|---|---|---|---|

| Higher equity allocation | More exposure to global risk assets. | Market breadth, earnings expectations, liquidity, credit spreads, and valuation context. | Does not prove short-term buying pressure or a durable risk-on regime. |

| Higher fixed-income allocation | Greater demand for income, duration, liquidity, or liability matching. | Yield levels, real rates, curve shape, fiscal needs, and reserve context. | Should not be reduced to a simple defensive signal. |

| Higher private-market allocation | Longer-horizon capital commitment and higher illiquidity tolerance. | Commitment schedule, cash calls, reporting lag, governance, and liquidity environment. | May not create immediate public-market flows. |

| Higher cash or liquidity allocation | More emphasis on flexibility, withdrawals, or fiscal transfer capacity. | Budget pressure, commodity revenues, currency pressure, and external liquidity conditions. | Cash can reflect operational design, not only caution. |

| More strategic domestic assets | Greater focus on national development or industrial policy objectives. | Fund mandate, fiscal role, domestic investment program, and governance structure. | Not directly comparable with return-seeking global portfolio allocation. |

SWF Allocation vs Foreign Exchange Reserves

SWF allocation and foreign exchange reserves can both matter in sovereign balance-sheet analysis, but they are separate categories. SWF allocation describes the asset mix of a sovereign investment fund. Reserve assets are official liquidity and external-stability assets held for monetary, currency, and balance-of-payments purposes.

Boundary: A change in SWF allocation does not by itself prove reserve liquidation, FX intervention, dollar abandonment, or immediate currency pressure. Those claims need separate evidence from reserve data, policy actions, balance-of-payments information, funding stress, and currency-market behavior.

Practical Failure-Mode Scenario

A sovereign fund increases its target exposure to private markets. A weak reading treats that as immediate risk-on capital support for public markets. A stronger reading checks whether the change involves long-term commitments, delayed cash calls, limited public-market turnover, and reporting lag.

The same allocation shift may reflect long horizon, illiquidity tolerance, governance changes, or strategic mandate design. It becomes more relevant for market-structure interpretation only when it aligns with easier liquidity, stable reserve pressure, reduced currency stress, and broader risk appetite.

Common Mistakes and Limitations

- Treating allocation percentages as live flow data: Allocation reports often arrive with delay and may describe targets, surveys, or broad categories rather than current transactions.

- Comparing all sovereign funds as if they share one mandate: Stabilization funds, savings funds, pension reserve funds, reserve-investment vehicles, and strategic development funds can hold different portfolios for different reasons.

- Using a ranking or asset-size table to infer allocation behavior: Fund size says little about liquidity needs, liabilities, governance, risk tolerance, or implementation path.

Data limitation: Current allocation percentages, country-level claims, and fund-specific shifts need a source, date, sample, and methodology. Without those details, allocation data should be treated as conceptual context rather than current evidence.

Related Market-Structure Concepts

Sovereign wealth fund allocation becomes more useful when it is connected to the wider sovereign-flow map. The fund’s mandate explains why the portfolio exists, while reserve context helps separate investment allocation from official liquidity management.

Capital-flow interpretation is strongest when SWF allocation is checked alongside liquidity conditions, DXY pressure, credit stress, fiscal needs, reserve behavior, cross-border flows, and the broader risk-on or risk-off environment.

FAQ

What is sovereign wealth fund asset allocation?

Sovereign wealth fund asset allocation is the way a state-owned investment fund divides capital across asset classes such as equities, bonds, cash, private markets, real assets, alternatives, and strategic holdings.

Does SWF asset allocation predict markets?

No. Allocation can support capital-flow interpretation, but it is not a standalone market forecast. Mandate, liquidity, liabilities, reserve pressure, fiscal needs, and risk appetite all change the meaning.

Why can private-market allocation be misread?

Private-market allocation can reflect long horizon, illiquidity tolerance, delayed cash calls, strategic mandate design, or governance changes. It does not necessarily create immediate public-market demand.

Are SWF assets the same as foreign exchange reserves?

No. SWF assets are investment-fund assets, while foreign exchange reserves are official liquidity and external-stability assets. They can be related in sovereign balance-sheet analysis, but they should not be merged.