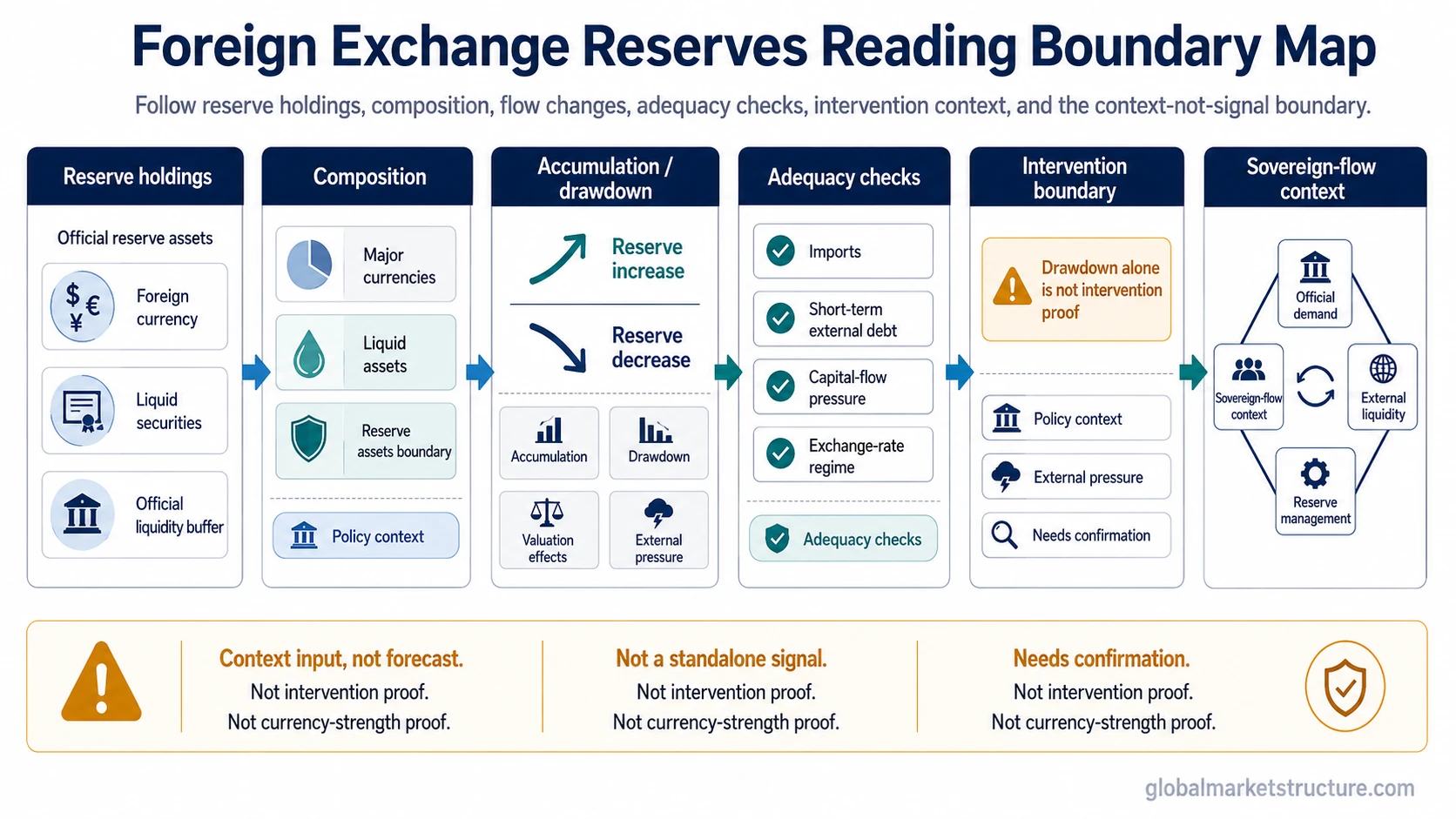

Foreign exchange reserves are official reserve assets controlled by a central bank or monetary authority, mainly foreign-currency and related liquid instruments held for external payments, currency management, policy credibility, and liquidity under stress. They help interpret reserve and sovereign flows, but they are not a standalone forecast, a currency-strength proof, or a trading signal.

Definition: Foreign exchange reserves are liquid official holdings that can be used to meet external obligations, support confidence in the currency regime, and provide a buffer when foreign-currency funding or payment pressure rises.

Holder: They are usually held or managed by a central bank, monetary authority, finance ministry, or official reserve manager, depending on the country and reporting structure.

Market-structure role: The market-structure question is not only how large the reserves are. Reserve stock, reserve change, and reserve composition may reveal external-liquidity pressure, sovereign-flow behavior, and stress around the currency system.

Foreign Exchange Reserves vs Broader Reserve Assets

Foreign exchange reserves are often discussed alongside broader official reserve assets, but the terms should not be treated as identical in every source. Foreign exchange reserves usually refer to foreign-currency reserve holdings and related liquid instruments. Broader official reserve assets may also include items such as monetary gold, special drawing rights, and reserve positions with the IMF, depending on the reporting framework.

Technical boundary: A reserve stock is not the same thing as a reserve transaction. A fall in reserves may reflect valuation changes, debt service, portfolio movement, settlement effects, intervention, or several factors at once. It should not be read as confirmed foreign exchange intervention unless the supporting evidence points in that direction.

The same boundary applies to reserve composition. A reported currency-composition shift can matter for dollar liquidity, portfolio preference, or reserve management, but one data point does not automatically prove a reserve-regime change. Composition needs time series context, valuation adjustment, policy context, and comparison with broader capital-flow behavior.

Why Foreign Exchange Reserves Matter

Foreign exchange reserves matter because they sit at the intersection of external liquidity, sovereign balance-sheet strength, currency management, and official capital flows. A country with usable reserves has more flexibility to meet foreign-currency obligations, manage periods of stress, and smooth pressure when external funding conditions tighten.

For market interpretation, reserves are most useful as context. Rising reserves may suggest reserve accumulation, current-account support, official purchases, or capital inflow pressure. Falling reserves may suggest external-payment pressure, valuation changes, currency support activity, or reserve-portfolio adjustment. The same reserve move can mean different things depending on the exchange-rate regime, capital-account structure, import needs, debt maturity profile, and central-bank policy objective.

Reserve portfolios can also connect to major sovereign-flow channels. For example, some reserve managers hold government securities as part of their liquid reserve portfolio, which is why foreign holdings of U.S. Treasuries can become relevant when analyzing official demand for dollar assets. That connection still needs care: Treasury holdings are one observable channel, not a complete map of all reserve behavior.

Observable Reserve Signals and Interpretation Limits

Reserve data becomes more useful when the observation is separated from the interpretation. Each reading should be treated as conditional evidence, not as an automatic conclusion.

| Observable signal | What it may suggest | What must be checked |

|---|---|---|

| Reserve level | A larger reserve stock may suggest more external-liquidity capacity and greater ability to manage foreign-currency stress. | Reserve adequacy depends on imports, short-term external debt, capital-flow volatility, exchange-rate regime, and reserve usability. |

| Reserve accumulation | Accumulation may reflect current-account surplus, capital inflows, official purchases, or policy preference for a larger reserve buffer. | Check whether the increase comes from transactions, valuation effects, reporting changes, or temporary portfolio movement. |

| Reserve drawdown | Drawdown may suggest external-payment pressure, currency support, debt service, capital outflows, or portfolio adjustment. | Do not assume intervention without corroborating evidence from currency behavior, official statements, balance-of-payments data, or market operations. |

| Currency composition | Composition can show how reserve managers allocate across major reserve currencies and liquid instruments. | Single-period changes can reflect valuation effects, reporting coverage, or portfolio rebalancing rather than a structural regime shift. |

| Reserve adequacy | A reserve stock may look strong or weak relative to a country’s external obligations and potential stress channels. | No universal threshold works for every country. External debt, import cover, capital mobility, and exchange-rate policy all matter. |

| Official data release or revision | New data may clarify the scale, composition, or direction of official reserve holdings. | Check reporting definitions, revision history, valuation effects, and whether the data measures reserves, reserve assets, or a narrower subset. |

Common False Readings

False reading 1: Reserve growth automatically means currency strength. Reserve growth can reflect supportive external flows, but it can also reflect policy choices, managed exchange-rate behavior, or valuation effects.

False reading 2: Reserve drawdown always means intervention. A drawdown may be consistent with intervention, but it can also come from debt payments, portfolio changes, valuation effects, or other official transactions.

False reading 3: High reserves eliminate external risk. A large reserve stock can help, but usability, liability structure, capital controls, external debt maturity, and market confidence still matter.

False reading 4: Currency composition proves future market direction. Composition data can show official allocation behavior, but it does not by itself predict exchange rates, bond yields, or risk-asset performance.

In a practical scenario, falling reserves during currency pressure may raise the possibility of official support activity. The stronger interpretation would require additional evidence: exchange-rate management behavior, official communication, balance-of-payments pressure, capital-flow data, and whether the reserve change is larger than expected valuation effects.

How Foreign Exchange Reserves Connect to Sovereign Flows

Foreign exchange reserves are one official reserve-flow concept inside a broader sovereign-flow system. They overlap with other topics, but each related concept has a different job.

Foreign exchange intervention: Intervention is a possible official action in the currency market. Reserves are the stock of official assets that may support such action, but the existence of reserves does not prove that intervention is happening.

Foreign holdings of U.S. Treasuries: Treasury holdings can be one visible part of dollar reserve management. They do not capture every reserve asset, every reserve manager, or every official dollar-flow channel.

Petrodollar recycling: Oil-export revenue can influence reserve accumulation and dollar-asset demand. The reserve angle becomes clearer when linked to trade surpluses, official saving, and petrodollar recycling channels rather than treated as a generic currency story.

Sovereign wealth fund: A sovereign wealth fund is usually a longer-horizon sovereign investment vehicle. Foreign exchange reserves are normally managed with liquidity, safety, and external-payment capacity in mind, so the investment mandate and interpretation differ.

FAQ

Are foreign exchange reserves the same as total reserve assets?

Not always. Foreign exchange reserves usually refer to foreign-currency reserve holdings and related liquid instruments, while broader reserve assets may also include monetary gold, SDR holdings, and IMF reserve positions depending on the source and reporting framework.

Does a fall in reserves always mean intervention?

No. A fall in reserves can reflect intervention, but it can also reflect valuation changes, debt service, portfolio adjustment, settlement effects, or other official transactions. Intervention requires corroborating evidence.

Are foreign exchange reserves a market signal?

They are a market-structure context input, not a standalone signal. Reserve levels, reserve changes, and reserve composition can help interpret external liquidity and sovereign flows, but they do not predict market direction by themselves.

Why do central banks hold foreign exchange reserves?

Central banks and monetary authorities hold foreign exchange reserves to support external payments, manage liquidity under stress, strengthen policy credibility, and maintain flexibility when currency or funding pressure rises.