What Foreign Holdings of U.S. Treasuries Show

Foreign holdings of U.S. Treasuries show how much Treasury debt is reported as held by foreign official and private investors. The data matters because it gives a window into foreign demand for dollar assets, reserve management, Treasury market participation, and cross-border capital flows.

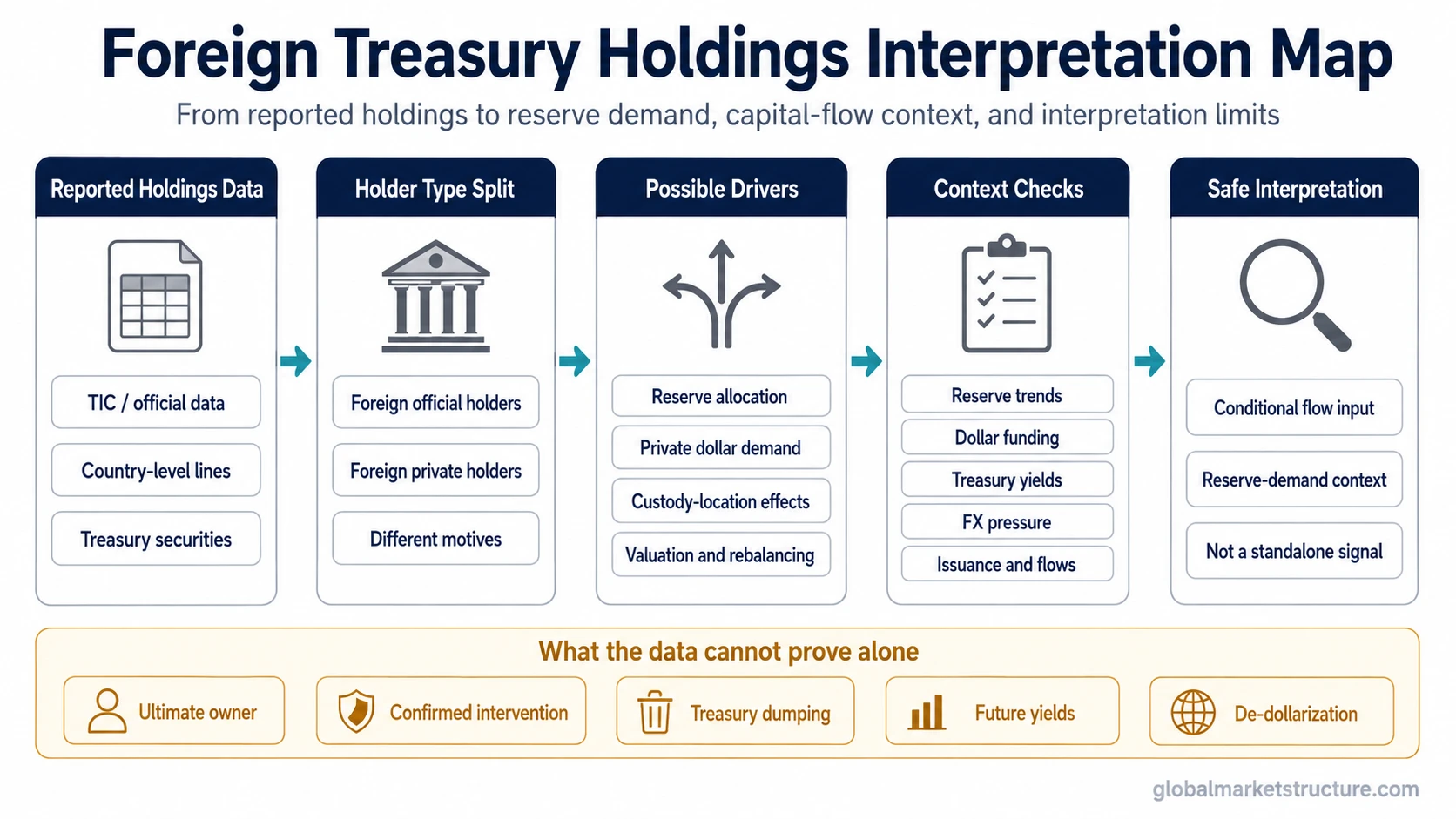

Official data sources can show reported holdings. The analytical task is to interpret what those holdings may mean without treating the table as a complete ownership map, a forecast, or a market signal.

Reported holdings are not a direct signal. A rise or fall can reflect reserve allocation, private foreign demand, custody-location effects, valuation changes, dollar-liquidity pressure, portfolio rebalancing, or changes in the relative appeal of Treasury yields.

What the Data Can and Cannot Show

What the data can show:

- Reported foreign demand for Treasury securities.

- Possible reserve allocation or private demand for dollar assets.

- Capital-flow pressure when confirmed by reserves, yields, exchange-rate pressure, and funding conditions.

What the data cannot prove by itself:

- The ultimate owner behind every country line.

- Deliberate Treasury dumping.

- Confirmed currency intervention.

- Future Treasury yields.

- De-dollarization.

For market-structure analysis, foreign Treasury holdings work best as a conditional input. They become more meaningful when read alongside reserve trends, dollar funding conditions, Treasury issuance, yield changes, exchange-rate pressure, and broader capital-flow evidence.

What the Data Measures

Foreign holdings of U.S. Treasuries refer to Treasury securities reported as held by foreign investors. These holdings can include foreign official institutions, such as central banks and government reserve managers, and foreign private investors, such as banks, funds, insurers, pension managers, and other non-U.S. institutions.

The data matters because U.S. Treasuries sit at the center of the global dollar system. They are used as reserve assets, collateral, liquidity instruments, duration assets, and safe dollar-denominated securities. When foreign holdings change, the move can reveal something about global reserve behavior and demand for dollar assets.

The data should not be read as a clean ownership map. Treasury holdings are often reported by the location of the holder or custodian, not always by the ultimate economic owner. A country-level line may reflect securities held through that jurisdiction rather than the final investor making the economic decision.

Official Versus Private Foreign Holders

The official/private split is one of the most important distinctions.

Foreign official holders are usually central banks, finance ministries, sovereign reserve managers, or other official institutions. Their Treasury holdings often connect to foreign exchange reserves, currency management, reserve adequacy, balance-of-payments flows, and policy choices. A reserve manager may hold Treasuries because they are liquid, dollar-denominated, and widely accepted as high-quality reserve assets. That makes the connection to foreign exchange reserves central to interpretation.

Foreign private holders are different. Their Treasury demand may reflect yield levels, hedging costs, regulatory treatment, collateral needs, portfolio allocation, risk appetite, or demand for dollar safety. A private foreign fund buying Treasuries is not the same signal as a central bank accumulating reserves, even if both appear under foreign holdings.

A clean interpretation begins by asking which type of holder is likely driving the change. Official buying may point toward reserve accumulation or reserve allocation. Private buying may point toward relative yield appeal, safety demand, hedging economics, or cross-border portfolio flows.

Why Foreign Investors Hold U.S. Treasuries

Foreign investors and reserve managers hold U.S. Treasuries for several main reasons.

Liquidity is the first reason. The Treasury market is deep enough for large institutions that need to move capital, manage reserves, or hold collateral without relying on narrow securities.

Dollar exposure is another reason. Many countries, banks, and global institutions operate in a dollar-centered system. Treasuries provide a way to hold dollar assets with high market acceptance.

Reserve management also matters. Central banks often need assets that can be liquidated, pledged, or used as part of a currency-stability framework. Treasuries can serve that role because they are dollar-denominated and widely recognized.

Yield and duration matter too, especially for private holders. When Treasury yields become more attractive relative to hedged foreign bond yields or other safe assets, private demand can rise. When hedging costs increase or local alternatives become more attractive, private demand can weaken. This is why foreign holdings should be read together with Treasury yields rather than treated as a stand-alone flow signal.

Reserve Recycling, Dollar Liquidity, and Treasury Demand

Foreign Treasury holdings can also reflect reserve recycling. When a country runs persistent external surpluses, receives dollar inflows, or accumulates reserves through currency management, part of those dollars may be invested in Treasury securities. In that setting, Treasury holdings can become a visible trace of how global savings and reserve flows move back into U.S. dollar assets.

The mechanism is not automatic. A country can accumulate reserves and allocate them across different instruments. A reserve manager can shift between bills, notes, bonds, agency securities, deposits, gold, or other assets. A private investor can change Treasury exposure for reasons unrelated to national reserve policy.

Dollar liquidity is the broader context. When offshore dollar demand is strong, Treasuries can remain attractive as liquid dollar assets. When dollar funding pressure rises, some investors may need to sell liquid securities to raise dollars. A decline in holdings can therefore signal stress in some cases, but it can also reflect rebalancing, valuation effects, custody shifts, or a different allocation choice.

The same reported change can have different meanings depending on surrounding conditions. A holdings decline during calm markets and stable reserves is not the same as a holdings decline during currency pressure, rising funding stress, and falling reserves.

How to Interpret Changes in Holdings

A monthly or quarterly change in foreign Treasury holdings should be treated as the start of the analysis, not the conclusion.

A rise in holdings can suggest stronger foreign demand for Treasuries, reserve accumulation, private demand for dollar safety, or a relative yield advantage. It may also reflect valuation effects, portfolio duration changes, or custodial reporting patterns.

A decline can suggest weaker demand, reserve drawdown, private portfolio reallocation, intervention-related liquidity needs, or higher hedging costs. It does not automatically mean a country is dumping Treasuries. A country-level decline may reflect securities moving through another custody center, changes in valuation, or a shift between Treasury bills and longer-duration securities.

The safer method is to connect the holdings change to confirmation evidence. If holdings fall while foreign exchange reserves also decline, the local currency is under pressure, and dollar funding conditions tighten, the interpretation becomes more serious. If holdings fall while reserves are stable and private risk appetite is changing, the reading is weaker.

Use the table below as a confirmation map. A holdings change should prompt a question, not finish the analysis.

Interpretation Table

| Observation | Possible Interpretation | Confirmation Needed | Main Limitation |

|---|---|---|---|

| Reported foreign holdings rise | Stronger foreign demand for Treasuries, reserve accumulation, or private demand for dollar assets | Reserve data, official/private split, yield context, currency behavior | Does not prove why the buying occurred |

| Reported foreign holdings fall | Reserve drawdown, private reallocation, custody shift, valuation effect, or weaker Treasury demand | Reserve changes, exchange-rate pressure, funding stress, TIC detail, yield and hedging-cost context | Does not prove deliberate Treasury dumping |

| Official holdings rise | Reserve accumulation or reserve allocation into Treasuries | Broader reserve data, current-account context, currency-policy background | Official holdings may still be affected by reporting and custody issues |

| Private holdings rise | Portfolio demand, yield appeal, collateral demand, or safe-asset demand | Yield spreads, hedging costs, risk appetite, global bond-market conditions | Private demand is not the same as reserve-policy demand |

| Country-level holdings fall | Selling, maturity rotation, custody relocation, valuation effect, or reserve use | Custody data, reserve trend, intervention evidence, market pricing | Country line may not identify the ultimate owner |

| Holdings change during currency pressure | Possible reserve use, dollar-liquidity need, or intervention-related flow | FX reserves, exchange-rate movement, central-bank communication, money-market stress | Holdings alone cannot confirm intervention |

| Holdings change while yields move | Demand may be interacting with duration, issuance, and relative yield attractiveness | Treasury curve behavior, auction demand, foreign hedging costs, issuance mix | Holdings are not enough to forecast yields |

Country Attribution and Custody-Location Limits

Country-level holdings are useful, but they are easy to overread. The reported jurisdiction is not always the same as the ultimate investor. Securities can be held through custodians, financial centers, offshore accounts, or intermediary institutions.

This matters because a country may appear to reduce or increase Treasury holdings even when the underlying economic owner has not changed in the way the headline suggests. Some holdings may be reported through a financial center rather than through the investor’s home country. A shift in custody location can therefore change reported country lines without representing a clean shift in final ownership.

Key limitation: Do not treat each country row as a direct statement of national intent. A decline in one country’s reported holdings may be meaningful, but it needs confirmation from reserve data, exchange-rate conditions, policy communication, and broader capital-flow evidence.

Why Holdings Are Not a Yield Forecast or Trading Signal

Foreign Treasury holdings can affect the market narrative, but they do not provide a direct yield forecast. Treasury yields are shaped by many forces at the same time: expected policy rates, inflation expectations, growth expectations, term premium, Treasury issuance, domestic demand, foreign demand, hedging costs, risk appetite, and liquidity conditions.

A large foreign holder reducing Treasury exposure can matter, especially if the move is persistent and confirmed by other data. The yield effect still depends on the broader market setting. If domestic demand is strong, risk aversion is high, or growth expectations weaken, yields may fall even when some foreign holders reduce exposure. If issuance rises, inflation pressure persists, or term premium increases, yields may rise even when foreign holdings are stable.

The same rule applies to trading interpretation. Foreign holdings are not a buy or sell instruction. They are a macro and capital-flow input. They help frame the demand side of the Treasury market, but they cannot replace rate expectations, liquidity conditions, curve structure, auction demand, credit conditions, and cross-asset confirmation.

Final Limitation

Foreign holdings of U.S. Treasuries are useful as reported evidence of foreign participation in the dollar Treasury market. They can clarify reserve behavior, private foreign demand, capital-flow pressure, and global demand for safe dollar assets.

The data becomes misleading when used as proof of a single story. One holdings line cannot confirm de-dollarization, currency intervention, Treasury dumping, future yields, or the ultimate owner behind a reported position. A stronger reading requires a sequence: reported holdings, official/private split, reserve data, custody limitations, yield context, dollar-liquidity conditions, and cross-asset confirmation.